Corporate Compliance Calendar for the Month of May 2020

This Article contains statutory compliance calendar 2020, ROC compliance calendar 2020-21, compliance calendar 2020 pdf, compliance calendar 2020 in excel, mca compliance calendar 2020, labour law compliance calendar 2020, GST compliance calendar 2020, Income Tax compliance calendar 2020-21, TDS due dates, TDS Return due date, TDS payment due date, Income Tax Return due Date

This article contains various Compliance requirements under Statutory Laws. Compliance means “adhering to rules and regulations.”

“If you think compliance is expensive, try non‐ compliance”

Corporate Compliance Calendar for the Month of May 2020

Compliance Requirement Under

Income Tax Act, 1961

Goods & Services Tax Act, 2017 (GST)

Other Statutory Laws

Foreign Exchange Management Act, 1999 (FEMA) and Important Notifications

SEBI (Listing Obligations & Disclosure Requirements) (LODR) Regulations, 2015

SEBI Takeover Regulations 2011

SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018

SEBI (Buyback of Securities) Regulations, 2018

SEBI (Depositories and Participants) Regulations 2018) and Circulars / Notifications

Companies Act, 2013 (MCA/ROC Compliance)

Insolvency and Bankruptcy Board of India (IBBI) Updates

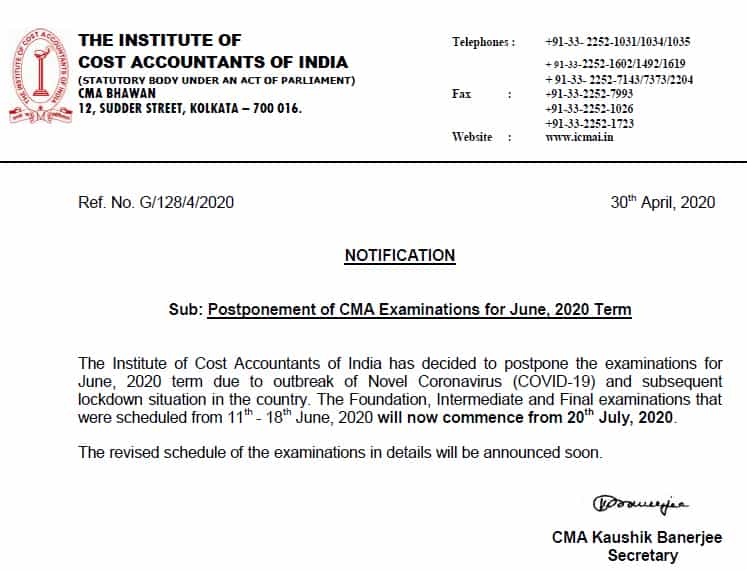

The Institute of Cost Accountants of India has decided to postpone the examinations for June, 2020 term. This is done due to outbreak of Novel Coronavirus (COVID-19) and subsequent lockdown situation in the country. The Foundation, Intermediate and Final examinations that were scheduled from 11th – 18th June, 2020 will now commence from 20th July, 2020.

The revised schedule of the examinations in details will be announced soon.

The Institute of company Secretaries of India, after due consideration of the prevalent situation and subsequent lockdown, due to Covid 19, has decided to postpone its Examinations (June – 2020 session) of Foundation, Executive and Professional Programme and Post Membership Qualification (PMQ) schedured to be held from 1st June,2020 to 10th June, 2020.

The examinations of the above session will now commence from 6th July.2020. The Revised schedule will be announced later

Companies Appointment and Qualification of Directors Second Amendment Rules 2020

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]

Government of India

Ministry of Corporate Affairs

Notification

New Delhi, the 29 April 2020

G.S.R. . . . (E). – In exercise of the powers conferred by section 149 read with section 459 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules further to amend the companies (Appointment and Qualification of Directors) Rules, 2014, namely:-

1. (1) These rules may be called the Companies (Appointment and Qualification of Directors) Second Amendment Rules, 2020.

(2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Companies (Appointment and Qualification of Directors) Rules, 2014, in rule 6, in sub-rule (1), in clause (a), for the words “five months” the words “seven months” shall be substituted.

Interest income from Fixed Deposits is taxable at marginal rate of taxation of the assessee. Add it to your total income and get taxed at slab rates applicable to your total income. This is where debt mutual funds score over Fixed Deposits, debt mutual funds for holding period greater than three years are taxed at 20% after adjusting the cost of inflation index in purchase price. It gives a decent tax arbitrage to assesses having taxable income in 30% tax bracket.

In debt mutual funds there are three types of risk:

As we all know, there is an inverse correlation between price of the bond and rate of interest. This risk can be avoided by investing in schemes following roll down maturities or target maturity ETFs.

Credit Risk:

In case the issuer defaults on coupon or principal or both, investors can potentially lose their entire capital.

Liquidity Risk:

In an open-ended debt fund, AMC is bound to honour redemptions within 10 working days and standard business practices are to honour redemption at T+1 days, provided the investor has submitted a valid redemption request before cut-of time. In case the redemption requests (in rupee terms) received by the fund house for a particular scheme is greater than the liquid marketable assets in the fund, the scheme has the option to borrow up to 20% of the net AUM. What if the redemption request is even more than that? This is exactly what happened in six of the Franklin Schemes. It is known as liquidity risk.

Through a notice dated April 23, 2020, the Trustees of Franklin Templeton Mutual Fund in India announced their decision to wind up six schemes

1) Franklin India Low Duration Fund

2) Franklin India Ultra Short Bond Fund

3) Franklin India Short Term Income Plan

4) Franklin India Credit Risk Fund

5) Franklin India Dynamic Accrual Fund

6) Franklin India Income Opportunities Fund

AMC blamed it on COVID-19, extended lockdown and very low liquidity in lower rated bonds. These 6 wound up schemes are no longer available for subscription or redemption post cut-off time from April 23, 2020. All Systematic Investment Plans (SIP), Systematic Transfer Plans (STP) and Systematic Withdrawal Plans (SWP) into and from the above-mentioned funds have been cancelled by the AMC post cut-off time from April 23, 2020.

SEBI in October 2017 classified the debt schemes under 16 categories, only 2 of the categories were based on credit profile of the scheme rest were based on maturity of the schemes. Two categories which were based on credit profile are:

1) Corporate Bond Funds: 80% of the net assets have to be invested in only in highest rated papers.

2) Credit Risk Funds: 65% of the net assets have to be invested in instruments below highest rating.

Let us now see the split of assets as on 31st march’2020 in 16 categories of debt mutual funds.

Fixed Deposit Investors & Debt Funds

Investors have seen maximum pain in this category. Look at the returns on different time frames.

In the credit risk category, 41335 Crore of funds have been flown out from these categories since 31st March 2019.

There have been instances of markdown in other categories as well. Look at the impact of DHFL default on open ended funds and Fixed Maturity Plans, below two pics represents only one day of markdown.

What shall investors do?

Investors should take help from their financial planner (please note your mutual fund distributor, LIC Agent or Bank relationship manager is not your financial planner) & DIY investors should stick to simpler solutions like target maturity funds and open ended mutual funds running roll down maturity with near to highest credit quality.

This article has been written by an aspiring fee only financial planer who intends to start affordable fee only advisory after getting the licence from SEBI. Writer can be reached on twitter @stepbystep888 (Nishant Batra)

Ministry of Corporate Affairs (MCA) has made amendments under Schedule III of the Companies Act, 2013 and read with notification S.O. 368(E) dated 22nd January, 2019 and introduced Companies (Furnishing of information about payment to micro and small enterprise suppliers) Order 2019 thereby notified filing of Form MSME1.

Under Form MSME1 The companies are required to make certain disclosures pertaining to the vendors registered under the Micro, Small and Medium Enterprises Development Act, 2006 (MSMED Act, 2006)

Imp. Q. Can we file MSME forms pursuant to CFSS Scheme?

Ans. No, There is no fees that is to be paid while filing the MSME form and The CFSS grants immunity from any additional fees, penalty and prosecution.

Form MSME1 is also not included in the list of forms available under CFSS Scheme.

20 FAQ’S ON E-FORM MSME1

FAQ’s ON MCA E-Form MSME1

S. No.

Questions

Answers

1

What are the Provisions applicable to MSME1 Form?

Order 2 and 3 dated 22 January, 2019 issued under Section 405 of the Companies Act, 2013

2

What is the Objective of MSME1 Form ?

furnishing half yearly return with the registrar in respect of outstanding payments to Micro or Small Enterprises

3

Nil Return (no outstanding amounts) is required to be filed?

No.

4

What is Return Type?

Half Yearly Return (the form was introduced with two types of returns – Initial and Half Yearly Return.)

5

What is the Due Date to file MSME1 Form?

a) For Half year period April to September – 31st October

b) For half year period October to March – 30th April

6

Who is required to file MSME1 Form?

All companies, who get supplies of goods or services from micro and small enterprises and whose payments to micro and small enterprise suppliers exceed forty-five days from the date of acceptance or the date of deemed acceptance of the goods or services as per the provisions of section 9 of the Micro, Small and Medium Enterprises Development Act, 2006

7

Whose details are required to be reported ?

Whose payments exceed 45 days from the date of acceptance or the date of deemed acceptance of the goods or services as per provisions of Section 9 of the Micro Small and Medium enterprises Development Act, 2006 (MSMED Act)

8

If agreement terms for payment is 28 days, and payment is made after 28 days?

it is termed as delayed payment and should be reported under MSME1 Form.

9

If agreement is made to make payment within 60 days between the parties but as on date of filing return the amount is outstanding for more than 45 days but less than 50 days. Whether reporting is required or not?

In this case, Reporting has to be made as per the rules made thereby and shall be given if the amount is outstanding for more than 45 days.

10

In case, if there is no agreement?

45 days criteria will be applicable when there is no agreement or agreement for 45 days.

11

If any Supplier is not registered under MSMED Act, 2006 and at the time of Filing return he got status of Micro or Small ?

Reporting should be required to be made for that supplier.

12

How many Entries we can made for vendors in a single form ?

99 Entries

13

If as on 31.03.2020

No outstanding payment to MSME vendor, But there was delay in payment of some MSME vendor more than 45 days which has been paid on or before 31.03.2020.

Whether Company needs to give details of such invoices in the form?

Companies have to give details of outstanding payment to MSME vendor only on due date i.e. 31.03.2020

Payment has already been made to vendors before 31.03.2020, then company is not required to give details of such transaction in MSME1.

14

If entries are more than 99 then what?

Multiple forms can be filed, if entries are more than 99.

15

If Company is under IBC Process – Who is required to file?

Duty of Resolution Professional is to file it

(only Advisable)

16

Exemption to file MSME1 Form?

Medium Enterprises are not require to file.

17

Is their any additional fee (late fee) for delay filing of MSME Form?

No Fee

18

Is their any statutory filing fee for the filing of MSME Form

No Additional Fee

19

Processing Type of this E-form

The form will be processed in STP mode.

20

What is the Penalty for Non-Filing of Form MSME1?

Non-compliance will lead to punishment and penalty under the provision of the Companies Act. As per Penalty Provision of Section 405 (4) of the Companies Act, 2013

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION. THIS HAS BEEN SHARED FOR KNOWLEDGE PURPOSES ONLY.

File FORM GST PMT 09, to shift/transfer money available in Electronic Cash ledger, between various major and minor heads of GST

Taxpayers deposit money using challan and the paid amount gets credited in the particular head in the Electronic Cash ledger and the same can be utilized in settling liabilities of that head only. In case a taxpayer deposited any amount under a major head i.e. IGST, CGST, SGST/UTGST and Cess or minor head i.e. Tax, Interest, Penalty, Fee and Others, they can then utilize this amount for discharging their liabilities only under that major head and minor head.

Why File this form?

Sometimes, inadvertently, the taxpayer pays the amount under the wrong head. This money cannot be used to discharge the liabilities which may be due in another head. In such cases taxpayers can claim the refund of the amount. This was done by filing a refund application in FORM RFD-01 under the category “Excess balance in electronic cash ledger”. The process of filing refund claim and its disbursement can sometimes lead to blockage of funds for the taxpayer.

Form is now available on GST portal

It enables a taxpayer to make intra-head or inter-head transfer of amount available in Electronic Cash Ledger. A taxpayer can file GST PMT-09 for transfer of any amount of:

tax,

interest,

penalty,

fee

or others

available under one (major or minor) head to another (major or minor) head in the Electronic Cash Ledger.

Form GST PMT 09 provides flexibility to taxpayers to make multiple transfers from more than one Major/Minor head to another Major/Minor head if the amount is available in the Electronic Cash Ledger. To file Form GST PMT 09 taxpayers are required to login on GST portal with valid credentials and navigate to Services > Ledgers > Electronic Cash Ledger > File GST PMT 09 For Transfer of Amount option. After Form GST PMT 09 is filed:

ARN is generated on successful filing of Form GST PMT-09.

An SMS and an email is sent to the taxpayer on his registered mobile and email id.

Electronic Cash ledger will get updated after successful filing of Form GST PMT-09.

Filed form GST PMT 09 will be available for view/download in PDF format.

Tax Audit Report Deferment of GST Reporting & GAAR

Tax Audit is applicable on Every person which falls under any of the category of clause (a) to (e) of section 44AB of Income Tax Act. Accordingly he is required to get his accounts audited by an accountant and furnish the report on such audit. Tax Audit Forms are specified forms under rule 6G. The Forms are 3CA, 3CB, 3CD.

Tax Audit Report Deferment of GST Reporting & GAAR

On July, 2018 income tax department has introduced some new clauses in tax audit reporting i.e. in form 3CD. They were:

clause no 30C which was reporting regarding GAAR and

clause no 44 which required reporting pertaining to GST compliances.

Cloud Kitchen Glaiming Prominence amidst the Global Impasse. Let’s learn the basics of it.

The Universal crisis caused by COVID-19 has led to revolutionary changes in the way the restaurant industry operates. With restaurants and hotels being shut, delivery kitchens, ghost restaurants or cloud kitchens are increasingly becoming more relevant. Even five-star chains across the country are counting on delivery operations to survive the crisis. The Oberoi Bengaluru, the Taj Group of Hotels, The Park Hotel and many other top chains are delivering their most popular dishes to customers’ doorsteps in the wake of the ongoing nationwide lockdown. As India’s largest cities have been shut, there is likely going to be an even sharper dip in sales than seen in 2009.

The online food delivery market is projected to grow from a $35 billion industry to $365 billion by 2030, globally, and restaurants’ food delivery sales are growing more than three times the rate of on-premises revenue. Considering the high rentals and the increasingly tightening margins, restaurant operators are now closing up the storefront altogether and moving towards the more economically profitable, Cloud Kitchen business. Cloud kitchens thereby are becoming the need of the hour.

Here’s All You Need to Know to Run a Successful Food Delivery Business in India

What Is A Cloud Kitchen

A cloud kitchen, also known as the ghost kitchen, dark kitchen, virtual restaurant, is a delivery-only restaurant format that offers no dine-in facility. Cloud Kitchens accept orders online or through telephone. They primarily rely on online food aggregators such as Swiggy, Zomato, Ubereats and/or websites or mobile apps to accept online orders.

Cloud kitchens are considered as a low investment, low risk, yet high on profit format since the cost of setting up a cloud kitchen is significantly less as compared to a traditional dine-in or takeaway restaurant.

Cloud kitchens may have their online ordering website and online ordering app or accept orders through various food delivery platforms. Since the primary source of revenue for these internet restaurants is through various food ordering platforms such as Swiggy, FoodPanda, Zomato, etc., it is important to have a check-in system that keeps track of the deliveries and the volume the company generates from different platforms. This will save you the trouble of adding and measuring orders from various ordering systems at the end of each day.

The cloud kitchen business provides restaurateurs the opportunity to experiment with different formats and concepts, which has in turn, given birth to varied food delivery business models.

Starting A Cloud Kitchen Business

The low investment and risk, along with the ease in replicating and scaling the business make cloud kitchen, one of the most profitable food business formats in the food industry.

Here are the things you need to consider to open a cloud kitchen business in India.

(i) Location & Property

Undoubtedly, the location and property are the biggest differentiators between a traditional dine-in/takeaway restaurant and a cloud kitchen. A cloud kitchen does not require a location with a high cricket stadium and prime property position. Rather, it can very easily be set up in a 250-300 Sq Ft space since there is no Front of the House.

The cloud kitchen can be in a fairly inaccessible area, but with high customer demand, particularly for a specific kitchen. Residential areas, market backsides, unused parking lots make a perfect cloud kitchen spot. Instead, you can also go for a shared kitchen room, as this helps reduce initial investment.

(ii) Licenses

For many reasons, obtaining proper licenses and certification is important to open a cloud kitchen. Second, getting the licenses in order will save you from legal difficulties. Second, because consumers can not visit the outlet themselves to test for sanitation, food safety and preparation, proper licensing gives them a sense of satisfaction. You can promote these on your website and in your marketing campaigns to convince your customers that you prepare high-quality food.

The major licenses required to start a cloud kitchen business are FSSAI, GST Registration, NOC from the fire department, etc. To ensure that you have these in place before starting a food delivery business.

1. FSSAI: Food Safety and Standards Authority of India. FSSAI Licenses are mandatory for food-related business in India and must be obtained on behalf of the company and its owner. The license period can range from 1 year to 5 years and must be renewed before expiry. It’s also nice to mention FSSAI on the packaging and invoice to build confidence in our customers about our offers.

2. GST: GST registration is mandatory for any business in India and also it is recommended to file all the company related taxes timely. GST must be submitted weekly, quarterly and annually. GST also helps to procure licensed vendors, as it reduces the tax amount if all parties have a GST number. Upon obtaining a bank account, we will apply for a GST number.

3. Trade License: Every business will require to possess a trade license, and so does the cloud kitchen. This can be obtained from the local municipal office by furnishing all necessary documents. Apart from the cost, we might need some extra money to get the job finished. It is a one-time job and its kind of mandatory legal action.

4. Fire and Safety License: Now it’s not mandatory to start with, but it is great to save yourself from future troubles. This is part of the law, and fire and human health agreements are compulsory for any workplace.

5. Trademark registration is also very relevant for the cloud kitchen company because the idea of this company doesn’t allow the customer to step in, so the brand name of the business is the customer’s HERO. To protect the brand, the business owner must file trademark applications for the logo, name, wordmark consisting of different colors, patterns to create their unique identity on the market.

(iii) Kitchen Equipment & Packaging

The kitchen equipment depends on the type of cuisine you serve. The basic equipment required to start a cloud kitchen is – stove and oven, refrigerator, knives, etc. Here is a full list of kitchen equipment to operate a food delivery company.

The packaging is a vital part of running a food company. No matter how good the food is, it will end up destroying the whole consumer experience and giving the company a bad name. Packaging also depends on the food type. You’d need plastic containers, bottles, spoons, etc. to ensure proper food packaging.

Because there’s no House Front, you don’t need many people in your cloud kitchen. Only 2-3 people concentrated on preparing and distributing food, you can easily open a shop. When you have several kitchen brands, the same chef will prepare food for various brands. Starting with a small team is best, and you can recruit more staff as incoming order volumes increase.

(iv) Staff

Since there would be employees, to stay compliant, the business owner will take care of all relevant rules and laws. Professional tax registration, TDS, PF, Payroll and wage measurement becomes an essential and critical part of the business.

Salary Accounts, PF, etc: Unfortunately, this is the last thing most cloud kitchen owners do as the blue-collar employees aren’t too concerned about paying taxes and getting Provident Fund. When you’re in serious business with a long-term target, it’s important to start the cycle from day 1. It helps the team in the long run, building trust and friendly relationships with everyone.

Generating Online Orders And Marketing

Once you’ve set up the kitchen and staff, generate online orders for your cloud kitchen company.

Since a cloud kitchen doesn’t have a dine-in facility and relies solely on online and telephone food orders, spending on promoting the food delivery brand is important, at least in the initial days. Without a shop with no display boards and signage, online marketing is important in this situation.

a) Listing Your Cloud Kitchen On Online Food Aggregators

b) Promoting Your Cloud Kitchen On Online Aggregators

c) Social Media Marketing

d) Search Engine Optimization

e) Loyalty Programs And SMS & Email

Technology Needed For A Cloud Kitchen

Since a cloud kitchen typically relies on online food websites and mobile apps to generate orders, technology plays a crucial role in this business. A cloud kitchen requires an integrated online restaurant ordering system for accepting online orders and for aiding operations

While cloud kitchens involve low risk and high benefit, one should be alert to the competition ahead to make profits. A cloud kitchen will be the next theme. If you plan to grow your company or start a food channel, the cloud kitchen is the safer and wiser alternative considering that you keep it compliant.

Optimizing Food Delivery

Preparing food while generating orders is just one part of the food delivery business. The bigger challenge here is ensuring that your food is delivered to your customers on time and in perfect condition. You can either tie-up with third-party aggregators or logistics company or have your in-house food delivery fleet to fulfill orders.

Packaging plays a crucial role in ensuring a great delivery service. You need to ensure that the food has been packaged and handled well when it is delivered to the customer.

Conclusion:

Admittedly, the FnB industry seems to be all set to witness the second round of the Food Tech revolution. With the increasing internet penetration, the demand for food delivery will further continue to Tier 2 and Tier 3 cities.

While cloud kitchens involve low risk and high benefit, one should be alert to the competition ahead to make profits. A cloud kitchen will be the next theme. If you plan to grow your company or start a food channel, the cloud kitchen is the safer and wiser alternative considering that you keep it compliant.

DISCLAIMER- This write-up is based on the understanding and interpretation of the author and the same is not intended to be professional advice.

ICAI issues Advisory for members on Mentioning Fees in Advertisements

Certain concerns have been raised by members as to whether it is permissible to advertise the services rendered by them. They also want to know if mentioning that Professional Fees would be allowed.

As the members are aware, the advertisement of services is generally prohibited. Relevant provisions are:

Clauses (6) and (7) of Part-I of First Schedule to The Chartered Accountants Act, 1949.

However, in accordance with proviso to Clause (7), the advertisement of services has been permitted vide “write-up”. This is subject to Guidelines issued by the Council.

In accordance thereof, the Council had issued Advertisement Guidelines No.1-CA(7)/ Council Guidelines/ 01/ 2008, dated 14th May, 2008.

The members may thus advertise through a write up setting out their particulars or of their firms and services provided by them in conformity with the said Guidelines.

Legal Text

As per the said Guidelines, the “write up” refers to “writing of particulars according to the information given in the Guidelines setting out services rendered by the Members or firms and any writing or display of the particulars of the Member(s) in Practice or of firm(s) issued, circulated or published by way of print or electronic mode or otherwise including in newspapers, Journals, magazines and websites (in Push as well in Pull mode) in accordance with the Guidelines.”

Further, as per the said Guidelines, the “write-up” may include only the information expressly permitted under the said Guidelines.

It may be noted that mentioning professional Fees for the services rendered is not permitted entry.

As the members are further aware, the Website Guidelines of the Institute govern the rules for posting of particulars on the Website of Chartered Accountant(s) in practice and firm(s) of Chartered Accountants in practice. As per S.no. 6(ix) of the Website Guidelines :-

“………Names of clients and fee charged cannot be given.”

In view of the above provisions, it is clear that:

the mandate of posting any particular(s) on Firm’s own website or advertisement through write -up cannot exceed the authority granted respectively vide the Website Guidelines and Advertisement Guidelines of the Institute under any circumstances.

Accordingly, it is clarified that the quantum of Fees should not be mentioned by members in any Advertisement.

Filing and Viewing Form GST PMT09 | Filing Form GST PMT09

1. What is Form GST PMT09?

Form GST PMT09 enables any registered taxpayer to perform intra-head or inter-head transfer of amount as available in Electronic Cash Ledger. Thus, a registered taxpayer can now file Form GST PMT09 for transfer of any amount of tax, interest, penalty, fee or others, under one (major or minor) head to another (major or minor) head, as available in the Electronic Cash Ledger.

2. What is the use of Form GST PMT09?

In case, a taxpayer deposits any amount under a major head (Integrated tax, Central tax, State/UT tax, and Cess) or minor head (Tax, Interest, Penalty, Fee and Others), they can then utilize this amount for discharging their liabilities only under that major head and minor Head. So, they need to deposit amount only under a particular Head to meet their existing liabilities under that head (only).

Form GST PMT09 on the GST portal allows taxpayers to make Intra-head and Inter-Head transfer of funds, as available in their Electronic Cash Ledger. Thus this facility can be used to transfer any amount available in Electronic Cash Ledger as given below:

To transfer amount from minor head tax under major head cess to minor head interest under major head CGST or

To transfer amount from minor head Interest under major head IGST to minor head Tax under same major head IGST.

3. From where can I file Form GST PMT09?

To file Form GST PMT09, navigate to Services > Ledgers > Electronic Cash Ledger > File GST PMT09 For Transfer of Amount option.

4. Can I select more than one major/minor head while filing Form GST PMT09?

Yes, you can select more than one major/minor heads while transferring amount from one head to another, one at a time, while filing Form GST PMT09.

5. How can I add more than one major/minor head while filing Form GST PMT09?

You can add more than one major/minor head using Add Record option before clicking PROCEED TO FILE.

Previewing and Signing Form GST PMT09

6. Can I preview Form GST PMT09 before filing?

Yes, you can view/download Form GST PMT09 in PDF format before filing the same on the GST Portal.

Aadhaar updation is easy with 20000 Common Service Centre

– UIDAI allows Aadhaar updation facility through CSCs

– CSC’s – Common Service Centre

Ministry of Electronics & IT, vide press release 1618913 dated 28th April, 2020 has Announced major relief to Aadhaar holders, UIDAI allows Aadhaar updation facility through and 20,000 CSCs to offer this service to citizens.

In view of the situation arising due to COVID-19 pandemic and extended lockdown period, this is a big relief to the Aadhaar Holders who wants updation.

Aadhaar updation is easy with 20000 Common Service Centre

Key Highlights:

1. UIDAI has allowed the Common Service Centre, an SPV under the Ministry of IT and Electronics, to begin the Aadhaar updation facility at their 20,000 CSCs.

2. Only those CSCs which operate as Banking Correspondents (BCs).

3. CSC VLEs has to start the Aadhaar work with responsibility and as per instructions issued by UIDAI.

4. this facility will help a large no of rural citizens to get Aadhar services closer to their place of residence.

5. Deadline:

UIDAI has set June deadline for the commencement of the work after CSCs with banking facilities upgrade their required infrastructure and get other necessary approvals.

6. It would further strengthen the efforts of achieving the goals of “Digital India”.

7. 20,000 additional centers available to update Aadhaar, the users particularly in rural areas need not visit Aadhaar centres in bank branches or Post Offices for this work.

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION.

About Author:

CS Lalit Rajput (PARTNER AT XCEDE CONSULTECH LLP) AND CAN BE REACHED AT consultech@xcede.in / +91 8802581290

Employees’ Provident Fund Organization, India, Ministry of Labour & Employment, Government of India has issued FREQUENTLY ASKED QUESTIONS ON EPF ADVANCE TO FIGHT COVID-19 PANDEMIC Dated 26/04/2020.

FAQ’s ON EPF ADVANCE TO FIGHT COVID-19 PANDEMIC

20 FAQ’s ON EPF ADVANCE TO FIGHT COVID19 PANDEMIC

Q1: What is the process for change in name on marriage of a woman member against UAN when changes are made in Aadhaar?

Ans. The name change process if the Aadhar data is changed is similar to other change requests. Member has to apply online and employer will digitally approve the request. The correction request can be submitted online or offline (joint request) along with a copy of the marriage certificate or such other documents which can prove that only the name of the member has changed from before marriage. Documents like school records containing Father’s name and Date of birth or PAN taken before marriage etc. are a useful to show that only name has changed after marriage.

Q2: The link ‘Know your UAN’ is not available on unified portal. Is approaching employer for this the only option?

Ans. Visit unified member portal at https://ift.tt/2upHdS5

• Select Member ID, Aadhaar or PAN

• Enter details such as name, date of birth, mobile number and e-mail id as per EPFO records

• Click on the “Get Authorization Pin” option

• A Pin will be sent to your mobile number registered with EPFO

• Enter the Pin and your UAN will be sent to the mobile number

Q.3: I have already applied advance for illness in March 2020 which is pending. I want to apply for advance to fight COVID pandemic now. What should I do?

Ans. During pendency of any other advance, the application for COVID-19 claim is permitted.

Q.4: KYC updation needs approval by Employer by using his DSC. When Establishment is closed and there is no Employer, who is to approve the same?

Ans. The approval of KYC by employer is an online facility which can be operated irrespective of the location. Please request the employer to approve the KYC.

Q5: For filing of claim a copy of cheque with name of member or copy of pass book is to be uploaded. Member does not have name on his cheque leaf and it is now difficult to get it from Bank. Even going to bank and getting an attested copy of bank statement is not easy as Banks are far away. What is the other option that can be made available?

Ans. As per prevailing instructions it is mandatory to upload a cheque leaf containing the printed name of the member, or the first page of the bank Passbook or bank statement containing the name, account number and IFSC. This is required to ensure that the bank account number uploaded in the KYC is correct and erroneous payments are avoided.

Q.6: I have worked for two companies and working in third one now. How to get PF accumulations of earlier companies transferred to present one so that I can file claim for COVID advance?

Ans. In case the name, date of birth and gender in all the accounts is same, the member can apply online for transfer through his login. The present UAN should be validated with Aadhar. In case of difference once he gets the basic details corrected in other accounts, he can apply online.

Q.7: You claim to settle COVID advance claims within 72 hours? It is over 4 days when I applied. I have still not received the money in my bank account. Why?

Ans. EPFO settles claims for availing advance to fight COVID-19 pandemic within 03 working days. After processing of the claims, cheque is sent to the bank for crediting amount to bank account of the claimant. Bank usually take additional one to three working days to credit advance in your bank account.

Q.8: I live in city A and work in City B. However, Head Office of my company is in city C. Which EPF office has to be contacted for any matter?

Ans. You should approach EPF office where your establishment is registered. To find concerned EPF office where your establishment is registered visit

• Fill in establishment PF code or name

• Enter captcha and click on search

• Establishment details will appear in tabular format.

• Confirm the establishment Id, Name and Address and in column four EPF office name is provided.

Q.9: I need to contact the EPF office through email or phone. Please provide me contact details of EPF office.

Ans. Please visit https://www.epfindia.gov.in/site_en/Contact_us.php. Click on the Zonal office under which EPF Regional/ District office falls>> Click on concerned Regional/District office to get their contact details.

Q.10: I have applied for COVID epidemic advance. How to check status of my claim?

Q.11: I work in a company in Jammu which was covered under J&K PF Act. Since last year this company is covered under Employees Provident Fund Act, 1952. Can I file claim for fighting COVID pandemic?

Ans. Yes member can apply for advance from the contributions received by EPFO.

Q.12: Why your toll-free number is not accessible?

Ans. Services will be resumed shortly. Pending resumption of services, you may contact us on our Facebook and twitter handle “socialepfo”. You can raise your grievances at epfigms.gov.in.

Q.13: I have a balance of Rs 100000 in my PF account and applied for Rs 75000 advance for COVID. At the rate of 75%, I should get Rs. 75000. Why a much lesser amount has been credited to my account?

Ans. The 75% of the amount standing to your credit is maximum permissible limit and the same is applicable if it is lesser than basic wages and dearness allowances for three months. If 75% of the balance is more than three months wages, advance equal to three months wages (Basic+DA) is sanctioned as per the rules. If your monthly wage is Rs.20000, the entitled advance amount is Rs 60000 only. If the monthly wages are Rs 30000, the amount of advance will be restricted to Rs.75000.

Q.14: I am not able to file COVID claim. Please help me.

The process is also noted below:

a. Login to Member Interface of Unified Portal (https://unifiedportalmem.epfindia.gov.in/memberinterface)

b. Go to Online Services>>Claim (Form-31,19,10C & 10D)

c. Enter your Bank Account and verify

d. Click on “Proceed for Online Claim”

e. Select PF Advance (Form 31) from the drop down

f. Select purpose as “Outbreak of pandemic (COVID-19)” from the drop down

g. Enter amount required and Upload scanned copy of cheque and enter your address

h. Click on “Get Aadhaar OTP”

i. Enter the OTP received on Aadhaar linked mobile.

j. Claim is submitted

Q.15: I have balance available in my account. How many times I can get advance to fight COVID?

Ans. The advance to fight COVID-19 pandemic is available once only.

Q.16: What is the last date for applying COVID advance?

Ans. The facility for availing advance to fight COVID-19 pandemic will be available till the pandemic prevails.

Q.17: I have two different UANs. The first UAN is linked with one PF member ID and the second UAN is linked with 2 different member IDs. Can I avail COVID advance benefits? How to get maximum benefit in this case.

Ans. Yes. In order to get maximum benefits, you are requested to transfer all the previous services (linked with multiple member IDs) to the latest member ID. This can be done by filing a transfer claim. Once the service is successfully transferred your entire PF corpus will reflect against the latest member ID. Subsequently you can file COVID advance claim to reap maximum benefit.

Q.18: My COVID claim has been rejected due to member details mismatch. How can I rectify this issue?

Ans. You can update your member details by logging into member e-sewa portal available at

Once the details are updated you can file the claim once again.

Q.19: How can I file COVID claim through UMANG app?

Ans: Steps are as follows:

Step 1: Open Umang app Step 2: Select EPFO

Step 3: Select “Request for Advance (COVID-19)”

Step 4: Enter your UAN details and click on ‘Get OTP’ to get one-time password. Use this OTP to login in your account.

Step 5: Enter the OTP and click on login. Once you are logged in you are required to enter the last four digits of your bank account and select the member ID from the drop-down menu. Click on “Proceed for claim”

Step 6: Enter your address. Click on ‘Next’.

Step 7: Upload the cheque image with your account number and name printed on it. Once all the details are entered, your claim will be successfully filed.

Q.20: I have left the service but not yet availed the final PF withdrawal benefits. Can I still avail the COVID advance?

Ans. Yes. COVID advance can be filed by any PF subscriber. Since you have not withdrawn your PF funds you are still a PF member.

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION.

THIS HAS BEEN SHARED FOR KNOWLEDGE PURPOSES ONLY.

About Author:

CS Lalit Rajput, Partner at Xcede Consultech LLP)

Email id lalitrajput537@gmail.com / +91 8802581290

SEBI REDUCES BROKER TURNOVER FEES AND FILING FEES FOR ISSUERS

• OVERVIEW

Securities and Exchange Board of India (SEBI) vide Press Release No. PR No.: 24/2020 issued and publish dated 27th April, 2020, has published SEBI reduces Broker turnover fees and filing fees for issuers”

KEY HIGHLIGHTS

• In its continuing efforts to help market participants to tide over challenges due to COVID 19, Securities and Exchange Board of India (SEBI) has decided to reduce broker turnover fees and filing fees on offer documents for Public issue, Rights issue and Buyback of shares.

• The broker turnover fee will be reduced to 50% of the existing fee structure for the period June 2020 to March 2021. The benefit of the above reduction in fees will automatically be passed on to the investors as well.

• Filing fees on offer documents for Public issue, Rights issue and Buyback of shares will be reduced to 50% of the existing fee structure. This will be effective for documents filed from June 1, 2020 to December 31, 2020.

CA Deepak Gupta & CA Sangam Agarwal are happy to invite you for 3 Days online webinar based course on Advance Level ICAI Code of Ethics by renowned faculties.

Key Highlights of RBI Liquidity Support to Mutual Funds due to COVID19 – RBI Announces Rs. 50,000 crore Special Liquidity Facility

RESERVE BANK OF INDIA, vide press release 2019-2020/2276 dated 27th April, 2020 has Announces Rs. 50,000 crore Special Liquidity Facility for Mutual Funds (SLF-MF) In view of the situation arising due to COVID-19 pandemic and extended lockdown period.

Why RBI Announces such Measure:

• Heightened volatility in capital markets

• liquidity strains on mutual funds (MFs),

• redemption pressures related to closure of some debt MFs

• potential contagious effects

• to mitigate the economic impact of COVID-19 and preserve financial stability

Key Highlights of RBI Liquidity Support to Mutual Funds due to COVID19

Scheme Applicability:

The scheme is available from today i.e., April 27, 2020 till May 11, 2020 or up to utilization of the allocated amount, whichever is earlier.

Key Highlights:

• With a view to easing liquidity pressures on MFs, it has been decided to open a special liquidity facility for mutual funds of `50,000 crore

• Under the SLF-MF, the RBI shall conduct repo operations of 90 days tenor at the fixed repo rate

• banks can submit their bids to avail funding on any day from Monday to Friday (excluding holidays).

• The Reserve Bank will review the timeline and amount, depending upon market conditions.

• Liquidity support would be eligible to be classified as held to maturity (HTM) even in excess of 25% of total investment permitted to be included in the HTM portfolio.

Note: Support extended to MFs under the SLF-MF shall be exempted from banks’ capital market exposure limits.

Utilization of Funds

Funds availed under the SLF-MF shall be used by banks exclusively for meeting the liquidity requirements of MFs by

(1) extending loans, and

(2) undertaking outright purchase of and/or repos against the collateral of investment grade corporate bonds, commercial papers (CPs), debentures and certificates of Deposit (CDs) held by MFs

How to Avail Benefits:

• This special repo window will be available to all LAF eligible banks and can be availed only for on-lending to Mutual funds

• The eligible banks may place their bids electronically on the CBS platform between 9 AM and 12.00 Noon every day

• The bidding process, settlement and reversal of SLF-MF repo would be similar to the existing system being followed in case of LAF/MSF.

• In case of over-subscription of the notified amount on any given day, the allotment will be done on pro-rata basis.

• The minimum bid amount would be Rupees one crore and multiples thereof. The allotment would be in multiples of Rupees one crore.

• A market participant can place bids of amount less than or equal to the notified amount of the issue announced on a given day.

• The eligible collateral and the applicable haircuts will remain the same as applicable for LAF.

Note: While banks will decide the tenor of lending to /repo with mutual funds, the minimum tenor of repo with RBI will be for a period of three months.

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION.

About Author:

CS Lalit Rajput (PARTNER AT XCEDE CONSULTECH LLP) AND CAN BE REACHED AT consultech@xcede.in / +91 8802581290

24 FAQ’S ON SCOPE / ELIGIBILITY OF DIRECT TAX VIVAD SE VISHWAS ACT 2020

Government of India, Ministry of Finance, Department of Revenue, Central Board of Direct Taxes vide Circular No. 9/2020, F. No. IT(A)/1/2020-TPL, dated 22nd April, 2020 has issued Clarifications on provisions of the Direct Tax Vivad se Vishwas Act, 2020 and FAQ’s on Scope / Eligibility of Direct Tax Vivad Se Vishwas Act, 2020.

This act was announced to provide for dispute resolution in respect of pending income tax litigation.

24 FAQ’S ON SCOPE / ELIGIBILITY OF DIRECT TAX VIVAD SE VISHWAS ACT 2020

24 FAQ’S ON SCOPE / ELIGIBILITY

Q1. Which appeals are covered under the Vivad se Vishwas ?

Answer: Appeals pending before the appellate forum [Commissioner (Appeals), Income lax Appellate Tribunal (ITAT), High Court or Supreme Court], and writ petitions pending before High Court (HC) or Supreme Court (SC) or special leave petitions (SI,Ps) pending before SC as on the 31st day of January, 2020 (specified date) are covered. Cases where the order has been passed but the time limit for filing appeal under the Income-tax Act, 1961 (the Act) against the order has not expired as on the specified date arc also covered. Similarly, cases where objections filed by the assessee against draft order are pending with Dispute Resolution Panel (DRP) or where DRP has given the directions but the Assessing Officer (AO) has not yet passed the final order on or before the specified date arc also covered. Cases where revision application under section 264 of the Act is pending before the Principal Commissioner or Commissioner are covered as well. Further, where a declarant has initiated any proceeding or given any notice for arbitration, conciliation or mediation as referred to in section 4 of the Bill is also covered.

Q2. If there is no appeal pending but the case is pending in arbitration, will the taxpayer he eligible to apply under Vivad se Vishwas? If yes what will he the disputed tax?

Answer: An assessee whose case is pending in arbitration is eligible to apply for settlement under Vivad se Vishwas even if no appeal is pending. In such case assessee should fill the relevant details applicable in his case in the declaration form. The disputed tax in this case would be the tax (including surcharge and cess) on the disputed income with reference to which the arbitration has been filed.

Q3. Whether Vivad se Vishwas can he availed for proceedings pending before Authority of Advance Ruling (AAR)? If a writ is pending against order passed by AAR in a HC will that case he covered and how disputed tax to he calculated?

Answer: Vivad se Vishwas is not available for disputes pending before AAR. However, if the order passed by AAR has determined the total income of an assessment year and writ against such order is pending in HC, the appellant would he eligible to apply for the Vivad se Vishwas. The disputed tax in that case shall he calculated as per the order of the AAR and accordingly, wherever required, consequential order shall be passed by the AO. However, if the order of AAR has not determined the total income, it would not be possible to calculate disputed tax and hence such cases would not he covered. To illustrate, if AAR has given a ruling that there exists Permanent Establishment (PE) in India but the AO has not yet determined the amount to be attributed to such PE, such cases cannot be covered since total income has not yet been determined.

Q4. An appeal has been filed against the interest levied on assessed tax; however., there is no dispute against the amount of assessed tax. Can the benefit of the Vivad se Vishwas be availed?

Answer: Declaration covering disputed interest (where there is no dispute on tax corresponding to such interest) are eligible under Vivad se Vishwas. It may be clarified that if there is a dispute on tax amount, and a declaration is filed for the disputed tax, the full amount of interest levied or leviable related to the disputed tax shall be waived.

Q5. What if the disputed demand including interest has been paid by the appellant while being in appeal?

Answer: Appeals in which appellant has already paid the disputed demand either partly or fully are also covered. If the amount of tax paid is more than amount payable under Vivad se Vishwas, the appellant will be entitled to refund without interest under section 244A of the Act.

Q6. Can the benefit of the Vivad se Vishwas be availed, if a search and seizure action by the Income-tax Department has been initiated against a taxpayer?

Answer: Case where the tax arrears relate to an assessment made under section 143(3) or section 144 or section I53A or section 153C of the Act on the basis of search initiated under section 132 or section 132A of the Act are excluded if the amount of disputed tax exceeds five crore rupees in that assessment year.

Thus, if there are 7 assessments of an assessee relating to search & seizure, out of which in 4 assessments, disputed tax is five crore rupees or less in each year and in remaining 3 assessments, disputed tax is more than five crore rupees in each year, declaration can be filed for 4 assessments where disputed tax is five crore rupees or less in each year.

Q7. If assessment has been set aside for giving proper opportunity to an assessee on the additions carried out by the AO. Can lie avail the Vivad se Vishwas with respect to such additions?

Answer: If an appellate authority has set aside an order (except where assessment is cancelled with a direction that assessment is to be framed de novo) to the file of the AO for giving proper opportunity or to carry out fresh examination of the issue with specific direction, the assessee would be eligible to avail Vivad se Vishwas. however, the appellant shall also be required to settle other issues, if any, which have not been set aside in that assessment, and in respect of which either appeal is pending or time to file appeal has not expired. In such a case disputed tax shall be the tax (including surcharge and cess) which would have been payable had the addition in respect of which the order was set aside by the appellate authority was to be repeated by the AO.

In such cases while filling the declaration in Form No 1, the declarant can indicate in the appropriate schedule that with respect to the set-aside issues the appeal is pending with the Commissioner (Appeals).

Q8. Imagine a case where an appellant desires to settle concealment penalty appeal pending before CIT (A), while continuing to litigate quantum appeal that has travelled to higher appellate forum. Considering these are two independent and different appeals, whether appellant can settle one to exclusion of others? If yes, whether settlement of penalty appeal will have any impact on quantum appeal?

Answer: If both quantum appeal covering disputed tax and appeal against penalty levied on such disputed tax for an assessment year are pending, the declarant is required to file a declaration form covering both disputed tax appeal and penalty appeal. However, he would be required to pay relevant percentage of disputed tax only. Further, it would not be possible for the appellant to apply for settlement of penalty appeal only when the appeal on disputed tax related to such penalty is still pending.

Q9. Is there any necessity that to qualify under the Vivad se Vishwas, the appellant should have tax demand in arrears as on the date of filing declaration?

Answer: Vivad se Vishwas can be availed by the appellant irrespective of whether the tax arrears have been paid either partly or fully or are outstanding.

Q10. Whether 234E and 234F appeals are covered?

Answer: If appeal has been filed against imposition of fees under sections 234E or 234F of the Act, the appellant would be eligible to file declaration for disputed fee and amount payable under Vivad se Vishwas shall be 25% or 30% of the disputed fee, as the case may be.

If the fee imposed wider section 234E or 234F pertains to a year in which there is disputed tax, the settlement of disputed tax will not settle the disputed fee. If assessce wants to settle disputed fee, he will need to settle it separately by paying 25% or 30% of the disputed fee, as the case may be.

Q11. In case where disputed tax contains qualifying tax arrears as also non-qualifying tax arrears (such as, tax arrears relating to assessment made in respect of undisclosed foreign income): (i) Whether assessee is eligible to the Vivad se Vishwas itself? (ii) If eligible, whether quantification of disputed tax can exclude/ignore non-qualifying tax arrears?

Answer: If the tax arrears include tax on issues that are excluded from the Vivad se Vishwas, such cases are not eligible to File declaration under Vivad se Vishwas. There is no provision under Vivad se Vishwas to settle part of a pending dispute in relation to an appeal or writ or SIT for an assessment year. For one pending appeal, all the issues are required to be settled and if any one of the issues makes the declaration invalid, no declaration can be filed.

Q12. If a writ has been.filed against a notice issued under section 148 of the Act and no assessment order has been passed consequent to that section 148 notice, will such case be eligible to file declaration under Vivad se Vishwas?

Answer: The assessee would not be eligible for Vivad se Vishwas as there is no determination of income against the said notice.

Q13. With respect to interest under section 234A, 234B or 234C, there is no appeal but the assessee has filed waiver application before the competent authority which is pending as on 31 Jan 2020? Will such cases be covered under Vivad se Vishwas?

Answer: No, such cases are not covered. Waiver applications are not appeal within the meaning of Vivad se Vishwas.

Q14. Whether assessee can avail of the Vivad se Vishwas for some of the issues and not accept other issues?

Answer: Refer to answer to question no 11. Picking and choosing issues for settlement of an appeal is not allowed. With respect to one order, the appellant must chose to settle all issues and then only he would be eligible to file declaration.

Q15. Will delay in deposit of TDS/TCS he also covered under Vivad se Vish was?

Answer: The disputed tax includes tax related to tax deducted at source (TDS) and tax collection at source (TCS) which are disputed and pending in appeal. however, if there is no dispute related to TDS or TCS and there is delay in depositing such TDS/TCS, then the dispute pending in appeal related to interest levied due to such delay will be covered under Vivad se Vishwas.

Q16. Are cases pending before DRP covered? What if the assessee has not filed objections with DRP and the AO has not yet passed the final order?

Answer: Yes, a person who has filed his objections before the DRP under section 1440 of the Act and the DRP has not issued any direction on or before the specified date as well as a person in whose case the DRY has issued directions but the AO has not passed the final assessment order on or before the specified date, is eligible under Vivad se Vishwas.

It is further clarified that there could be a situation where the AO has passed a draft assessment order before the specified date. Assessee decides not to file objection with the DRP and is waiting for final order to be passed by the AO against which he can file appeal with Commissioner (Appeals). In this situation even if the final assessment order is not passed on or before the specified date, the assessee would be considered as the appellant and would be eligible to settle his dispute under Vivad se Vishwas. Disputed tax in such case would be computed based on the draft order. In the declaration in Form No 1, the declarant in this situation should indicate in the appropriate schedule that time to file objection with DRI’ has not expired.

Q17. If CIT (Appeals) has given an enhancement notice, can the appellant avail the Vivad se Vishwas after including proposed enhanced income in the total assessed income?

Answer: The amendment proposed in the Vivad se Vishwas allows the declaration even in cases where CIT (Appeals) has issued enhancement notice on or before 31″ January, 2020. However, the disputed tax in such cases shall be increased by the amount of tax pertaining to issues for which notice of enhancement has been issued.

Q18. Are disputes relating to wealth tax, security transaction tax, commodity transaction tax and equalisation levy covered?

Answer: No. Only disputes relating to income-tax are covered.

Q19. The assessment order under section 143(3) of the Act was passed in the case of an assessee for the assessment year 2015-16. The said assessment order is pending with 1TAT. Subsequently another order under section 147/143(3) was passed for the same assessment year and that is pending with CIT (Appeals)? Could both or one of the orders be settled under Vivad se Vishwas?

Answer: The appellant in this case has an option to settle either of the two appeals or both appeals for the same assessment year. I f he decides to settle both appeals then he has to file only one declaration in Form No 1. The disputed tax in this case would he the aggregate amount of disputed tax in both appeals.

Q20. In a case there is no disputed tax. However, there is appeal for disputed penalty which has been disposed of by CIT (Appeals) on 1st January 2020. Time to file appeal in ITAT against the order of Commissioner (Appeals) is still available but the appeal has not yet been filed. Will such case he eligible to avail the benefit?

Answer: Yes, the appellant in this case would also be eligible to avail the benefit of Vivad se Vishwas. In this case, the terms of availing Vivad se Vishwas in case of disputed penalty/interest/fee are similar to terms in ease of disputed tax. Thus, if the time to file appeal has not expired as on specified date, the appellant is eligible to avail benefit of Vivad se Vishwas. In this case the declarant should indicate in the declaration Form No 1, in the appropriate schedule, that time limit to file appeal in ITAT has not expired.

Q21. In a case ITAT has quashed the assessment order based on lack of jurisdiction by the AO. The department has filed an appeal in IIC which is pending. Is the assessee eligible to settle this dispute under Vivad se Vishwas and if yes how disputed tax be calculated as there is no assessment order?

Answer: The assessee in this case is eligible to settle the department appeal in TIC. The amount payable shall be calculated at half rate of 100%, 110%, 125% or 135%, as the case may be, on the disputed tax that would be restored if the department was to win the appeal in HC

Q22. In the case of an assessee prosecution has been instituted and is pending in court. Is assessee eligible for the Vivad se Vishwas? Further, where the prosecution has not been instituted but the notice has been issued, whether the assessee is eligible for Vivad se Vishwas?

Answer: Where only notice for initiation of prosecution has been issued without prosecution being instituted, the assessee is eligible to file declaration under Vivad se Vishwas. however, where the prosecution has been instituted with respect to an assessment year, the assessee is not eligible to file declaration for that assessment year under Vivad se Vishwas, unless the prosecution is compounded before filing the declaration.

Q23. If the due date of filing appeal is after 31.1.2020 the appeal has not been filed, will such: case be eligible for Vivad se Vishwas?

Answer: Yes

Q24. If appeal is filed before High Court and is pending for admission as on 31.1.2020, whether the case is eligible for Vivad se Vishwas?

IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USE OF THIS INFORMATION.

About Author:

CS Lalit Rajput (PARTNER AT XCEDE CONSULTECH LLP) AND CAN BE REACHED AT lalitrajput537@gmail.com / +91 8802581290