Union Budget 2020 also known as Aam Admi Budget was presented by current Finance Minister, Nirmala Sitharaman. Common People had lot of expectations from this budget specially in terms of reduction of slab rates, abolishing dividend distribution tax & Long term capital gains, reduction of GST Rates on various articles and Higher Income Tax Deductions.

This Budget is also being quoted as most difficult Budget of the decade for India, due to economic slowdown.

Presently, cycles and other cycles (including delivery tricycles), which are not motorised are chargeable to GST at the rate of 12%. The rate of 12% has became a hurdle for the leading bicycle maker Hero Bicycles.

Leading bicycle maker Hero Cycles urged the government to reduce GST on bicycles from 12 per cent to 5 per cent ahead of the Union Budget to revive demand in the rural markets. The company has also sought extension of FAME-II benefits to electric bicycles.

What is FAME 2?

FAME 2 was announced in first week of March 2019, which proposes to give a push to electric vehicles (EVs) in public transport and seeks to encourage adoption of EV’s by way of market creation and demand aggregation.

FAME 2 will offer incentives to manufacturers, who invest in developing electric vehicles and its components, including lithium-ion batteries and electric motors.

FAME 2 scheme will also help in improving charging infrastructure. The centre will invest in setting up charging stations, with the active participation of public sector units and private players.

Issues faced by the makers of cycle- as per Hero Cycles:-

• The bicycles are largely used by low income group and rural populations. The rate of GST seems to be high. Therefore, slashing GST from the current 12 per cent to the lowest 5 per cent slab would make the cycle cheaper and affordable.

• There is a need to promote electric bicycles as much as the need to promote electric cars. While electric cars address the problem of pollution, they do not address the concern of traffic congestion in Indian cities.

The chairman of HERO MOTORS COMPANY stated that:-

The budget must focus on reviving slumping demand across the country through a series of measures including re-adjusting GST slabs to put more disposable income into the hands of people.

Benefits of extending FAME 2 & reduced rate of GST on cycles:-

• It is noteworthy that lowering the GST rate on cycles from the present rate of 12% to 5% would provide relief to millions of low income households.

• Extending the subsidy benefits of FAME-II to electric bicycles will help manufacturers offer more affordable products to consumers.

• Electric bicycles are both eco-friendly and space friendly and also offer a viable solution to the problem of range anxiety that comes with lack of charging infrastructure as they can be easily pedaled back in case of battery loss.

Double taxation in respect to dividends refers to the fact that dividends are taxed twice.

What are dividends?

Dividends are the profits which are distributed to the shareholders of the company. The shareholder, being the owners of the company, are entitled to the profits of the company. The company, therefore, distributes a certain portion of the profits earned by it to its shareholders, which are termed as dividends. It is not mandatory for the company under any law to distribute dividends to its shareholders, hence, it is at the full discretion of the company to distribute dividends.

What is dividend distribution tax?

The Dividend Distribution Tax is a tax levied on dividends that a company pays to its shareholders out of its profits. The Dividend Distribution Tax, or DDT, is taxable at source, and is deducted at the time of the company distributing dividends, as provided under section 115-O of the Income Tax Act. The dividend is the part of profits that the company shares with its shareholders. The law provides for the Dividend Distribution Tax to be levied at the hands of the company, and not at the hands of the receiving shareholder. However, an additional tax is imposed on the shareholder, who receives over ₹10 lakh in dividend income in a financial year.

How are dividends taxed twice?

Dividends as referred above are the profits which have been earned by the company. These are part of the net business income on which the income tax has been already paid. This means that first the net profits are arrived at by the company and then tax is levied on the profits. After deducting tax from the net profit, the dividend is distributed by the company from the profits remaining with the company after payment of tax. Dividends are then subject to DDT (as discussed under section 115-O of the Income Tax Act. It has been argued that the dividends are the victim of double taxation. Let us know how:-

The dividend distribution tax is doubly-taxed in the following manner:-

• Firstly, the profits earned by the company are subject to income tax at the rate(s) applicable to them.

• The same profits (on which the tax has been levied) when distributed to the shareholders are subject to DDT, on the gross amount of dividend.

What is the procedure for taxation of dividends?

As per section 10(34) of the Income Tax Act, any dividend received by a shareholder from a domestic company is exempt in the hands of the shareholder. Hence, the company has to pay dividend distribution tax on the same. However, this section is subject to section 115BBDA.

As per section 115BBDA, where dividend is received from a domestic company by a specified resident assessee and the amount of dividend exceeds ₹10 lakhs in aggregate, then the receiver is required to pay tax at the rate of 10% on the amount of dividend in excess of ₹10 lakhs. This means that the dividend received up to ₹10 lakhs would be exempt under section 10(34) and the remaining dividend in excess of ₹10 lakhs would be taxable under section 115BBDA.

It is noteworthy that the dividend has already been taxed as business income of the company. Also, the profits of a company are supposed to be the income of shareholders. This way they as part owners i.e. the shareholders have already been taxed.

Hence, the argument extended by most of the corporate houses is that, dividend distribution tax leads to double taxation.

What are the expectations from the budget 2020 in regard to dividends?

This may not seem like a big deal to some people who don’t really earn substantial amounts of dividend income, but it does bother those whose dividend earnings are larger. The double taxation also poses a dilemma to CEOs of companies when deciding whether to reinvest the company’s earnings internally. Because the government takes two bites out of the money paid as dividends, it may seem more logical for the company to reinvest the money into projects that may instead give shareholders earnings in capital gains. Hence, proper amendments in the law relating to DDT is the most expected change from the budget 2020.

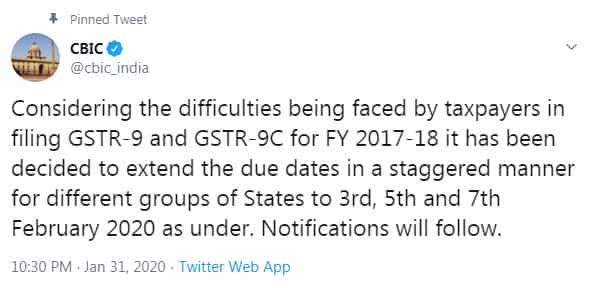

GSTR 9 and GSTR 9C due date for FY 2017-18 extended in staggered manner:

Considering the difficulties being faced by taxpayers in filing GSTR-9 and GSTR-9C for FY 2017-18 it has been decided to extend the due dates in a staggered manner for different groups of States to 3rd, 5th and 7th February 2020 as under. Notifications will follow.

Group 1: Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Puducherry, Telangana, Andhra Pradesh, Other Territory – 3rd February 2020

Group 2: Jammu and Kashmir, Himachal Pradesh, Punjab, Chandigarh, Uttarakhand, Haryana, Delhi, Rajasthan, Gujarat- 5th February 2020

Group 3: Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Andaman & Nicobar Islands, Jharkhand, Odisha, Chhattisgarh, Dadra and Nagar Haveli and Daman and Diu, Lakshadweep, Madhya Pradesh, Uttar Pradesh- 7th February 2020

Notifications will be issued soon in this regards.

GSTN issues advisory on technical problems faced while filing GSTR-9C

GSTN through its twitter account, GST Tech has issued an advisory on technical problems faced while filing GSTR-9C. This issue was related with error while uploading Balance Sheet and Profit & Loss Statement while filing GSTR-9C.

The Advisory was as follows:

“Balance sheet and Profit & loss statement/income & Expenditure Statement keywords used in office network firewall/ content security filter firewall to deny upload of such files/content as these contains sensitive information. If this will be used on open network all such mentioned documents can be uploaded successfully.”

Another issue which was being faced by taxpayers was Error while uploding JSON, that “While trying to upload JSON file they were getting message “ERROR OCCURRED””.

For that, GSTN has issued the advisory that, “This issue is because of incorrect format of data entered in Membership ID being uploaded on GST Portal starting with 0. “0” should not be used.”

This issue is because of incorrect format of data entered in Membership ID being uploaded on GST Portal starting with 0.

“0” should not be used. (2/2)@cbic_india@nsitharaman@nsitharamanoffc@Infosys

With due date of GST Annual Return and GST Audit for FY 17-18, approching near, their is panic among the tax professionals to file the same.

Currently due date of Filing GSTR-9 and GSTR-9C for Financial Year 2017-18 is 31st January 2019.

Penalty for non-filing of GSTR9 is Rs. 200 per day (Rs. 100 in CGST Act and Rs. 100 in respective SGST Act) or 0.25% of total turnover whichever is lower. Further a general penalty of Rs. 50000/- (Rs. 25,000 in CGST Act and Rs. 25,000 in respective SGST Act)can also be levied.

Also there would be 100% chance of Department scruitney if your GST Annual Return is not filed on time.

Lets hope that you are able to file your GSTR-9 & GSTR-9C on or before the due date.

Also in case of any query, do write your comments in the message box.

GSTN started giving advisory of reversal of ITC for FY 2018-19

The advisory reads as follows:

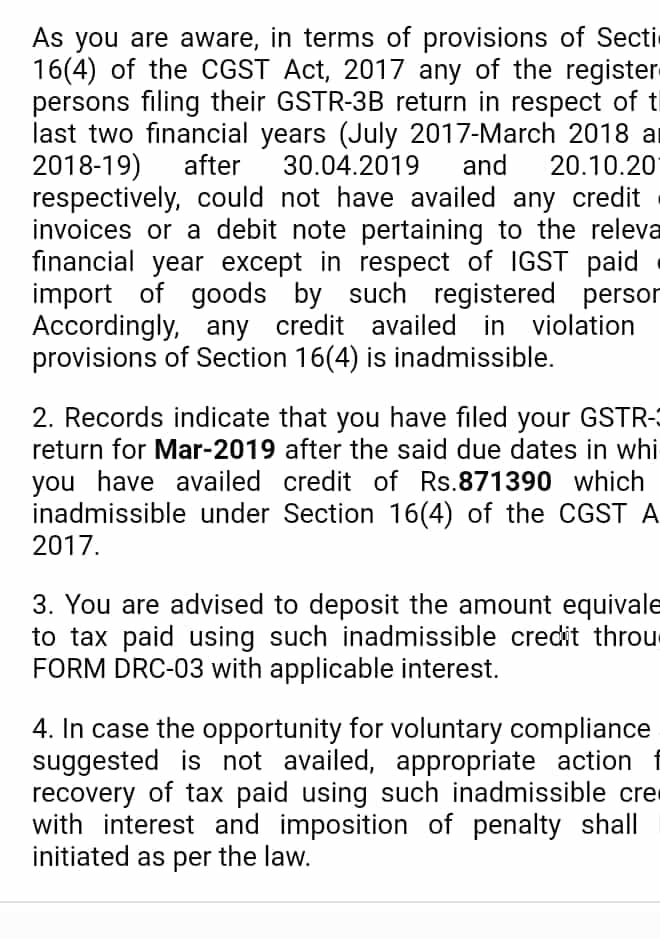

“As you are aware, in terms of provisions of Section 16(4) of the CGST Act, 2017 any of the registerd persons filing their GSTR-3B return in respect of the last two financial years (July 2017-March 2018 and 2018-19) after 30.04.2019 and 20.10.2019 respectively, could not have availed any credit of invoices or a debit note pertaining to the relevant financial year except in respect of IGST paid for import of goods by such registered person. Accordingly, any credit availed in violation provisions of Section 16(4) is inadmissible.”

GSTN started giving advisory of reversal of ITC for FY 2018-19

Points to note:

1. Firstly, this is an advisory and not a notice. The message is system generated.

2. Also, no Document Identification Number has been mentioned in it. Hence, this shall be deemed to have never been issued as per GST Law.

3. The last date to claim ITC of FY 2017-18 was GSTR 3B of March 2019 [i.e. 20/04/2019] and of FY 2018-19 was GSTR 3B of September 2019 [i.e. 20/10/2019)

4. Further, merely late filing of any GSTR 3B does not invalidate the ITC claimed in such month, unless any ITC of preceding FY has been claimed therein and return is filed belated.

5. Since GSTR 3B is summary return, wherein no line item wise detail have been uploaded, without detailed scrutiny, it can never be substantiated that the whole or any part of ITC claimed in any tax period is pertaining to preceding FY and is time barred.

6. Therefore, it can be concluded that this advisory might be generated out of data analytics tool of GSTN. However, it is not in line with the provisions of the law. Hence, no action should be initiated from our end. However, a general submission stating above mentioned facts can be submitted to jurisdiction office without mentioning any figures.

7. Also Taxpayers should do the whole analysis at their end as well, so that they can prepare themself in advance in case of future litigation.

Budget 2020 – Suggestion given for removal of GST Audit, Tax Audit

One of the suggestion given by Advocate community for Budget 2020 is that GST Audit and Tax Audit should be abolished. As per the suggestion, India is a digital economy, where Tax Audits and GST Audits cast shadow on our digital economy. Further as per the argument, there are sufficient safeguards by way of penal provisions provided in tax regime. Therefore, there is no necessity to subject the taxpayers to GST Audits. They also belive, that when entire information about the business done by the taxpayers is readily available to all the officers in the tax administration department, then there is no need of Audit.

Budget 2020 – Suggestion given for removal of GST Audit, Tax Audit

“Hon’ble Prime minister, Sir, it will be good for the GST tax administration if GST Audit is removed from the statute book. This is particularly so when GST Audit even for 2017-18 has still not been done and there are notifications extending the dates for such audits or exempting certain class of taxpayers. The information asked for in the GST Audit Form is readily available to the GST department through various returns filed by the taxpayers. It is impossible for any professionals to give a certificate that all the GST rules have been followed by the taxpayers. GST Audit is done. based on books and other documents that are given by the taxpayers to the accountants. With thousands of documents, legal interpretation of HSN classification, nature of supply, point & time of supply, exemptions, interpretation of tax rates – it is virtually not possible to give a certificate that all GST laws have been complied with.”

Non Quoting of Aadhaar or PAN can lead to 20% TDS Deduction

As per CBDT Circular Number 4/2020, dated 16.01.2020, CBDT has clarified that Employer will deduct 20% TDS in case of Non Quoting of Aadhaar or PAN details. This rule is applicable in case of employee whose salary is more than Exempted Slab.

Section 206AA of Income Tax provides for deduction of TDS at rate of 20% or higher, in case of Non quoting or incorrect quoting of PAN Number. Also, No Lower Tax Deduction declaration is valid in case you dont have a PAN.

As per the new circular, the non quoting of aadhaar or PAN can lead to Higher TDS Deduction. This is also a hint towards, government initiative towards linking of PAN and Aadhaar. So an employee if gives Aadhaar instead of PAN, that will also safeguard him from Higher TDS deduction.

Non Quoting of Aadhaar or PAN can lead to 20% TDS Deduction

This can be summarised by below mentioned example:

For Example if after making all deductions, the average tax rates, comes out less than 20%, then 20% TDS would be deducted. If the average rate is more than 20%, then the higher rate will be applicable.

Notification demanding IGST on ocean freight declared as ultra virus

As per Order of the Court, The impugned Notification No.8/2017 – Integrated Tax (Rate) dated 28th June 2017 and the Entry 10 of the Notification No.10/2017 – Integrated Tax (Rate) dated 28th June 2017 demanding GST on Ocean Freight are declared as ultra vires the Integrated Goods and Services Tax Act, 2017, as they lack legislative competency.

Notification demanding IGST on ocean freight declared as ultra virus

After the judgment is pronounced, Mr.Nirzar Desai, the learned standing counsel appearing for the Union of India, made a request to stay the operation, implementation and execution of the judgment.

Having taken the view that the impugned Notification and the Entry No.10 levying IGST on Ocean Freight therein are ultra vires the IGST Act, 2017, we decline to stay the operation of our judgment.

ITC Claim not shown in VAT Return can’t be availed through merely Filing Form 240 – HC

IN THE HIGH COURT OF KARNATAKA AT BENGALURU

The Extract of the Judgment are as follows :

Fact of the Case

• The petitioners are the dealers registered under the provisions of the Act.

• Based on the annual audit statement of accounts the assessee filed in Form VAT 240 notwithstanding no claim made in the return of turnover filed under Section 35 of the Act.

• The ITC claim of the petitioners based on Form VAT 240 has been rejected by the Authorities.

ITC Claim not shown in VAT Return can’t be availed through merely Filing Form 240 – HC

Decision of the Case

• Justice S. Sujatha observed that all the registered dealers are not required to file such Form VAT 240 but only depending on the total turnover for the year, Form VAT 240 has to be filed.

• In cases where no such VAT 240 is filed, it would certainly result in discrimination if VAT 240 has to be accepted as the basis for determining the Input Tax Credit (ITC). VAT From 240 cannot replace the “return”.

• While dismissing the writ petition Court also said that, When the statutory provision mandates compliance in a particular manner, it should be done in that particular way alone not by any other method.

• The Karnataka High Court has held that the Input Tax Credit ITC claim not shown in the VAT Return cannot be availed through merely filing Form 240.

Direct Tax Updates During The Period 16.12.2019 – 15.01.2020

I. NOTIFICATIONS

1.Form No 10DA (under Rule 19AB) providing for Report under section 80JJAA of the Income-tax Act, 1961 substituted w.e.f. 18.12.2019 – Notification No. 104/2019, dated 18-12-2019

Where the gross total income of an assessee to whom section 44AB applies, includes any profits and gains derived from business, a deduction of an amount equal to 30% of additional employee cost incurred in the course of such business in the previous year, would be allowed under section 80JJAA for three assessment years including the assessment year relevant to the previous year in which such employment is provided. Further, section 80JJAA(2)(c) provides that deduction would be available only if the assessee furnishes alongwith the return of income the report of the accountant giving such particulars in the report as may be prescribed.

Direct Tax Updates During The Period 16.12.2019 – 15.01.2020

Vide this notification, the existing Form No. 10DA providing for Report under section 80JJAA has been substituted. For details regarding the substituted Form No. 10DA, members may refer the aforesaid notification. The said notification is applicable w.e.f. 18.12.2019.

The detailed Notification can be downloaded from the link below:

2. Modes of payment for the purpose of section 269SU specified vide insertion of new Rule 119AA in the Income-tax Rules, 1962 and a related clarification – Notification No. 105/2019 & Circular No. 32/2019, dated 30-12-2019

In furtherance to the declared policy objective of the Government to encourage digital economy and move towards a less-cash economy, a new provision namely Section 269SU was inserted in the Income-tax Act, 1961, vide the Finance (No. 2) Act 2019, which provides that every person having a business turnover of more than Rs 50 Crore (“specified person”) shall mandatorily provide facilities for accepting payments through prescribed electronic modes. The said electronic modes have been prescribed vide notification no. 105/2019 dated 30.12.2019 (“prescribed electronic modes”).

In this regard, new Rule 119AA (Modes of payment for the purpose of section 269SU) has been inserted in the Income-tax Rules, 1962. Rule 119AA provides that the specified person shall provide facility for accepting payment through following electronic modes, in addition to the facility for other electronic modes of payment, if any, being provided by such person, namely:—

(i) Debit Card powered by RuPay;

(ii) Unified Payments Interface (UPI) (BHIM-UPI); and

(iii) Unified Payments Interface Quick Response Code (UPI QR Code) (BHIM-UPI QR Code)

Accordingly, w.e.f. 01.01.2020, the specified person must provide the facilities for accepting payment through the prescribed electronic modes. Further, Section 10A of the Payment and Settlement Systems Act 2007, inserted by the Finance Act, provides that no Bank or system provider shall impose any charge on a payer making payment, or a beneficiary receiving payment, through electronic modes prescribed under Section 269SU of the Act. Consequently, any charge including the MDR (Merchant Discount Rate) shall not be applicable on or after 01.01.2020 on payment made through prescribed electronic modes.

In this connection, it may be noted that the Finance Act has also inserted section 271DB in the Act, which provides for levy of penalty of Rs 5,000 per day in case of failure by the specified person to comply with the provisions of section 269SU. In order to allow sufficient time to the specified person to install and operationalise the facility for accepting payment through the prescribed electronic modes, it is clarified by the CBDT that the penalty under section 271DB shall not be levied if the specified person installs and operationalises the facilities on or before 31.01.2020. However, if the specified person fails to do so, he shall be liable to pay a penalty of Rs 5,000 per day from 01.02.2020 under section 271DB for such failure.

The detailed Notification/Circular can be downloaded from the link below:

3. CBDT further extends the timeline for Linking PAN with Aadhaar from 31.12.2019 to 31.03.2020 – Notification No. 107/2019, dated 30-12-2019

Vide Notification No. 75/2019 dated 28.09.2019, the CBDT had extended the cut-off date for intimating the Aadhaar number and linking PAN with Aadhaar to 31.12.2019, unless specifically exempted.

Vide this notification, the due date for linking PAN with Aadhaar has been further extended from 31.12.2019 to 31.03.2020.

The detailed Notification can be downloaded from the link below:

4. CBDT notifies ITR Form No. 1 and 4 for AY 2020-21 & thereafter grants relaxation in eligibility conditions for filing of said ITR Forms – Notification No. 01/2020, dated 03-01-2020 & Press Release, dated 09-01-2020

In order to ensure that the e-filing utility for filing of return for A.Y 2020-21 is available as on 01.04.2020, the ITR Forms ITR-1 (Sahaj) and ITR-4 (Sugam) for the A.Y 2020-21 are notified vide this notification. In the notified returns, the eligibility conditions for filing of ITR-1 & ITR-4 Forms were modified with an intent to keep these forms short and simple with bare minimum number of Schedules. Therefore, a person who owns a property in joint ownership was not made eligible to file the ITR-1 or ITR-4 Forms. For the same reason, a person who is otherwise not required to file return but is required to file return due to fulfilment of one or more conditions in the seventh proviso to section 139(1), was also not made eligible to file ITR-1 Form.

After the aforesaid notification was issued, concerns were raised that the changes are likely to cause hardship in the case of individual taxpayers. The taxpayers with jointly owned property had expressed concern that they will now need to file a detailed ITR Form instead of a simple ITR-1 and ITR-4. Similarly, persons who are required to file return as per the seventh proviso to section 139(1), and are otherwise eligible to file ITR-1, had also expressed concern that they will not be able to opt for a simpler ITR-1 Form.

The matter was examined by the CBDT and it has been decided to allow a person, who jointly owns a single house property, to file his/her return of income in ITR-1 or ITR-4 Form, as may be applicable, if he/she meets the other conditions. It has also been decided to allow a person, who is required to file return due to fulfilment of one or more conditions specified in the seventh proviso to section 139(1), to file his/her return in ITR-1 Form.

For further details, the newly notified ITR forms 1 and 4 may be referred.

The detailed Notification can be downloaded from the link below:

5. Amendment of rule 10DA and rule 10DB regarding furnishing of information and maintenance of documents by Constituent Entity of an international group – Notification No. 03/2020, dated 06-01-2020

Section 286 provides for furnishing of a Country-by-Country report in respect of an international group by the parent entity or alternate reporting entity, resident in India. Further, section 92D, substituted by the Finance (No.2) Act, 2019, provides for maintenance, keeping and furnishing of information and document by every person who has entered into an international transaction or specified domestic transaction and every person, being a constituent entity of an international group.

Amendments in Rule 10DA

(i) Rule 10DA now provides for maintenance and furnishing of information and document by certain person under section 92D.

(ii) There is no change in sub-rule (1) of Rule 10DA specifying the threshold and the information and documents of the international group to be kept and maintained by every person, being a constituent entity of an international group.

(iii) Sub-rules (2), (3) and (4) have been substituted w.e.f. 1.4.2020. New sub-rule (2) requires the information and document specified under rule 10DA(1) to be furnished to the Joint Commissioner referred to in rule 10DB(1), in Form No. 3CEAA on or before the due date for furnishing the return of income as specified under section 139(1).

(iv) New sub-rule (3) requires the constituent entity to furnish Part A of Form No.3CEAA even if the conditions specified under sub-rule (1) are not satisfied.

(v) New sub-rule (4) provides that where there are more than one constituent entities resident in India of an international group, Form No.3CEAA may be furnished by any one constituent entity if –

(a) the international group has designated such entity for this purpose; and

(b) the information has been conveyed in Form No.3CEAB to the Joint Commissioner referred to in Rule 10DB(1), in this behalf 30 days before the due date of furnishing Form No.3CEAA.

Amendments in Rule 10DB

(i) Sub-rules (1), (2) and (5) have been substituted. Rule 10DB(1) now provides that the income-tax authority for the purposes of section 286 shall be the Joint Commissioner as may be designated by the Director General of Income-tax (Risk Assessment).

(ii) Rule 10DB(2) now provides that the notification under section 286(1) shall be made in Form No. 3CEAC two months prior to the due date for furnishing of report as specified under section 286(2).

(iii) The proviso to section 286(4) requires furnishing of CbC report by any one constituent entity, where there are more than one constituent entity of an international group, resident in India. Such constituent entity should have been designated by the international group to furnish the report on behalf of all the constituent entities resident in India and the information should have been conveyed in writing on behalf of the group to the prescribed authority. Rule 10DB(5) now requires the information required to be conveyed in writing on behalf of the group regarding the designated constituent entity to be furnished in Form No.3CEAE.

Amended Rule 10DA shall come into force w.e.f. 01.04.2020 whereas amendments in rule 10DB is applicable w.e.f. 06.01.2020. For further details, the said notification be referred.

The detailed Notification can be downloaded from the link below:

1. Income-tax Deduction from salaries during the Financial Year 2019-20 under section 192 of the Income-tax Act, 1961 – Circular No. 04/2020, dated 16-01-2020

This CBDT Circular contains the rates for deduction of income-tax from the payment of income chargeable under the head “Salaries” during the financial year 2019-20 and explains certain provisions of the Income-tax Act, 1961 and Income-tax Rules, 1962, including the broad scheme of TDS from Salaries, persons responsible for deducting tax at source from Salaries and their duties, computation of income under the head “Salaries” etc.

The detailed Circular can be downloaded from the link below:

Madras HC denies exemption benefit w.r.t. imports made prior to registration under Rules

Synopsis : The Hon’ble Madras HC in Civil Miscellaneous Appeal No. 1699 of2017 dated January 6th, 2020, allowed the Revenue’s appeal to hold that to avail the exemption of duty under any Notification, the Rules and Regulations and the conditions prescribed therein have to be strictly adhered and thus, the Assessee is not entitled to claim exemption in respect of import of goods made prior to the date of Registration under Rule 3 of the Customs (Import of Goods at Concessional Rate of Duty for Manufacture of Excisable Goods) Rules, 1996 (“Customs Import Rules 1996”).

Facts :

The Commissioner of Customs, Chennai (“the Appellant” or “Revenue”) has filed an appeal in the Hon’ble Madras High Court (“Madras HC”) against the Final Order No. 41210 of 2015 dated September 14th, 2015 passed by the CESTAT Chennai in favour of Medreich Sterilab Ltd. (“the Respondent”) vide Civil Miscellaneous Appeal No. 1699 of 2017, whereby the Hon’ble Tribunal dismissed the Appeal filed by the Appellant in favour of the Respondent M/s. Medreich Sterilab Limited (“the Company”or “the Assessee”).

The Tribunal upheld the order of the lower appellate authority and thereby granted the exemption claimed by the Company, while observing that Rule 3 & 4 of the Customs Import Rules 1996 were only procedural in nature.Therefore, though the Application for registration under Rule 3 was filed later on and the Registration granted to the Respondent to avail the exemption from payment of duty in respect of import under Bill of Entry No. 550344 dated June 28th, 2003 under which goods imported in question which were cleared by the Customs Authority on June 30th, 2003, prior to the date of Registration under Rule 3 on July 14th, 2003, the Company should be granted the exemption claimed.

Revenue’s Contention :

The Tribunal has erred in holding that the requirement of Registration under Rule 3 and 4 of the aforesaid Rules of 1996 were only procedural and the import of goods in question prior to the registration on July 14th, 2003 could not entitle the Company to avail the exemption of duty on the basis of such registration and therefore the Tribunal has erred in granting such exemption in favour of the Assessee.

Assessee’s Contention :

The Certificate was issued by the Superintendent of Central Excise allowing the Company to avail such exemption with respect to the same Bill of Entry No. 550344 dated June 30th, 2003 on July 3rd, 2003 itself and therefore even though the registration of Assessee under 1996 Rules was done later on July 14th, 2003, the Assessee had rightly availed the said exemption and the Rules in question are only directory in nature and therefore the order of the learned Tribunal is justified in accordance with law.

Issue involved :

Whether the Assessee is eligible to avail the benefit of exemption of duty for the pre-registration period?

Held :

The Hon’ble Madras HC passed the following order in the matter of Civil Miscellaneous Appeal No. 1699 of 2017 dated January 6th, 2020:

• The Tribunal has erred in holding that the Rules are merely procedural or directory in nature and upholding the grant of exemption to the Assessee in respect of Bill of Entry No.550344 dated June 28th, 2003 by which the goods were imported and cleared on June 30th, 2003. The Certificate issued by the Superintendent of Central Excise, relied upon by the learned counsel for the Assessee is not under the aforesaid 1996 Rules but it is only a Certificate that the Assessee has not availed the CENVAT Credit on that consignment and that Certificate has nothing to do with the 1996 Rules in question.

•We do not see any justification for the learned Tribunal to hold that these Rules are only procedural or directory in nature and therefore it could be applied for the import made at prior point of time. Then, the very purpose of Rules and requirement of the Assessee to apply under Rule 4 for the intended imports in future would be frustrated, if these Rules were to be applied retrospectively to the imports already made. There wasno question of substantial compliance by the Assessee. The very initiation of procedure of registration and application was not undertaken by the Assessee in the present case.

•It is well settled law that to avail the exemption of duty under any Notification, the Rules and Regulations and the conditions prescribed therein have to be strictly adhered and there is no place for equity or intendment in the interpretation of the taxing Statutes. By holding that the Rules of 1996 are only procedural or directory in nature, the learned Tribunal has frustrated the very purpose of Rules 3 and 4 in question by holding that the Assessee is entitled to the exemption for import made on June 28th, 2003. There is no dispute before us that the registration under Rules 1996 was granted in favour of the Assessee only on July 14th, 2003 and not at any point of time prior to that and therefore we cannot uphold the order passed by the learned Tribunal.

The Hon’ble Madras HC conclusively allowed the appeal filed by the Revenue and set aside the order passed by the learned Tribunal consequently closing the miscellaneous petitions.

Important Provisions :

Rule 3 of Customs Import Rules, 1996 : Registration

(1) A manufacturer intending to avail of the benefit of an exemption notification referred in sub-rule (1) of rule 2, shall obtain a registration from the Assistant Commissioner of Central Excise or Deputy Commissioner of Central Excise having jurisdiction over his factory.

(2) The registration shall contain particulars about the name and address of the manufacturer, the excisable goods produced in his factory, the nature and description of imported goods used in the manufacture of such goods.

(3) The Assistant Commissioner of Central Excise or Deputy Commissioner of Central Excise shall issue a certificate to the manufacturer indicating the particulars refer to in sub-rule(2).

Rule 4 of Customs Import Rules, 1996 : Application by the Manufacturer to obtain the benefit

(1) A manufacturer who has obtained a certificate referred to in sub-rule (3) of rule 3 and intends to import any goods for use in his factory at concessional rate of duty, shall make an application to this effect to the Assistant Commissioner of Central Excise or Deputy Commissioner of Central Excise indicating the estimated quantity and value of such goods to be imported, particulars of the notification applicable on such import and the port of import.

(1A) The manufacture may, at his option, file the application specified under sub-rule (1), either in respect of a particular consignment, or indicating his estimated requirement of such goods for a period not exceeding one year.

(2) The manufacturer shall also give undertaking on the application that the imported goods shall be used for the intended purpose.

(3) The application shall be countersigned by the Assistant Commissioner of Central Excise or Deputy Commissioner of Central Excise who shall certify therein that the manufacturer is registered in his office and has executed a bond to his satisfaction in respect of end use of the imported goods in the manufacturer’s factory and indicate the particulars of such bond.”

DISCLAIMER : The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon.

CAG shall not carry any further Service Tax audit of private agencies after GST – HC

IN THE HIGH COURT OF GUJARAT AT AHMEDABAD

ORDER

1. The petitioner is a limited Company and is engaged in the business of providing material management and logistical requirements of oil and natural gas industries. The petitioner, on behalf of such industries, sets up warehouse service centers and provides support services in Special Economic Zones.

2. The petitioner has challenged the communication issued by the Comptroller and Auditor General of India (“the CAG”, for short) calling upon the petitioner to submit Service Tax audit at the hands of the officers of the CAG.

CAG shall not carry any further Service Tax audit of private agencies after GST – HC

3. In this context, the petitioner would draw our attention to the final communication dated 09.10.2018 issued by the CAG rejecting the petitioner’s objection to initiation of such audit. The respondents seem to be relying heavily on Rule 5A of the Service Tax Rules, 1994 for exercising such powers of audit. Such Rule 5A, as it stood earlier, was challenged before the Delhi High Court and was struck down, as being unconstitutional, in the judgment in case of

Travelite (India) v. Union of India reported in 2014 (35) S.T.R. 653 (Delhi). Before this Court, one Sadbhav Engineering Limited had disputed the authority of CAG to carry out such Service Tax audit. This Court, in case of Sadbhav Engineering Limited v. Union of India reported in 2016 (46) S.T.R. 22 (Guj.), by recording brief reasons, had granted stay against further proceedings. The Court had noted the decision of Delhi High Court in case of Travelite (India) striking down the validity of the said Rule. It was observed as under;

“4. Prima facie, therefore, if Rule 5A is not valid, a serious question of the powers of the authority to issue the impugned communication would arise. Subsidiary question would be, even if Rule 5A is valid, would the communication in question be covered within the powers of the Commissioner as envisaged under subrule (1) of Rule 5A, which empowers the Commissioner to authorize any person to carry out the inquiry with respect to the accounts of an assessee. Whether such authorized persons can be an outsider of the organization of the Commissioner would also be an issue.”

4. Counsel for the petitioner pointed out that the Union of India has asked for transfer of such petitions along with other proceedings filed before different High Courts. Our attention was drawn to an order dated 31.08.2018 passed by the Supreme Court, in which, reference to the said order of this Court is made and the proceedings before the High Court have been stayed. The stay granted by the High Court, however, does not appear to have been disturbed.

5. Counsel for the petitioner submitted that thereafter, Rule 5A of the Service Tax Rules, 1994 was amended. The amended Rule also came to be challenged before the Delhi High Court in case of Mega Cabs Pvt. Ltd. v. Union of India. The Delhi High Court again struck down the Rule in judgment reported in 2016 (43) S.T.R. 67 (Del.). Counsel candidly stated that the Supreme Court has stayed the judgment of the Delhi High Court in case of Mega Cabs Pvt. Ltd. by an order dated 26.09.2016.

6. Quite apart from these legal controversies, counsel for the petitioner raised an additional contention that with the introduction of the Goods and Service Tax Act, the Finance Act, 1994 and the Service Tax provisions made thereon, stand repealed. He referred to Section 174 of the Central Goods and Service Tax Act, 2017 (“the CGST Act” for short) and contended that the Saving Clause contained therein would not save Rule 5A of the Service Tax Rules, 1994, so as to enable the respondents to initiate fresh proceedings for audit under the said Rule.

7. Section 173 of the CGST Act provides that save and otherwise provided in the said Act, Chapter-V of the Finance Act, 1994, shall be omitted. Section 174 of the CGST Act contains Repeal and Saving Clauses. Sub-section (1) thereof provides that save and otherwise provided, on and from the date of commencement of the said Act, several Acts mentioned therein would stand repealed. Sub-section (2) of Section 174 is a Saving Clause and it inter alia provides that the amendment of the Finance Act, 1994 to the extent mentioned in Sub-section (1) of Section 173, shall not revive anything not in force or existing at the time of such amendment or repeal. Clause (e) of this Saving Clause reads as under;

“(e) affect any investigation, inquiry, verification (including scrutiny and audit), assessment proceedings, adjudication and any other legal proceedings or recovery of arrears or remedy in respect of any such duty, tax, surcharge, penalty, fine, interest, right, privilege, obligation, liability, forfeiture or punishment, as aforesaid, and any such investigation, inquiry, verification (including scrutiny and audit), assessment proceedings, adjudication and other legal proceedings or recovery of arrears or remedy may be instituted, continued or enforced, and any such tax, surcharge, penalty, fine, interest, forfeiture or punishment may be levied or imposed as if these Acts had not been so amended or repealed;”

8. A perusal of the said clause of Sub-sectio (2) of Section 174 and other clauses would, prima facie, show that there was no saving of Rule 5A in such manner that fresh proceedings for audit could be initiated in exercise of powers under the said Rule. We, therefore, have serious doubts whether, with the aid of Rule 5A of the Service Tax Rules, 1994, the CAG can carry out compulsory Service Tax audit of private agencies like the petitioner.

9. Under the circumstances, issue Notice, returnable on 28.11.2018. By way of ad-interim relief, the impugned order dated 09.10.2018 is stayed. In other words, the CAG shall not carry out any further Service Tax audit of the petitioner. Direct service permitted.

• Increase in basic exemption limit : With the rise in inflation on the income which is spent out by a person, there is a need to change the exemption limit. It has been observed that the slab rates has remained unchanged since financial year 2014-15. Taking into consideration the relationship between the unchanged tax rate along with the eroding inflation, it is necessary to increase the basic exemption limit.Rather, a rebate has been provided to individuals where the total income does not exceed ₹5 lakh. However, this does not really meet the wider expectation of providing enhanced exemption to all.

Expectations from Budget 2020

When we look at the income threshold limits on which tax is levied for individuals, the last change was made in 2014 when the Modi government presented its first Union budget. Since then, there has not been any major change in these limits albeit some benefits and sops which were given in the years that followed. Thus, the increase in basic exemption limit is one of the note worthy expectation from the upcoming budget.

• Increase in deduction under section 80C : The limit of deduction under section 80C has remained unchanged since the past 5 years. Also the limit of ₹1.5 lakhs under section 80C is inclusive of amount paid on account of tuition fees, principal amount paid on account of loan for purchase of residential house property, LIC premium amount, etc., which are the basic necessities of an individual. The limit of ₹1.5 lakhs is considered as very low, taking into consideration the overall rise in the inflation rate. Alternatively, a separate section may be introduced, in order to provide deductions for certain high-value transactions.

• Increase in deductions in relation to purchase of house property : Presently, there are certain sections which provides deduction of principal as well as interest amount on purchase of house property, but the same is restricted to value of house property being not more than ₹45 lakh and loans up to ₹35 lakh. The expectation is that this is extended to all first time home buyers irrespective of the property value, which will result in a big relief for individuals contemplating to invest in their primary homes.

• Increase in deduction for tuition fees : Deductions for tuition fees are covered under section 80C. In today’s competitive world, education from a premier school has become a necessity and the deduction limit under section 80C is insufficient to cover up the yearly fees spent by the assessee. This limit is required to be increased, taking into consideration the amount spent by the assessee on tuition fees.

• Deduction on fixed deposit interest : Section 80TTA provides for deduction of interest income on savings account. Such a similar deduction should also be available to interest income on fixed deposits. With low interest rates, which does not reflect the inflationary trends, and with taxes eating into such incomes, fixed income investments do not provide any benefit to investors. Also the deduction limit of ₹10000 on interest on savings account is quite low. Hence, extending the deduction to fixed deposit interest is in the wish list of the assessees.

• Enhancement of limits for various exempt allowances : The present taxation system provides for certain exemptions that are allowed to individual tax payers but the thresholds are considered as not in line with the actual expenditure incurred. Therefore, these limits may be enhanced bearing in mind the current inflation rates. The maximum limit of various allowable deductions available for claiming tax benefit have remained constant. For example, children’s education allowance is exempt up to ₹100 per month for maximum two children has not been changed over the years, which can be enhanced to ₹500 per month per child, children’s hostel allowance limit can be enhanced from₹300 to ₹1,500 per month per child and meal vouchers from ₹50 to ₹100 per meal. Also, the limit of standard deduction may be enhanced from ₹50,000 to at least₹75,000.

• Increase in exemption limit on LTCG tax : LTCG tax was re-introduced in Union Budget 2018 making it mandatory for an investor to pay 10% LTCG tax on profit made over ₹1 lakh in a year if he/she sells listed equity shares and equity-oriented mutual funds after keeping them for one year. The expectations are the government will increase the current exemption limit from ₹1 lakh to ₹2 lakh.

• Doing away with Double Taxation on Dividend Distribution Tax : Any domestic company which is declaring/distributing dividend is required to pay DDT at the rate of 15% on the gross amount of dividend as mandated under Section 115O. Therefore the effective rate of DDT is 17.65% on the amount of dividend. Dividend Distribution Tax (Sec 115 O) is 15%.The argument extended by most of the corporate houses is that, it leads to double taxation. Dividend is nothing but distribution of profit of the companies. It is after paying income-tax on the profits earned by the companies, that the profit is distributed among shareholders. Dividend distribution tax is further levied on the profits distributed to the shareholders of a company.

The profits of a company are supposed to be the income of shareholders. This way they as part owners i.e. the shareholders have already been taxed. Dividend distribution tax thus amounts to double taxation; the fact that the companies in India are already paying high corporate tax on these profits further deteriorates the condition of the shareholders.

CUSTOMS, EXCISE & SERVICE TAX APPELLATE TRIBUNAL BANGALORE

The present appeal is directed against the impugned order dated 4.12.2018 passed by the Commissioner (A), whereby the Commissioner (A) has rejected the appeal of the appellant.

2. Briefly the facts of the present case are that the appellants are registered as service providers under the category of ‘Structural Design and Detailing consultancy Services’ and are availing CENVAT credit of service tax paid on various input services used while exporting their output services. The appellant had filed a refund claim for refund of unutilized CENVAT credit of service tax amounting to Rs.5,45,186/- availed on input services for the period April 2017 to June 2017 under Notification No.27/2012-CE (NT) dated 18.6.2012 read with Rule 8 of Cenvat Credit Rules, 2004 (CCR) and Service Tax Rules, 1994. After due process vide Order-in-Original No.162/2018 dated 31.7.2018/7.8.2018, the original adjudicating authority, AC, CT, East Division-I rejected the claim on the ground that the appellant had failed to submit proof of having debited the amount of refund being claimed in his Cenvat credit account, as per the provisions of Para 2(h) of Notification No.27/2012-CE (NT) dated 18.6.2012 read with Section 142(4) of the CGST Act, 2017. Aggrieved by the Order-in-Original, appellant filed appeal before the Commissioner (A), who rejected the appeal. Hence, the present appeal.

Claim of CENVAT Credited in GSTR-3B allowed – HC

3. Heard both the parties and perused the records.

4. Learned counsel for the appellant submitted that the impugned order is not sustainable in law as the same has been passed without properly appreciating the facts and the law. He further submitted that the refund claim amount was debited in the books of accounts on 20.5.2018. The refund claim was filed for the period April 2017 to June 2017 on 14.2.2018 and by that time, the due date to file the Tran-1 was over and the appellant could not envisage the quantum of refund at the time of filing Tran-1, therefore the basis to reject the refund claim was not proper. He further submitted that the refund has been rejected only on procedural lapses created by introduction of GST. He also submitted that they have debited the refund claim amount in May 2018 in GSTR-3B Return. He further submitted that the condition at paragraph 2(h) of the Notification No.27/2012 was applicable only during the period prior to GST regime since GST was done away with the filing of the ST-3 returns. Further, they have submitted that there was no procedure in ACES System to debit the value of refund claim in the Cenvat account during the relevant period. Learned counsel also referred to CBIC Circular No.58/32/2018-GST dated 4.9.2018 wherein the Board itself had clarified that the reversal of credit in GSTR-3B amounts to non- availment of credit. Learned counsel further submitted that the substantive right cannot be denied on merely procedural lapses. For this submission, he relied upon the decision in the case of Ramdev Food Products Pvt. Ltd. vs. CCE, Ahmedabad: 2011 (23) STR 475 (Tri.-Ahmd.) wherein it was held that rectifiable defect should be allowed to be cleared. In the present case, the appellant had debited the refund claim amount in the books of accounts and also the debit is made in the GSTR-3B. He also relied upon the decision in the case of Sandoz Pvt. Ltd. vs. CCE: 2015 (10) TMI 882- CESTAT-Mumbai, wherein it was held that failure to debit on the date of filing the refund claim is not such a lapse that it would debar the appellants from refund. On the day of debiting the CENVAT account, they have fulfilled the conditions of the Notification and thereby become entitled to the refund on that date.

5. On the other hand, the learned AR defended the impugned order.

6. After considering the submissions of both the parties and perusal of the material on record, I find that the appellant have reversed the CENVAT credit in their CENVAT credit account but the same was not shown in the ST-3 Returns because by the time refund was filed, GST has been introduced and filing of ST-3 returns itself was done away with. Further, I find that the appellant has voluntarily debited the refund amount in GSTR-3B during May 2018 which clearly complies with the conditions of the Notification. Further, the Board has also clarified the said position in its Circular No.58/32/2018-GST. Further, I find that in the case of M/s. Global Analytics India Pvt. Ltd. vs. Commissioner of GST reported in 2019 ACR 388 CESTAT CHENNAI, on identical set of facts, the Tribunal has allowed the appeal of the appellant and set aside the denial of refund. Following the ratio of the above said decisions, I am of the considered view that the impugned order is not sustainable in law and therefore, I set aside the same by allowing the appeal of the appellant with consequential relief, if any.

(Order was pronounced in Open Court on 16/12/2019.)

Undervaluation is no sufficient reason for detaining the goods

Complete extract of Order is givn below:

The challenge in the writ petition is to Exts. P8 and P11 detention notices issued to the petitioner detaining goods that were transported at the instance of the petitioner. A perusal of Exts.P8 and P11 notices would indicate that the goods belonging to the petitioner, and covered by Exts.P1 and P1(a) invoices, were detained for an alleged discrepancy noticed in respect of the E- way bill raised in connection with Ext.P1 invoice. I note however that the discrepancy noticed is with regard to the value of the commodity as shown in Ext.P1 invoice, which is Rs.25.60, whereas in the E-way bill, it was shown as Rs.25.66. It is also the case of the detaining authority that the commodity in question was undervalued by the vendor by offering excessive discounts to the purchaser.

Undervaluation is no sufficient reason for detaining the goods

2. I have heard the learned counsel appearing for the petitioner and also the learned Government Pleader appearing for the respondents.

3. On a consideration of the facts and circumstances of the case as also the submissions made across the bar, I find that the reasons shown in Exts.P8 and P11 notices, that are impugned in this writ petition, are not sufficient for the purposes of detaining the goods in terms of Section 129 of the CGST/SGST Act. Accordingly, I direct the 1st respondent to forthwith release the goods and the vehicle to the petitioner on the petitioner producing a copy of this judgment before the said respondent. The 1st respondent shall thereafter forward the files for adjudication to the adjudicating authority.

ROC cannot deactivate DIN of disqualified directors – HC

28. Act, 2013 is made applicable to all companies incorporated under previous Company Law as under Act, 2013, and, certain other companies also as is evident from Section 1(4), which reads as under :

“1(4) The provisions of this Act shall apply to-

(a) companies incorporated under this Act or under any previous company law;

(b) insurance companies, except insofar as the said provisions are inconsistent with the provisions of the Insurance Act, 1938 (4 of 1938) or the Insurance Regulatory and Development Authority Act, 1999 (41 of 1999);

(c) banking companies, except insofar as the said provisions are inconsistent with the provisions of the Banking Regulation Act, 1949 (10 of 1949);

(d) companies engaged in the generation or supply of electricity, except insofar as the said provisions are inconsistent with the provisions of the Electricity Act, 2003 (36 of 2003);

(e) any other company governed by any special Act for the time being in force, except in so far as the said provisions are inconsistent with the provisions of such special Act; and

(f) such body corporate, incorporated by any Act for the time being in force, as the Central Government may, by notification, specify in this behalf, subject to such exceptions, modifications or adaptation, as may be specified in the notification.”

29. The terms “Board of Directors” or “Board” and “Director” are defined in Sections 2(10) and 2(34) and read as under :

“2(10) “Board of Directors” or “Board”, in relation to a company, means the collective body of the directors of the company.

2(34) “director” means a director appointed to the Board of a company.”

30. Chapter XI of Act, 2013 deals with appointment and qualifications of ‘Directors’ and contains Sections 149 to 172. Section 153 to 159 deal with issue of Director Identification Number (i.e. DIN). Section 153 provides that every individual, intending to be appointed as director of a company, shall make an application for allotment of DIN to the Central Government in such form and manner and along with such fees as may be prescribed. Section 154 makes it obligatory upon Central Government to allot DIN within one month from receipt of application under Section 153 to the person applying for the same. Section 155 prohibits more than one DIN to any individual and says that no individual who has already been allotted DIN under Section 154, shall apply for, obtain or possess another DIN. Vide Section 156, every existing Director is under obligation to intimate his DIN to the company or all the companies wherein he is a director, after receipt of DIN from Central Government. Similarly, Section 157 makes it obligatory upon Company to inform ROC of the Directors of companies. Obligation to indicate DIN is provided under Section 158. It says that every person or company, while furnishing any return, information or particulars, as are required to be furnished under Act, 2013, shall mention DIN in such return, information or particulars, in case such return, information or particulars related to the Director or contain any reference of any Director.

31. Section 164 of Act, 2013 talks of disqualifications for appointment of Director. It came to be enforced from 01.04.2014 and has been amended twice, inasmuch as, a proviso was added to sub-section 2 of Section 164, vide Section 52(i) of Act 1 of 2018, w.e.f. 07.05.2018. Existing proviso to sub- section 3 of Section 164 was substituted by Section 52 (iii) of Act 1 of 2018, which also came into force on 07.05.2018. Section 164 as it stood on and after 07.05.2018, after amendment vide Act 1 of 2018, reads as under :

“164. Disqualifications for appointment of director .-(1) A person shall not be eligible for appointment as a director of a company, if-

(a) he is of unsound mind and stands so declared by a competent court;

(b) he is an undischarged insolvent;

(c) he has applied to be adjudicated as an insolvent and his application is pending;

(d) he has been convicted by a court of any offence, whether involving moral turpitude or otherwise, and sentenced in respect thereof to imprisonment for not less than six months and a period of five years has not elapsed from the date of expiry of thesentence:

Provided that if a person has been convicted of any offence and sentenced in respect thereof to imprisonment for a period of seven years or more, he shall not be eligible to be appointed as a director in any company;

(e) an order disqualifying him for appointment as a director has been passed by a court or Tribunal and the order is in force;

(f) he has not paid any calls in respect of any shares of the company held by him, whether alone or jointly with others, and six months have elapsed from the last day fixed for the payment of the call;

(g) he has been convicted of the offence dealing with related party transactions under section 188 at any time during the last preceding five years; or

(h) he has not complied with sub-section (3) of section 152.

(2) No person who is or has been a director of a company which—

(a) has not filed financial statements or annual returns for any continuous period of three financial years; or

(b) has failed to repay the deposits accepted by it or pay interest thereon or to redeem any debentures on the due date or pay interest due thereon or pay any dividend declared and such failure to pay or redeem continues for one year or more, shall be eligible to be re-appointed as a director of that company or appointed in other company for a period of five years from the date on which the said company fails to do so.

Provided that where a person is appointed as a director of a company which is in default of clause (a) or clause (b), he shall not incur the disqualification for a period of six months from the date of his appointment.

(3) A private company may by its articles provide for any disqualifications for appointment as a director in addition to those specified in sub-sections (1) and (2):

Provided that the disqualifications referred to in clauses (d), (e) and (g) of sub-section (1) shall continue to apply even if the appeal or petition has been filed against the order of conviction or disqualification.”

(Provisions shown in bold were amended by Act 1 of 2018 w.e.f. 07.05.2018)

32. Broadly Section 164 of Act, 2013 is not only similar to Section 274 of Act, 1956 but a bit wider. Disqualification added in Section 274 (1) by insertion of Clause (g) has been continued in Section 164 though framed in slightly different language and is on the Statute as sub-section (2) of Section 164 of Act, 2013.

33. Under Act, 2013 liability to file Annual Return is provided vide Section 92. It says that every Company shall prepare a return (described in Section 92 as “Annual Return”) in the prescribed form containing particulars as detailed in Sub-section 1 of Section 92, as they stood on the close of Financial Year. Such Annual Return shall be signed by Director and the Company Secretary. Where there is no Company Secretary, it shall be signed by a Company Secretary in practice. Sub-section (4) of Section 92 makes it obligatory for every Company to file Annual Return with ROC within sixty days from the date on which Annual General Meeting (hereinafter referred to as ‘AGM’) is held or where no AGM is held in any year within sixty days from the date on which AGM should have been held together with the statement specifying the reasons for not holding the AGM. We find it appropriate to reproduce Sub-section (4) of Section 92 of Act, 2013 as under :

“92(4). Every company shall file with the Registrar a copy of the annual return, within sixty days from the date on which the annual general meeting is held or where no annual general meeting is held in any year within sixty days from the date on which the annual general meeting should have been held together with the statement specifying the reasons for not holding the annual general meeting, with such fees or additional fess as may be prescribed.”

(emphasis added)

34. Earlier with regard to payment of fees or additional fees it was provided that it could have been paid within time as specified under Section 403 but it has been amended by Act 1 of 2018 w.e.f. 07.05.2018 and now Sub-section (4) says that payment of fees or additional fees shall be as may be prescribed. Therefore, we have quoted Sub-section (4) of Section 92 as it stands after amendment made by Act 1 of 2018 w.e.f. 07.05.2018.

35. Sub-section 5 of Section 92 of Act, 2013 contemplates failure on the part of a Company to file its Annual Return under Sub-section (4) and says that it is an offence punishable with fine and every officer of the Company, who is in default is liable to be punished with imprisonment as well as fine as provided therein. We may produce sub-section (5) of Section 92 of Act, 2013 as under :

“92 (5). If a company fails to file its annual return under sub- section (4), before the expiry of the period specified under Section 403 with additional fees, the company shall be punishable with fine which shall not be less than fifty thousand rupees but which may extend to five lakhs rupees and every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to six months or with fine which shall not be less than fifty thousand rupees but which may extend to five lakh rupees, or with both.”

(emphasis added)

36. Section 96 of Act, 2013 provides for Annual General Meeting (AGM) and says that in each year, in addition to any other meeting, a general meeting as its Annual General Meeting shall be held by Company and there shall not be a gap of more than fifteen months between two Annual General Meetings of the Company.

ROC cannot deactivate DIN of disqualified directors – HC

37. Section 137 of Act, 2013 provides for filing of Financial Statements by a Company with ROC. Here also non-compliance of filing of Financial Statements under sub-section(1) or (2), has been declared to be an offence punishable with fine for the Company, and, Managing Director and Chief Financial Officer of the Company or Director of the Company are punishable with fine and imprisonment or both. Section 137 of Act, 2013 has also undergone certain minor amendments by Act 1 of 2018 w.e.f. 09.02.2018 and 07.05.2018, hence we reproduce Section 137 of Act, 2013 as amended with effect from 07.05.2018 as under:

“137.Copy of financial statement to be filed with Registrar.(1) A copy of the financial statements, including consolidated financial statement, if any, along with all the documents which are required to be or attached to such financial statements under this Act, duly adopted at the annual general meeting of the company, shall be filed with the Registrar within thirty days of the date of annual general meeting in such manner, with such fees or additional fees as may be prescribed.

Provided that where the financial statements under sub- section (1) are not adopted at annual general meeting or adjourned annual general meeting, such unadopted financial statements along with the required documents under sub-section (1) shall be filed with the Registrar within thirty days of the date of annual general meeting and the Registrar shall take them in his records as provisional till the financial statements are filed with him after their adoption in the adjourned annual general meeting for that purpose:

Provided further that financial statements adopted in the adjourned annual general meeting shall be filed with the Registrar within thirty days of the date of such adjourned annual general meeting with such fees or such additional fees as may be prescribed:

Provided also that a One Person Company shall file a copy of the financial statements duly adopted by its member, along with all the documents which are required to be attached to such financial statements, within one hundred eighty days from the closure of the financial year:

Provided also that a company shall, along with its financial statements to be filed with the Registrar, attach the accounts of its subsidiary or subsidiaries which have been incorporated outside India and which have not established their place of business in India.

Provided also that in the case of a subsidiary which has been incorporated outside India (herein referred to as “foreign subsidiary”), which is not required to get its financial statement audited under any law of the country of its incorporation and which does not get such financial statement audited, the requirements of the fourth proviso shall be met if the holding Indian company files such unaudited financial statement along with a declaration to this effect and where such financial statement is in a language other than English, along with a translated copy of the financial statement in English.

(2) Where the annual general meeting of a company for any year has not been held, the financial statements along with the documents required to be attached under sub-section (1), duly signed along with the statement of facts and reasons for not holding the annual general meeting shall be filed with the Registrar within thirty days of the last date before which the annual general meeting should have been held and in such manner, with such fees or additional fees as may be prescribed.

(3) If a company fails to file the copy of the financial statements under sub-section (1) or sub-section (2), as the case may be, before the expiry of the period specified, the company shall be punishable with fine of one thousand rupees for every day during which the failure continues but which shall not be more than ten lakh rupees, and the managing director and the Chief Financial Officer of the company, if any, and, in the absence of the managing director and the Chief Financial Officer, any other director who is charged by the Board with the responsibility of complying with the provisions of this section, and, in the absence of any such director, all the directors of the company, shall be punishable with imprisonment for a terms which may extend to six months or with fine which shall not be less than one lakh rupees but which may extend to five lakh rupees, or with both.”

38. Section 403 of Act, 2013 talks of fees for filing any document required to be filed under Act, 2013 with ROC and for the purpose of present dispute we do not find it relevant, so skipping said provision.

39. However, aforesaid provisions make it clear that filing of Annual Returns and Financial Statements are obligatory, non-compliance thereof is punitive and penal is nature. Therefore, Legislature has found it expedient to include violation of said provisions as one of the disqualification of a person to be a Director of such Company.

40. Section 167 of Act, 2013 which came into force on 01.04.2014 provides for contingencies when office of director shall become vacant. Here also a proviso was inserted in clause (a) of sub-section 1 of Section 167 vide Section 54 (i) of Act 1 of 2018 w.e.f. 07.05.2018 and existing proviso after clause (f) of Section 167 was substituted by aforesaid amendment act. The amended Section 167, reads as under :

“167. Vacation of office of director.-(1) The office of a director shall become vacant in case-

(a) he incurs any of the disqualifications specified in Section 164:

Provided that where he incurs disqualification under sub- section (2) of Section 164, the office of the director shall become vacant in all the companies, other than the company which is in default under that sub-section.

(b) he absents himself from all the meetings of the Board of Directors hold during a period of twelve months with or without seeking leave of absence of the Board;

(c) he acts in contravention of the provisions of Section 184 relating to entering into contracts or arrangements in which he is directly or indirectly interested;

(d) he fails to disclose his interest in any contract or arrangement in which he is directly or indirectly interested, in cotravention of the provisions of Section 184;

(e) he becomes disqualified by an order of a court or the Tribunal;

(f) he is convicted by a court of any offence, whether involving moral turpitude or otherwise and sentenced in respect thereof to imprisonment for not less than six months;

Provided that the office shall not be vacated by the director in case of orders referred to in clauses (e) and (f)-

(i) for thirty days from the date of conviction or order of disqualification;

(ii) where an appeal or petition is preferred within thirty days as aforesaid against the conviction resulting in sentence or order, until expiry of seven days from the date of which such appeal or petition is disposed of; or

(iii) where any further appeal or petition is preferred against order or sentence within seven days, until such further appeal or petition is disposed of.

(g) he is removed in pursuance of the provisions of this Act;

(h) he, having been appointed a director by virtue of his holding any office or other employment in the holding, subsidiary or associate company, ceases to hold such office or other employment in that company.

(2) If a person, functions as a director even when he knows that the office of director held by him has become vacant on account of any of the disqualifications specified in sub-section (1), he shall be punishable with imprisonment for a term which may extend to one year or with fine which shall not be less than one lakh rupees but which may extend to five lakh rupees, or with both.

(3) Where all the directors of a company vacate their offices under any of the disqualifications specified in sub-section (1), the promoter or, in his absence, the Central Government shall appoint the required number of directors who shall hold office till the directors are appointed by the company in the general meeting.

(4) A private company may, by its articles, provide any other ground for the vacation of the office of a director in addition to those specified in sub-section (1).”

(Provisions shown in bold were amended by Act 1 of 2018 w.e.f. 07.05.2018)

41. Before proceeding further we find it appropriate to refer one more provision i.e. Section 470 of Act, 2013 which has been enforced w.e.f. 12.09.2013. It provides that if any difficulty arises in giving effect to the provisions of Act, 2013, Central Government may, by order published in Official Gazette, make such provision, not inconsistent with the provisions of this Act, as appear to it to be necessary or expedient for removing difficulty. It also provides that no order under sub-section (1) of Section 470 shall be made after expiry of a period of five years from the date of commencement of Section 1 of Act, 2013. Section 470 of Act, 2013 is reproduced as under :

“470. Power to remove difficulties.-(1) If any difficulty arises in giving effect to the provisions of this Act, the Central Government may, by order published in the Official Gazette, make such provisions, not inconsistent with the provisions of this Act, as appear to it to be necessary or expedient for removing the difficulty:

Provided that no such order shall be made after the expiry of a period of five years from the date of commencement of Section 1 of this Act.

(2) Every order made under this section shall, as soon as may be after it is made, be laid before each House of Parliament.”

42. Section 1 of Act, 2013 came into force at once i.e. 30.08.2013 when it was published in the Gazette of India(Extra-ordinary) after receiving assent of the President on 29.08.2013. Therefore, Central Government may issue orders referable to Section 470 (1) of Act, 2013 for five years i.e. upto 29.08.2018.

43. Now we proceed to consider rival submissions advanced in these writ petitions.

44. The First Question, up for consideration is, “What shall be the financial years, which can be considered for the purpose of disqualification under Section 164 (2) of Act, 2013, which came into force on 01.04.2014?”

45. “Financial Year” has been defined under Section 2(41) of Act, 2013 and it also came into force w.e.f. 01.04.2014. It reads as under :

“2(41) “financial year”, in relation to any company or body corporate, means the period ending on the 31st day of March every year, and where it has been incorporated on or after the 1st day of January of a year, the period ending on the 31st day of March of the following year, in respect whereof financial statement of the company or body corporate is made up :

Provided that on an application made by a company or body corporate, which is a holding company or a subsidiary or associate company of a company incorporated outside India and is required to follow a different financial year for consolidation of its accounts outside India, the Tribunal may, if it is satisfied, allow any period as its financial year, whether or not that period is a year:

Provided further that a company or body corporate, existing on the commencement of this Act, shall, within a period of two years from such commencement, align its financial year as per the provisions of this clause”

(emphasis added)

46. A perusal of Section 2(41) of Act, 2013 shows that for a provision, which came into force on 01.04.2014, ‘Financial Year’ which ended on 31.03.2014 will not be relevant, inasmuch as, disqualification under Section 164(2)(a) of Act, 2013 is failure of submission of Financial Statements or Annual Returns for any continuous period of three Financial Years and this provision, which is adverse and penal in nature, cannot be made applicable to a Financial Year which had already lapsed and when there was no such condition attracting any disqualification on an event as provided under Section 164(2) (a) of Act, 2013.

47. In taking above view, we need to look into the question, whether Section 164 (2) of Act, 2013 is retrospective or prospective or any other argument for the reason that a plain reading, in our view, leaves no manner of doubt that ‘Financial Year’ in which Section 164 of Act, 2013 has been enforced has to be excluded; A provision which has been enforced w.e.f. 01.04.2014 and talks of three Financial years, if read with Section 2 (41) of Act, 2013 clearly shows that such ‘Financial Year’ must commence from 1st April of the concerned year and Financial Year which has ended on 31st March, will not be covered. Probably this was also realized by Central Government, inasmuch as, a General Circular No.08/14 dated 04.04.2014 was issued by Ministry of Corporate Affairs and the relevant extract of said Circular reads as under :

“Although the position in this behalf is quite clear, to make things absolutely clear it is hereby notified that the financial statements (and documents required to be attached thereto), auditors report and Board’s report in respect of financial years that commenced earlier that 1st April shall be governed by the relevant provisions/schedules/rules of the Companies Act, 1956 and that in respect of financial years commencing on or after 1st April, 2014, the provisions of the new Act shall apply.”

(emphasis added)

48. The above Circular also shows that ‘Financial Year’ commencing from 1st April after enforcement of Section 164 of Act, 2013 will be relevant and hence, it would cover Financial Year 2014-15 and thereafter. Therefore, for the purpose of Section 164 (2) (a) of Act, 2013, in our view, three Financial Years relevant for attracting Section 164 (2) (a) of Act, 2013, would commence from Financial Year 2014-15 and onwards and not prior thereto.

49. We find that considering a similar issue, Gujarat High Court in Gaurang Balvantlal Shah Vs. Union of India, 2019 GLH (1) 444; Madras High Court in Bhagavan Das Dhananjaya Das Vs. Union of India and Anr., (2018)6 MLJ 704; Karnataka High Court in Yashodhara Shroff vs. Union of India, (2019)155 SCL 299; and Telangana High Court in Venkata Ramana Tadiparthi vs. Union of India (Writ Petition No.5422 of 2019) decided on 18.07.2019, have also taken same view. We also find that a Division Bench of this Court (at Lucknow Bench) in Mohd. Tariq Siddiqui and others Vs. Union of India and others (Misc Bench No.16173 of 2019 and other connected matters) decided on 15.10.2019 has followed the view taken by Gujarat High Court in Gaurang Balvantlal Shah (supra) and has also said in para 6 of the judgment that besides Madras High Court similar view has been taken by Madhya Pradesh High Court also. Since Division Bench of this Court has also followed the view taken by Gujarat High Court, we also find no reason to take a different view in the matter.

50. We, therefore, answer the question by observing that for attracting mischief of Section 164(2) (a) of Act, 2013, the ‘Financial Year’ would commence from 2014-15 and not prior thereto.