Income Tax return Forms for Financial Year 2019-2020 notified

Please note that MINISTRY OF FINANCE has notified, Income Tax return Forms for Financial Year 2019-2020 or Assessment Year 2020-2021 notified.

Form ITR-1 or Sahaj: [For individuals being a resident (other than not ordinarily resident) having total income upto Rs.50 lakh, having Income from Salaries, one house property, other sources (Interest etc.), and agricultural income upto Rs.5 thousand] [Not for an individual who is either Director in a company or has invested in unlisted equity shares]

Form ITR-2: [For Individuals and HUFs not having income from profits and gains of business or profession]

Income Tax return Forms for Financial Year 2019-2020 notified

Form ITR-3: [For individuals and HUFs having income from profits and gains of business or profession]

Form ITR-4 or Sugam: [For Individuals, HUFs and Firms (other than LLP) being a resident having total income upto Rs.50 lakh and having income from business and profession which is computed under sections 44AD, 44ADA or 44AE] [Not for an individual who is either Director in a company or has invested in unlisted equity shares]

New Rule 114-I along with form 26AS has been notified by CBDT to share annual financial information in respect of each taxpayer not only of taxes paid by of TDS/TCS or otherwise . Now this new form 26AS will also provide information in respect of specified financial transactions which include transactions of purchase/ sale of goods, property, services, works contract, investment, expenditure,taking or accepting any loan or deposits of such value as may be prescribed but not less than of Rs 50,000. Also information about income tax demand, refund, proceedings pending and proceedings completed which may include assessment, reassessment under section 148,153A 153C , revision , appeal will also be shared in this form 26AS.

Analysis

Further an enabling provision has been notified empowering the CBDT to authorise DG Systems or any other officer to upload in this form 26A/, information received from any other officer, authority under any law. Thus any adverse action initiated or taken or found or order passed under any other law such as custom , GST , Benami Law etc. including information about Turnover , import , export etc. will also be put in this form 26AS so that not only the concerned taxpayer but also all the Income Tax authorities will know and have access to such information. This form 26AS will also provide information received by Tax Deptt from any other country under the treaty /exchange of information about income or assets of the taxpayer located outside India. This form will also have mobile no, email I’d and Aadhar no.of the taxpayer.

New Rule 114-I along with form 26AS has been notified by CBDT

Moreover information on this form 26AS will not be a one time affair at year end . This will be a live 26AS ,as this will be updated regularly within 3 months from the end of the month in which such information is received.

Conclusion

Thus form 26AS will now be a complete profile of the taxpayer for that particular year as against earlier form 26AS which just provided the information about taxes paid by way of TDS/TCS or self assessing.

The implication of this new form 26AS will be that banks , financial institutions or any other authority or customer , buyer etc. while carrying out due diligence of the person/ corporate concerned will now ask for form 26AS so as to be sure that there are not any major issues about such person/corporates . This will now make difficult for any taxpayer to hide information from any bank / financial institution/ authority about any proceedings against under any law or tax demand , tax disputes etc .

NRI Planning to Come Back to India for Good – Check Points Explained

Authored by CA CS Ajay R. Vaswani B.Com, LCS, FCA, DISA (ICAI)

An individual chooses to stay outside India and work day and night away from family and social circle for years and decades. The intentions are to have better living standards by earning more, looking at opportunities available vis-a-vis in his own home country. The apparent intentions of a person looking to become Non-Resident Indian (NRI) is to have a better capability to deliver for family needs, education of children and have a good and comfortable post-retirement life.

After having lived for years outside India being NRI, the moment of thought is sure to pop up, thinking let us go back to India. It is the call of the motherland, to take a break from work and now to enjoy post-retirement life.

The second thought triggers, is that there is a lot to be done before going back to India. The planning and preparations take a lot of energy and time, especially when they are planning for going back for good.

One of the points of consideration or botheration is taxation. It is essential to know and to be aware of the implications that would arise post moving back to India. The laws of the land, the compliances and concerns that are required to be addressed and all. That too, it is important when someone is planning to move back to India has had not complied to filing tax returns for years for reasons like no tax liability, awareness, the requirement of the case, or having been used to living in countries having no direct tax liability as such on income earned like in UAE or other gulf countries. People out there are habitual because of the prevailing tax systems and being in their comfort zone.

NRI Planning to Come Back to India for Good – Check Points Explained

The points that need to be assessed have been discussed in brief point by point:

1. Residential Status:

Taxation of an Individual in India is based on an assessment method followed looking upon the number of days stayed in India and outside India. There are two acts, which govern the taxation and investment provisions for NRIs, i.e. Income Tax Act, 1961 and Foreign Exchange Management Act, 1999.

As per the Income Tax Act, in all, there are three major classifications of the status of an individual, which define him are Resident, Non-Resident and Resident But Not Ordinary Resident (RNOR). Based on the status, taxation of various source of income is defined.

The taxability and levy of Income Tax in India, based on the residential status as discussed above, is further based on two concepts, i.e. Accrual of Income and Receipt of Income along with deemed concept.

The following table defines the status and taxation system:

So, looking at the mechanism a system prevailing, it is advisable to have a planned and calculated strategy in place with regards to the number of days to be stayed outside India before coming back to India. A day here and there can change the tax liability on the assessee having a direct monetary impact.

2. Taxation of Foreign Income / Foreign Assets:

As referred in the above-mentioned table, the taxation of foreign income depends upon the residential status continued to be maintained. For NRI and RNOR, purely foreign income continue to be exempt. Once an individual becomes an Ordinary Resident of India, His or Her Global Income is Taxable. FCNR or NRE accounts are tax-free for RNOR. End of Service benefit would also be treated to be tax-free in similar lines.

Under FEMA, Non-Resident Indians who return to India can own, hold, invest, or transfer their assets not located in India. However, this is only applicable if the assets were acquired when the NRI was outside India. FEMA also allows NRIs to make transactions and even earn foreign income through EEFCA (Exchange Earners Foreign Currency Account) and RFC (Resident Foreign Currency) accounts.

3. Bank Accounts:

Another set of big questions list comes upon what happens to the bank accounts opened like NRO, NRE, FCNR or Foreign Currency Bank Accounts, including salary account. Upon expiry of VISA and change in residency status, bank accounts have to be updated accordingly. Summing up in easy words:

NRO: Is converted back into regular resident saving account. Application needs to be done either online or offline to the concerned bank along with the submission of necessary documents.

NRE and FCNR: Can be converted into RFC, i.e. Resident Foreign Currency Account, where two categories of accounts can be maintained like saving account and fixed deposit account where an individual can continue holding foreign currency. It can be maintained in acceptable currencies like USD or GBP. However, observation has been few nationalised bank offer only in the form of FD account. Again subject to the documents and condition is individual should have been NRI in the past.

Foreign Bank Accounts: Can be continued, subject to holding VISA and complying with other country bank norms.

Crux: Be Tax-Planned Before Moving to India

Having a proper tax-planning is one of the most critical considerations for NRIs willing to come back to India for good and have a peaceful retirement life.

DISCLAIMER

The information contained herein is generic and is meant for educational purposes only. Nothing here is to be construed as an advice. Readers are advised to exercise discretion and should seek independent professional advice before making any decision.

The Author is available for further queries on Email: contact@cafornri.com

Studycafe free upcoming webinar Series! Join for Free

Friends!

Team Studycafe is happy to invite you for a Zoom Webinar sessions on below mentioned Topics. Here is the list of our upcoming webinar Series. The webinar will be taken up by reknown Authors. Join our series for free and update your skills in this time of COVID-19. We will keep updating this page once our next dates will ge finalized. So keep visiting this page.

Studycafe free upcoming webinar Series! Join for Free

10 Days Online GST Certification course is also Starting form 1st June 2020. For more information of the same click here

Once Successfully registered you will receive an email having webinar ID & password. Webinar ID and Password will be applicable only to this webinar.

500 Seats FCFS Basis Applies. If you are not able to Login due to limited seats you can access the live Webinar on Youtube Page & Facebook Page Link of Youtube Page:

1. Are monetary gifts received by an individual or Hindu Undivided Family (HUF) taxable?

Ans. If the following conditions are satisfied then any sum of money received (i.e, monetary gift may be received in cash, cheque, draft, etc.) by an individual/ HUF will be charged to tax (*):

• Sum of money received without consideration

• The aggregate value of such sum of money received during the year exceeds Rs. 50,000.

(*) Refer next FAQ for situations in which sum of money received by an individual or HUF is not charged to tax, i.e., monetary gift is not charged to tax.

2. Are there any cases in which sum of money received without consideration, i.e., monetary gift received by an individual or HUF is not charged to tax?

Ans. If any sum of money is received on or after 01/10/2009 by an Individual or HUF without any consideration and the aggregate value of which exceeds Rs. 50,000 during the previous year, then the whole of the aggregate value of such sum is chargeable to tax.

However, in the following cases nothing will be charged to tax in respect of any sum of money received by an Individual or HUF without any consideration, if the same is received:

• from any relative or by a HUF from its members; or

• on the occasion of the marriage of the individual; or

• under a will/ by way of inheritance; or

• in contemplation of death of the payer or donor as the case may be; or

• from a local authority as defined under Explanation to clause (20) of section 10 of the Income-tax Act, 1961; or

• from any fund, foundation, university, other educational institution, hospital or other medical institution, any trust or institution referred to in section 10 or

• by any fund, trust, institution, any university, other educational institution, any hospital, other medical institution referred to in sub-clause (iv) or sub-clause (v) or sub-clause (vi) or sub-clause (via) of clause (23C) of section 10; or (applicable if the property is received on or after 1st day of April, 2017)

• from or by a trust or institution registered under section 12AA; or

• from or by a trust or institution registered under section 12A; or (applicable if the property is received on or after 1st day of April, 2017)

• by way of transaction not regarded as transfer under section 47(i)/(iv)/(v)/(vi)/(via)/ (viaa)/(vib)/ (vic)/ (vica)/ (vicb)/ (vid)/ (vii)

• from an Individual by a trust created or established solely for the benefit of relative of the Individual. (applicable if the property is received on or after 1st day of April, 2017)

• from such of person’s and subject to such conditions as may be prescribed.

3. Gift received from relatives are exempt from tax. Who will be considered as relative for the purpose of claiming such exemption?

Ans. Gift received from relatives are exempt from tax. by virtue of Section 56. Following persons would be considered as relative

(a) Spouse of the individual;

(b) Brother or sister of the individual;

(c) Brother or sister of the spouse of the individual;

(d) Brother or sister of either of the parents of the individual;

(e) Any lineal ascendant or descendent of the individual;

(f) Any lineal ascendant or descendent of the spouse of the individual;

(g) Spouse of the persons referred to in (b) to (f).

4. Apart from marriage are there any other occasions in which monetary gift received by an individual will not be charged to tax?

Ans. Gift received only on the occasion of marriage of the individual is not charged to tax. Apart from marriage there is no other occasion in which gift received by an individual is not charged to tax. Hence, gift received on occasions like birthday, anniversary, etc. will be charged to tax.

5. Are monetary gifts received from friends liable to tax?

Ans. Gifts received from relatives (as defined in the previous FAQ) are not charged to tax.

Friend is not a relative as defined in the list and hence, gift received from friends will be charged to tax (if other criteria of taxing gift are satisfied).

6. Are monetary gifts received from abroad liable to tax?

Ans. If the aggregate value of monetary gift received during the year by an individual or HUF exceeds Rs. 50,000 and the gifts are not covered under the exceptions prescribed in the preceding FAQ, then gifts whether received from India or abroad will be charged to tax.

7. An Individual received different gifts (cash) from his friends, none of the gift exceeded Rs. 50,000 but the total of the gifts received during the year exceeded Rs. 50,000. What will be the tax treatment in such a case?

Ans. Sum of money received without consideration by an individual or HUF is chargeable to tax if the aggregate value of such sum received during the year exceeds Rs. 50,000.

The important point to be noted in this regard is the “aggregate value of such sum received during the year”. The taxability of the gift is determined on the basis of the aggregate value of gift received during the year and not on the basis of individual gift. Hence, if the aggregate value of gifts received during the year exceeds Rs. 50,000, then aggregate value of such gifts received during the year will be charged to tax.

8. If the aggregate value of gift received during the year by an individual or HUF exceeds Rs. 50,000, whether total amount of gift will be charged to tax or only the amount in excess of Rs. 50,000 will be charged to tax?

Ans. Sum of money received without consideration by an individual or HUF is charged to tax if the aggregate value of such sum received during the year exceeds Rs. 50,000. Once the aggregate value of monetary gift received during the year exceeds Rs. 50,000, then the aggregate value of gift received during the year will be charged to tax.

9. Are there any cases in which the value of immovable property received by an individual or HUF without consideration (i.e. by way of gift) is not charged to tax?|Are gifts of immovable property received by an individual or HUF charged to tax?

Ans. Stamp duty of immovable property is chargeable to tax, if immovable property is received by an Individual or HUF without any consideration and the stamp duty value exceeds Rs. 50000.

However, in the following cases nothing will be charged to tax in respect of immovable property received on or after 01/10/2009 without any consideration, even if the stamp duty value exceeds Rs. 50,000:

• from any relative or by a HUF from its members; or

• on the occasion of the marriage of the individual; or

• under a will/ by way of inheritance; or

• in contemplation of death of the payer or donor as the case may be; or

• from a local authority as defined under Explanation to clause (20) of section 10 of the Income-tax Act, 1961; or

• from any fund, foundation, university, other educational institution, hospital or other medical institution, any trust or institution referred to in section 10(23C); or

• by any fund, trust, institution, any university, other educational institution, any hospital, other medical institution referred to in sub-clause (iv) or sub-clause (v) or sub-clause (vi) or sub-clause (via) of clause (23C) of section 10; or (applicable if the property is received on or after 1st day of April, 2017)

• from or by a trust or institution registered under section 12AA ; or

• from or by a trust or institution registered under section 12A; or (applicable if the property is received on or after 1st day of April, 2017)

• by way of transaction not regarded as transfer: (applicable if the property is received on or after 1st day of April, 2017)

1. property received by way of distribution at the time of total or partial partition of HUF [sec. 47(i)]

2. property received by an Indian subsidiary company, if the parent company or its nominees hold the whole of the share capital of the subsidiary company [sec. 47(iv)] (Inserted by Finance Act, 2018 i.e. w.e.f 01.04.2018)

3. property received by an Indian holding company, if the whole of the share capital of the subsidiary company is held by the holding company [sec. 47(v)] (Inserted by Finance Act, 2018 i.e. w.e.f 01.04.2018)

4. property received by amalgamated company from amalgamating company in the scheme of amalgamation, if amalgamated company is an Indian company. [sec. 47(vi)]

5. property received by resulting company from demerged company in the scheme of demerger, if resulting company is an Indian company. [sec. 47(vib)]

6. property received by a banking institution from banking company in a scheme of amalgamation of a banking company with a banking institution sanctioned and brought into force by the Central Government under sub-section (7) of section 45 of the Banking Regulation Act, 1949 (10 of 1949) [sec. 47(viaa)]

7. property received by successor co-operative bank from predecessor co-operative bank in a business reorganisation. [sec. 47(vica)]

8. from an Individual by a trust created or established solely for the benefit of relative of the Individual. (applicable if the property is received on or after 1st day of April, 2017)

9. from such class of persons and subject to such conditions, as may be prescribed.

FAQs on Gifts received by an individual or HUF

10. An individual received gift of three properties from his friend. The value of none of the property exceeded Rs. 50,000, but the aggregate value of these three properties exceeded Rs. 50,000. What will be the tax treatment of gift in this case?

Ans. In case of immovable property received without consideration by an individual or HUF, the limit of Rs. 50,000 is to be applied transaction-wise and all immovable properties received as gift during the year are not to be clubbed for applying the limit of Rs. 50,000. Hence, if the total stamp value of immovable properties received as gift during the year exceeds Rs. 50,000 but the stamp value of none of the property exceeds Rs. 50,000, then nothing will be charged to tax.

11. Are immovable properties received as gift from friends liable to tax?

Ans. Gifts received from relatives are not charged to tax. Relative for this purpose means:

(a) Spouse of the individual;

(b) Brother or sister of the individual;

(c) Brother or sister of the spouse of the individual;

(d) Brother or sister of either of the parents of the individual;

(e) Any lineal ascendant or descendent of the individual;

(f) Any lineal ascendant or descendent of the spouse of the individual;

(g) Spouse of the persons referred to in (b) to (f).

Friend is not a relative as defined in the above list and hence, gift received from friends will be charged to tax (if other criteria of taxing gift are satisfied).

12. An Individual received gift of a flat from his friend. The stamp duty value of the flat is Rs. 84,000. In this case whether the total value of gifted property will be charged to tax or only the value in excess of Rs. 50,000 will be charged to tax?

Ans. If the conditions discussed in earlier FAQ (regarding the taxability of gift of immovable property) are satisfied, then the entire value of immovable property received without consideration, i.e., received as gift will be charged to tax. Once the taxability is attracted, i.e., value of property received as gift exceeds Rs. 50,000 then the entire value of the property is chargeable to tax. Hence, in this case entire value of property, i.e., Rs. 84,000 will be charged to tax.

13. Would any taxability arise if an immovable property is received for less than its stamp duty value?

Ans. If an Individual or HUF receives (on or after 1st day of October, 2009 but before April 1, 2017) and any person receives (After April 1, 2017), in any previous year from any person or persons any immovable property(being land or building or both):

• without consideration, the stamp duty value of which exceeds Rs. 50,000 then the stamp duty value shall be chargeable to tax.

• for a consideration, if stamp duty value exceeds the amount of consideration and the difference between stamp duty value and consideration is more than Rs. 50,000, then such difference is chargeable to tax. (applicable from A.Y 2014-15 to A.Y 2018-19).

• for a consideration, if stamp duty value exceeds 110% of the amount of consideration and the difference between stamp duty value and consideration is more than Rs. 50,000, then such difference is chargeable to tax. (applicable from A.Y 2019-20)

Provided that where the date of an agreement and date of registration are not same, Stamp Duty will be considered as applicable on the date of agreement. This will be applicable only when the amount of consideration is received by account-payee cheque or bank draft or online transfer or through such other electronic mode as my be precribed before the date of agreement.

Provided that if the stamp duty value of immovable property is disputed by the assessee on grounds mentioned in sub-section (2) of section 50C, the Assessing officer may refer the valuation of such property to a Valuation Officer, and the provisions of section 50C and sub-section (15) of section 155 shall apply in relation to stamp duty value of such property as they apply for valuation of a capital asset under those sections.

14. Are gifts of movable property received by an individual or HUF charged to tax?

Ans. If the following conditions are satisfied then value prescribed for movable property (*) received by an individual or HUF will be charged to tax:

• Prescribed movable property is received without consideration (i.e., received as gift).

• The aggregate fair market value of such property received by the taxpayer during the year exceeds Rs. 50,000

In above case, the fair market value of the prescribed movable property will be treated as income of the receiver.

(*) Prescribed movable property means shares/securities, jewellery, archaeological collections, drawings, paintings, sculptures or any work of art and bullion, being capital asset of the taxpayer.

Considering the above definition, nothing will be charged to tax in respect of gift of any item being a movable property other than covered in the above definition, e.g., Nothing will be charged to tax in respect of a television set received as gift, because a television set is not covered in the definition of prescribed movable property.

($) Refer next FAQ for situations in which prescribed movable property received without consideration by an individual or HUF, i.e., received as gift is not charged to tax.

15. Are there any cases in which the value of prescribed movable property received without consideration, i.e., received as gift by an individual or HUF is not charged to tax?

Ans. If the conditions given in preceding FAQ are satisfied, then value of prescribed movable property received without consideration, i.e., received as gift by an individual or HUF is charged to tax. However, in the following cases nothing will be charged to tax in respect of prescribed movable property received without consideration:

• Property received from relatives.

• Property received by a HUF from its members.

• Property received on the occasion of the marriage of the individual.

• Property received under will/ by way of inheritance.

• Property received in contemplation of death of the donor.

• Property received from a local authority as defined under section 10(20) of the Income-tax Act).

• Property received from any fund, foundation, university, other educational institution, hospital or other medical institution, any trust or institution referred to in section 10(23C).

• Property received from or by a trust or institution registered under section 12AA or section 12A.

• Any shares received by an individual or HUF, as a consequence of business re-organisation of co-operative bank or demerger or amalgamation of a company [as referred to in clause (vicb) or clause (vid) or clause (vii) of Section 47]

• from an induvidual by a trust created or established solely for the benefit of relative of individual.

• from such class of persons and subject to conditions as my be prescribed.

16. An individual received gift of jewellery from his friends. The total value of jewellery received during the year as gift from all the friends amounted to Rs. 84,000. What will be the tax treatment of gift in this case?

Ans. If the aggregate fair market value of prescribed movable property received by an individual or HUF without consideration during the year exceeds Rs. 50,000, then the total value of such properties received during the year without consideration will be charged to tax. In this case the total value of jewellery received during the year exceeds Rs. 50,000 and hence, Rs. 84,000 will be charged to tax.

17. Does any taxability arise if prescribed movable property is received by an individual or HUF for less than its fair market value?

Ans. If the following conditions are satisfied then prescribed movable property (*) received by an individual or HUF will be charged to tax ($):

• Prescribed movable property is acquired by an individual or HUF.

• The aggregate fair market value of such properties acquired by the taxpayer during the year exceeds the consideration of these properties by more than Rs. 50,000. In other words, the aggregate fair market value of all such properties is higher than the consideration and the difference is more than Rs. 50,000.

(*) Prescribed movable property means shares/securities, jewellery, archaeological collections, drawings, paintings, sculptures or any work of art and bullion, being capital asset of the taxpayer.

Considering the above definition, nothing will be charged to tax if any movable property (other than those covered in the above definition) is received for less than its fair market value e.g., Nothing will be charged to tax in respect of a television set received for less than its fair market value because a television set is not covered in the definition of prescribed movable property.

($) Refer next FAQ for situations in which prescribed movable property received for less than its fair market value is not charged to tax.

18. Are there any cases in which prescribed movable property received for less than its fair market value by an individual or HUF is not charged to tax?

Ans. If the conditions given in preceding FAQ are satisfied, then prescribed movable property received (i.e. acquired) by an individual or HUF for less than its fair market value is chargeable to tax. However, in the following cases nothing will be charged to tax in respect of prescribed movable property received for less than its fair market value:

• Property received from relatives (*).

• Property received by a HUF from its members.

• Property received on the occasion of the marriage of the individual.

• Property received under will/ by way of inheritance.

• Property received in contemplation of death of the donor.

• Property received from a local authority as defined under section 10(20) of the Income-tax Act.

• Property received from any fund, foundation, university, other educational institution, hospital or other medical institution, any trust or institution referred to in section 10(23C).

• Property received from a trust or institution registered under section 12AA or section 12A.

• by way of transaction not regarded as transfer under section 47(i)/(iv)/(v)/(vi)/(via)/ (viaa)/(vib)/ (vic)/ (vica)/ (vicb)/ (vid)/ (vii).

• from an individual by a trust created or established solely for the benefit of relative of the individual.

• From such persons and subject to such conditions as may be prescribed.

(*) Relative for this purpose means:

(a) Spouse of the individual;

(b) Brother or sister of the individual;

(c) Brother or sister of the spouse of the individual;

(d) Brother or sister of either of the parents of the individual;

(e) Any lineal ascendant or descendent of the individual;

(f) Any lineal ascendant or descendent of the spouse of the individual;

(g) Spouse of the persons referred to in (b) to (f).

Would taxability arise if any money is received by a non-resident?

As per the amendments made by the Finance (No. 2) Act, 2019, income shall be deemed to accrue or arise in India if it arises due to payment of money, without adequate consideration, by a resident person to a non-resident.

Cases under which gifts received by a non-resident will be taxable in his hands

Gifts received by a non-resident will be taxed in his hands if following conditions are satisfied: -

1. Money is transferred without consideration,

2. Resident person transfers the amount to a non-resident,

3. Aggregate amount exceeds Rs. 50,000 during a previous year,

4. Amount is not received from a relative; example; Spouse, lineal descendant, lineal ascendant, siblings etc.

5. Amount is not received the occasion of marriage or other specified occasions.

Are gifts of any movable or immovable property received by a non-resident charged to tax?

The Finance (No.2) Act, 2019 has amended Section 9 providing that any money exceeding Rs. 50,000, received by a non-resident from a resident person will be taxed in the hands of non-resident provided that the amount is received without adequate consideration.

However, the amendment does not mention anything about the taxability of gift of property as referred to in Section 56(2)(x), inter-alia, immovable property, gold, securities, etc. Thus, if a resident person transfers any property to a non-resident or foreign company then tax shall be levied as per the existing provisions of Income-tax Act read with Double Taxation Avoidance Agreement (DTAA).

If provisions of DTAA are more beneficial, then the non-resident person can choose to apply the provisions of DTAA. All double taxation agreements, India has signed with the foreign countries contain a residuary article ‘Other Income’ which deals with all other incomes not dealt with in any other articles of the said DTAA. Some of the DTAAs allocate the taxing rights to the source country if such residuary income is not dealt with in any other provision of that DTAA, while as some DTAAs provide the taxing right to the resident country only. Thus, if such residuary income is not taxable in India as per DTAA, the deeming fiction introduced in the domestic law can be outweighed by the DTAA. In other words, even if income by way of gift received by non-resident from a person resident in India is deemed to accrue or arise in India, a person can take recourse of the provisions of DTAA to escape from this deeming fiction.

FAQs in respect of filling-up of the Income-tax return forms for Assessment Year 2019-20

1. I am a non-resident. The Taxpayer Identification Number (TIN) is not allotted in my jurisdiction of residence. How do I report the same in the column on “residential status”?

Ans. In case TIN has not been allotted in the jurisdiction of residence, the passport number should be mentioned instead of TIN. Name of the country in which the passport was issued should be mentioned in the column “jurisdiction of residence”.

2. I am a director in a foreign company which does not have PAN. How do I report the same against the column “Whether you were Director in a company at any time during the previous year?”

Ans. You should choose “foreign company” in the drop-down provided for “type of company”. In such case, PAN is not mandatory. However, PAN should be mentioned, if such foreign company has been allotted a PAN.

3. Whether an individual who is a non-resident, or resident but not ordinary resident (RoNR) is also required to disclose details of his directorship in a foreign company which does not have any income accruing or arising in India?

Ans. Yes.

4. I have held shares of a company during the previous year, which are listed in a recognized stock exchange outside India. Whether I am required to report the requisite details against the column “Whether you have held unlisted equity shares at any time during previous year”?

Ans. No.

5. I have held equity shares of a company which were previously listed in a recognised stock exchange, but delisted subsequently, and became unlisted. How do I report PAN of company in the column “whether you have held unlisted equity shares at any time during previous year”?

Ans. In such cases, PAN of the company may be furnished if it is available. In case PAN of delisted company cannot be obtained, you may enter a default value in place of PAN, as “NNNNN0000N”.

6. In case unlisted equity shares are acquired or transferred by way of gift, will, amalgamation, merger, demerger, or bonus issue etc., how to report the “cost of acquisition” and “sale consideration” in the relevant column?

Ans. You may enter zero or the appropriate value against “cost of acquisition” or “sale consideration” in such cases. Please note that the details of unlisted equity shares held during the year are required only for the purpose of reporting. The quantitative details entered in this column are not relevant for the purpose of computation of total income or tax liability.

7. I hold shares in an unlisted foreign company which has been duly reported in the Schedule FA. Whether I am required to report the same again in the column “Whether you have held unlisted equity shares at any time during the previous year?”

Ans. Yes.

8. I have held unlisted equity shares as stock-in-trade of business during the previous year. Whether I have to report the same in the column “Whether you have held unlisted equity shares at any time during the previous year?”

Ans. Yes.

FAQs in respect of filling-up of the Income-tax return forms for Assessment Year 2019-20

9. Please clarify whether holding of equity shares of a Co-operative Bank or Credit Societies, which are unlisted, are required to be reported?

Ans. The details of equity shareholding in any entity which is registered under the Companies Act, and is not listed on any recognised stock exchange, is only required to be reported.

10. I have sold land and building to a non-resident. Whether I need to report the PAN of buyer in the table A1/B1 in Schedule CG?

Ans. As mentioned in ITR form, quoting of PAN of buyer is mandatory only if tax is deducted under section 194-IA or is mentioned in the documents.

11. I am resident and have sold land and building situated outside India. Whether I need to report the details of property and identity of buyer in Schedule CG?

Ans. The details of property and name of buyer should invariably be mentioned. However, quoting of PAN of buyer is mandatory only if tax is deducted under section 194-IA or is mentioned in the documents.

12. Whether it is mandatory to provide ISIN details and scrip-wise computation of Long Term Capital Gains (LTCG) arising on sale of Shares/Mutual Funds units on which STT has been paid?

Ans. The tools for computation of LTCG under sections 112A and 115AD have been provided in the departmental utility for the convenience of taxpayers. These are optional tools designed for computation of the final figures of LTCG, which is then populated in the respective items in Schedule CG. Alternatively, the taxpayers can themselves compute the aggregate long term gain or loss manually, and input the same directly in the respective items in Schedule CG.

13. An unlisted company is required to furnish details of assets and liabilities in the Schedule AL-1 of ITR-6? Please clarify whether details of assets held as stock-in-trade of business are also required to be reported therein.

Ans. In case jewellery/motor vehicle etc. is held as stock-in-trade of business, the drop-down value “stock-in-trade” should be selected against the field “purpose for which used”, while filling up details in the relevant table (table ‘I’ or table ‘H’). In such cases, only the aggregate values are required to be filled up, and the particular details of each asset held as stock-in-trade is not required to be reported.

14. I hold foreign assets during the previous year which have been duly reported in the Schedule FA. Whether I am required to report such foreign asset again in the Schedule AL (if applicable)?

Ans. Yes.

15. An unlisted company is required to furnish details of shareholding as at the end of previous year in the Schedule SH-1 of ITR-6. Please clarify whether these details are required to be furnished in case of an unlisted foreign company.

Ans. Not required.

16. An unlisted company is required to furnish details of assets and liabilities in the Schedule AL-1 of ITR-6. Please clarify whether these details are required to be furnished in case of an unlisted foreign company.

Ans. Not required.

17. Please clarify whether a farmer producer company as defined in section 581A of Companies Act, 1956 is required to furnish details of shareholding in the Schedule SH-1 of ITR-6?

Ans. No. However, please ensure to tick the option ‘Yes’ against the item “whether the company is a producer company as defined in section 581A of Companies Act, 1956?” in Part-A General.

18. A company is required to disclose break-up of all payments and receipts during the year, in foreign currency, as per Schedule FD of ITR-6 (if it is not required to get the accounts audited u/s 44AB). Please clarify whether only the receipts/payments related……

Ans. Yes. In Schedule FD, the break-up of receipts and payments in foreign currency is required to be reported only in respect of business operations in India.

19. In schedule TDS, one is required to enter the head under which corresponding receipt has been offered. In some cases, TDS is deducted by the payer in current year, but corresponding income is to be offered in future years. How to fill up Schedule TDS in such case?

Ans. In such cases, no TDS credit should be claimed under the column “in own hands” for the current year. If this is done, the column “Corresponding receipt offered” is greyed-off and is not required to be filled up.

Facility for registration of IRP/RPs made available on the GST Portal

1. Insolvency Resolution Professionals/ Resolution Professionals (IRPs/RPs), appointed to undertake corporate insolvency resolution proceedings for Corporate Debtors, in terms of Notification. No 11/2020-CT, dated 21st March, 2020 can apply for new registration on GST Portal, on behalf of the Corporate Debtors, in each of the States or Union Territories, on the PAN and CIN of the Corporate Debtor, where the corporate debtor was registered earlier, within thirty days of their appointment as IRP/RP.

2. They should select the Reason for Registration as “Corporate Debtor undergoing the Corporate Insolvency Resolution Process with IRP/RP” from the drop down menu.

3. The date of commencement of business for IRP/RPs will be the date of their appointment. Their compliance liabilities will also come into effect from the date of their appointment.

Facility for registration of IRP/RPs made available on the GST Portal

4. The person appointed as IRP/RP shall be the Primary Authorized Signatory for the newly registered Company.

5. In the Principal Place of business/ Additional place of business, the details as specified in original registration of the Corporate Debtors, is required to be entered.

6. The new registration application shall be submitted electronically on GST Portal under DSC of the IRP/RP

7. The new registration by IRP/RP will be required only once. In case of a change in IRP/RP, after initial appointment, it would be deemed to be change of authorized signatory and not an appointment of a distinct person requiring a fresh registration.

8. In cases where the RP is not the same as IRP, or in cases where a different IRP/RP is appointed midway during the insolvency process, the change in the GST system may be carried out by a non- core amendment in the registration form.

9. The change in Primary Authorized Signatory details on the portal can be done either by the authorised signatory of the Company or by the concerned jurisdictional officer (if the previous authorized signatory does not share the credentials with his successor) on request of IRP/RP.

Do we need to file Nil statement of financial transaction [SFT] or Not

SFT or statement of financial transaction :Section 285BA of the Income Tax requires specified reporting persons to furnish statement of financial transaction. Rule 114E of the Income Tax Rules, 1962 specifies that the statement of financial transaction required to be furnished under sub-section (1) of section 285BA of the Act shall be furnished in Form 61A

Do we need to file Nil statement of financial transaction [SFT] or Not

What is the periodicity and due date of furnishing statement of financial transaction

The statement of financial transactions (online return in Form No. 61A with digital signature) shall be furnished on or before 31st of May, immediately following the financial year in which the transaction is registered or recorded. Section 285BA (5) empower the tax authorities to issue a notice to a person who is required to furnish a statement as above and who has not filed the statement within prescribed time, requiring person to furnish the statement within a period not exceeding 30 days from the date of service of such notice and in such case, the person shall furnish the statement within the time as specified in the notice

Obligation to furnish statement of financial transaction or reportable account.

285BA.(1) Any person, being

(a) an assessee; or

(b) the prescribed person in the case of an office of Government; or

(c) a local authority or other public body or association; or

(d) the Registrar or Sub-Registrar appointed under section 6 of the Registration Act, 1908 (16 of 1908); or

(e) the registering authority empowered to register motor vehicles under Chapter IV of the Motor Vehicles Act, 1988 (59 of 1988) ; or

(f) the Post Master General as referred to in clause (j) of section 2 of the Indian Post Office Act, 1898 (6 of 1898) ; or

(g) the Collector referred to in clause (g) of section 3 of the Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement Act, 2013 (30 of 2013) ; or

(h) the recognised stock exchange referred to in clause (f) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956) ; or

(i) an officer of the Reserve Bank of India, constituted under section 3 of the Reserve Bank of India Act, 1934 (2 of 1934) ; or

(j) a depository referred to in clause (e) of sub-section (1) of section 2 of the Depositories Act, 1996 (22 of 1996) ; or

(k) a prescribed reporting financial institution,

who is responsible for registering, or, maintaining books of account or other document containing a record of any specified financial transaction or any reportable account as may be prescribed, under any law for the time being in force, shall furnish a statement in respect of such specified financial transaction or such reportable account which is registered or recorded or maintained by him and information relating to which is relevant and required for the purposes of this Act, to the income-tax authority or such other authority or agency as may be prescribed.

[Furnishing of statement of financial transaction.

114E.(1) The statement of financial transaction required to be furnished under sub-section (1) of section 285BA of the Act shall be furnished in respect of a financial year inForm No. 61Aand shall be verified in the manner indicated therein.

(2) The statement referred to in sub-rule (1) shall be furnished by every person mentioned in column (3) of the Table below in respect of all the transactions of the nature and value specified in the corresponding entry in column (2) of the said Table in accordance with the provisions of sub-rule (3), which are registered or recorded by him on or after the 1st day of April, 2016

Conclusion : As per Section 285BA of Income Tax Act Read with Rule 114E of Income Tax Rules, Specified Persons having Specified financial transaction or reportable account shall furnish statement of financial transaction with Income Tax Authorities.

Income Tax Act does not specifically mandate filing of nil SFT.

Further CBDT has released aPress Release on 26/05/2017 which says that The registration of reporting person (ITDREIN registration) is mandatory only when at least one of the Transaction Type is reportable. A functionality “SFT Preliminary Response” has been provided on the e-Filing portal for the reporting persons to indicate that a specified transaction type is not reportable for the year.

Therefore it can be concluded that is not Mandatory to file NIL Statement. However it is advisable to submit SFT Preliminary Response.

Do we need to file Nil statement of financial transaction [SFT] or Not

Tags : Do we need to file Nil statement of financial transaction,due date of filing statement of financial transaction, filing of nil SFT, SFT Preliminary Response

ICSI Request for amendment in GST law due to COVID 19

THE INSTITUTE OF COMPANY SECRETARIES OF INDIA

ICSI: PFP:2020

Ms. Nirmala Sitharaman

The Chairperson

Goods & Services Tax Council

5th Floor, Tower II, Jeevan Bharti Building

Janpath Road, Connaught Place

New Delhi-110 001

Sub.: Request for amendment in GST law due to COVID 19

Hon’ble Madam,

Your goodself may kindly be aware that the Institute of Company Secretaries of India (ICSI) is a premier professional body established under an Act of Parliament, namely, the Company Secretaries Act, 1980. The ICSI has nationwide presence with its headquarters at New Delhi, four Regional Offices at New Delhi, Chennai, Kolkata and Mumbai, a Centre for Corporate Governance, Research and Training at Navi Mumbai, a Centre of Excellence for Research and Training at Hyderabad and 72 Chapters spread all over India. The ICSI has on its register over 60,000 members and around 3,00,000 students.

We wish to submit that COVID-19 has brought unprecedented economic crisis before the business entities of India including the professionals like Company Secretaries. The coming months may witness huge liquidity problems in the market. There will be a situation that customers/clients will ask for more credit period as a condition of sales. Thus, business will experience shortage of money for fulfilling its monthly obligation and outflows.

ICSI Request for amendment in GST law due to COVID 19

We wish to further submit that as per the present provisions under the GST Law, the payment of GST is required to be made on accrual basis whether the supplier of goods or services realises the amount of supply of goods or services is immaterial. Even if no amount towards supply of goods or services for a particular month is realised, there remains the liability to pay GST on 20th of the next month. In the event of non-compliance or delay in payment of GST by the due date, the supplier is liable for payment of interest @18% p.a. along with attraction of other penal provisions stated therein the law.

We wish to mention here that when the service tax was first introduced in 1994, the liability to pay service tax (point of supply of service) was on receipt basis, in as much as liability to pay service tax was attracting only on receipt of value of taxable service. This provision in the statute book was in existence for more than a decade and it worked very well in administration of tax law.

The present developments arising due to the spread of the COVID-19 virus has warranted the need for temporary relaxation in compliance requirements under various laws. It is humbly requested that this method (receipt basis) of determining time of supply be introduced for limited period till the industry and business does not come out of crisis arising out of COVID-19.

It is further requested that time of supply of goods or services or both be defined as receipt of money or money equivalent towards supply of goods or services or both and the supplier discharges tax liability on receipt basis proportionate to amount received, inclusive tax. Similarly, a supplier shall avail Input Tax Credit (ITC) proportionate to the payments made within the period of time specified of and reverse credit on non payment of supplies received. This interim measure will not only ensure tax compliance from supplier side, but put a simultaneous check on availment of ITC on payment basis and maintain smooth cash flow of taxes to the exchequer.

We hope that these amendments will help the trade, industry and professionals to great extent and will also help them on focusing on nation building post COVID-19.

We shall be pleased to provide any further information in this regard on hearing from your goodself.

Your spouse not only helps you in meeting your social and personal obligations but also helps you in saving income tax as well. There are certain tax benefits by way of which you can enhance you tax savings through your spouse.

Let us discuss some of important provisions.

Expenses incurred for your children

Presently Indian income tax laws allow you to claim a deduction for education expenses incurred in any university, college, school or educational institution in India in respect of full-time education of two of your children, under Section C, upto an amount of Rs. 1.50 lakh in a year. This deduction is available along with other eligible items like PPF, ULIP and PF etc.. Since this benefit can only be claimed for two children only and if there are more than two children, the other spouse can also claim these expenses for upto additional two children as the limit of two children is applicable for a tax payer and not for a family. Even in case you do not have more than two children but the expenses on education for your children exceeds the limit available under Section 80 C, these expenses can be bifurcated between two parents in such a way so as to maximise the claim amount.

Tax planning through your spouse

Medical Insurance

Section 80 D allows an Individual and HUF to claim deduction upto Rs. 25,000 for medical insurance premium for self and family. As the actual cost of buying a health insurance is so high that even the limit of Rs. 25,000 is not sufficient enough for the entire family to be adequately covered. As the limit of Rs. 25,000 available under Section 80D includes a sub limit of Rs. 5,000 for preventive health check up, the effective limit available for health insurance premium comes down to Rs. 20,000 in case you are availing tax benefit of preventive health check up. Health insurance premium paid in excess of these limits cannot be claimed under Section 80 D in most of the cases if only one spouse is taxpayer. However in case your spouse is also a taxpayer, the health insurance can be bought in such a way so as to ensure that both the spouse are able to claim the fullest possible benefits of Section 80D while ensuring that the entire family gets adequate health insurance cover.

Leave Travel Allowance (LTA) benefits

A person can avail the benefit of LTA in respect of two journeys undertaken during a block period of four years. However if both the spouses are employed then both of them together can claim LTA for four journeys undertaken during the period of four years and thus can go on holidays for every year during the block of 4 years. There is no absolute limit on deduction for LTA.

Home loan benefits

Section 80 C of the Income Tax Act allows an individual and an HUF to claim deduction for certain items which are almost mandatory in nature like Life Insurance Premium, Provident Fund and repayment of housing loans With increased property prices and consequent enhanced amount of home loan one needs to take, the amount of principal repayment itself exceeds the maximum available limit of Rs. 1.50 lakh in most of the cases. This results into most of the home loan borrowers not being able to claim the full benefit of home loan repayment available under Section 80C. In such case if only one spouse is working, the benefit in respect of such overflowing home loan repayment gets lost. However in case both the spouses are earning, the deduction for home loan repayment of Rs. 1.50 lakh can be claimed by both of them provided both spouse are joint owners and co-borrowers as well.

Presently all the tax payers are allowed to claim interest on home loan upto Rs. 2 lakhs in respect of property used for self occupation. So in case of jointly owned house on which a home loan is taken in joint names and serviced by both the spouse, both can claim the deduction of Rs. 2 lakhs each under Section 24(b). Moreover there is a limit of Rs. two lakhs every year on set off of losses under the head ‘income from house property” against other incomes. So it makes sense for both the spouses to become joint owners and co borrowers so as to make both eligible to claim benefit of set off of upto Rs. 2 lakhs in each spouse’s ITR for interest paid on home loan. In cases property is let out, the limit of 2 lakhs will apply after internally setting off the taxable portion of the rent received.

Investments in equity

As per Section 112A a person can claim an initial exemption upto Rs. 1 lakhs on long term capital gains arising on sale/transfer of listed equity shares or units of equity oriented schemes every year provided Security Transaction Tax (STT) has been paid. Since this exemption can be claimed by each tax payers, the investments can be made in the names of both the spouses so as to avail the benefit of this exemption every year as long as it is possible.

From the above discussion it become apparent that though presently there are no separate tax benefits available for working spouse, however a working spouse can still take benefit of existing provisions of tax laws to minimize overall tax liability of the family as a unit.

Balwant Jain is a tax and investment expert and can be reached on jainbalwant@gmail.com and @jainbalwant on his twitter handle.

Day 1: Data Cleansing & Date related Calculation Functions:

Alt Function, Excel Smart Shortcuts, Edit Tool Bar, Randomdata, Smart Copy Paste, Smart Paste special, Transpose, now, date function, Format Cell, Concatenate, Trim & Clean, Proper, Upper, Lower, Left, Right, Mid & Len, Filter, Advance Filter, Format Painter.

Day 2: Advanced Features in Excel:

Concatenate & Text Join, Giving password to excel and back up, Advance Find & Replace, Smart Sorting, Skip Blank, TDS Working Check list, GST Late Fees Calculator, Import 26 AS data and converting in to excel

Day 3: Advanced Excel Functions:

Text to Columns, Flash Fill, Remove Duplicate, Data Validation, Consolidation, Conditional Formatting, if functions, Goto Special, Macro of Spell Number, etc.

Day 4: Advanced Excel Functions:

Calculate Drs Ageing, Sumif, Sumifs, Advance Subtotal, Iferror, Match Function, Vlookup, IF Error+Vlook up, IFError+Vlookup, Hlookup, Xlookup

Day 5: Advanced Excel Functions:

Table, Pivot Table, Sparkline Chart, Use of Onedrive and Google Sheet, Preperation of Balance Sheet from trial.

Advanced excel course fees

No Fees. We are just charging logistic charges of Rs. 600.

This excel expert course helps you to do data analysis using excel course free.

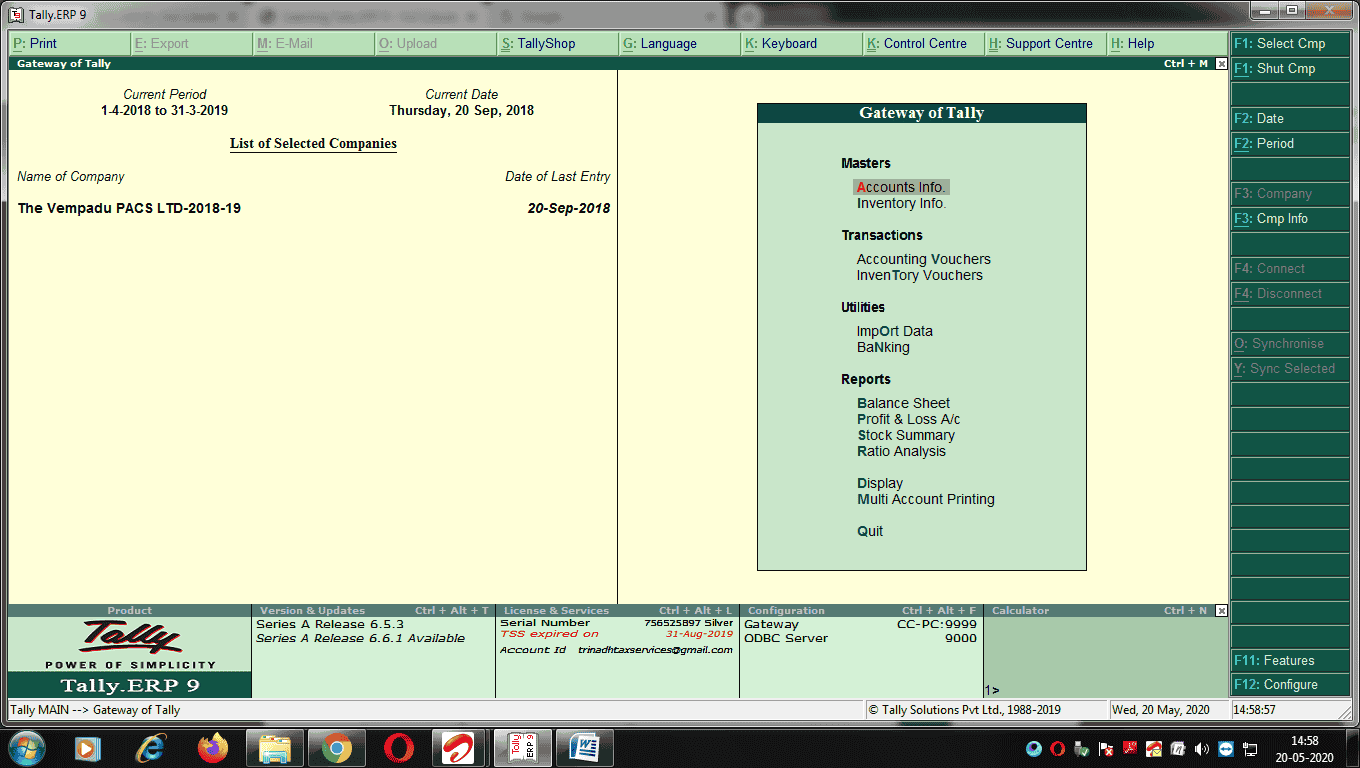

Double click on the Tally ERP 9 icon on your Desktop

Tally ERP 9 Easy Learning Notes

Above Screen Components

Title Bar, Harizontal Button bar, Close button,Gateway of Tally,Buttons toolbar, CalculatorArea, Info panel.

Imp:-

While Working with TallyERP 9, use the following conventions: Mouse /Keyboard Conventions

Action

Particulars

Click

Press the left mouse button.

Double-click

Press and release the left mouse button twice, without moving the mouse pointer off the item

Choose

Position the mouse pointer on the item and click the left mouse button

Select

Position the mouse pointer on the item and doubleclick the left mouse button.

Press

Use the keys on the keyboard in the combination shown

Fn

Press the function key.

Fn

Press ALT + function key

Fn

Press CTRL + function key

Switching between Screen Areas:

When Tally.ERP 9 first loads, the Gateway of Tally screen displays. To toggle between this screen and the Calculator/ ODBC server area at the bottom of the screen, press Ctrl+N or Ctrl+M as indicated on the screen. A green bar highlights the active area of the screen.

Quitting Tally.ERP 9 :-

You can exit the program from any Tally.ERP 9 screen, but Tally.ERP 9 requires all screens to be closed before it shuts down

Following ways to quit working on Tally.ERP 9

1. Press Esc until you see the message Quit? Yes or No ? Press Enter or Y, or click Yes to quit Tally.ERP 9.

2. Alternatively, to exit without confirmation, press Ctrl+Q from Gateway of Tally.

3. You can also press Enter while the option Quit is selected from Gateway of Tally.

1). Creation of a Company:-

Go to Gateway of Tally > Company Info. > Create Company Or from the buttons bar select by using mouse Company Info. Or Alt +F3 to bring up the Company Info Menu

To Select a Company:-

Go to the Gateway of Tally > Alt + F3 > Company Info. > Select Company OR Press F1.

To Alter Company Details :-

Go to the Gateway of Tally > Alt + F3 > Company Info. >Alter

To Shut a Company :-

Go to the Gateway of Tally > Alt + F3 > Company Info. > Shut Company

Or

Alt +F1

2). F11: Features:-

Features are divided in to Four Major Categories –

Accounting Features

Inventory Features

Statutory & Taxation

Tally. NET Features

Gateway of Tally > Press F11 OR

To Select F11:Features from button bar

Note: If you want change some features at any screen of Tally.ERP9 Press F11 (Functional Key).

Accounting Features :-

Go to Gateway of Tally > F11: Features > Accounting Features or click on F1: Accounts

Inventory Features:-

Go to Gateway of Tally > F11: Features > Inventory Features or click on F2 : Inventory

Statutory & Taxation:-

Go to Gateway of Tally > F11: Features > Statutory & Taxation or click on F3 : Statutory

Tally.NET Features:-

Go to Gateway of Tally > F11: Features > Tally.NET Features or click on F4 : Tally.NET

3). F12: Configurations:-

In Tally.ERP 9, the F12: Configurations are provided for Accounting, Inventory & printing options and are user-definable as per your requirements.

The F12: Configuration options vary depending upon the menu display. i.e., if you press F12: configure from Voucher entry screen, the respective F12: Configurations screen is displayed.

Go to Gateway of Tally > press F12: Configure

4). In Master Creation:-

Group and Ledger Creation

Group Creation:–

Go to the Gateway of Tally > Accounts Info. > Groups > Create

Or A +G+C from Gateway of Tally

Group Alter :-

Go to the Gateway of Tally > Accounts Info. > Groups > Alter

Or A +G+A from Gateway of Tally

Group Display:-

Go to the Gateway of Tally > Accounts Info. > Groups > Display

Or A+G+D of Gateway of Tally

You can create Multiple Group:-

Go to the Gateway of Tally > Accounts Info. > Groups > CReate

Or A+G+R from Gateway of Tally

To Alter Multiple Group:-

Go to the Gateway of Tally > Accounts Info. > Groups > AlTer

Or A+G+T from Gateway of Tally

To Display Multiple Group:-

Go to the Gateway of Tally > Accounts Info. > Groups > DIsplay

How to create Ledgers:-

Ledger Creation:–

Go to the Gateway of Tally > Accounts Info. > Ledger> Create

Or A +L+C from Gateway of Tally

Ledger Alter :-

Go to the Gateway of Tally > Accounts Info. > Ledger > Alter

Or A +L+A from Gateway of Tally

Ledger Display:-

Go to the Gateway of Tally > Accounts Info. > Ledger > Display

Or A+L+D of Gateway of Tally

You can create Multiple Ledgers:-

Go to the Gateway of Tally > Accounts Info. > Ledger> CReate

Or A+L+R from Gateway of Tally

To Alter Multiple Ledger:-

Go to the Gateway of Tally > Accounts Info. > Ledger > AlTer

Or A+L+T from Gateway of Tally

To Display Multiple Ledger:-

Go to the Gateway of Tally > Accounts Info. > Ledger > DIsplay

Or A+L+I from Gateway of Tally

5). Creating Inventory Masters in Tally .ERP 9:-

Go to Gateway of Tally – Inventory Info.

Creation of Stock Group :-

Gateway of Tally > Inventory Info. > Stock Groups > Create

Or I+G+C from Gateway of Tally

Alter of Stock Group:-

Gateway of Tally > Inventory Info. > Stock Groups > Alter

Or I+G+A from Gateway of Tally

Creating Units of Measure:-

Gateway of Tally > Inventory Info. > Units of Measure > Create

First change F11 Features -(F2 inventory features)-Maintain Stock Categories-set –Yes to get additional option Stock categories under InventryInfo.

Gateway of Tally > Inventory Info. > Stock Categories > Create or

I+C+C from Gateway of Tally

Creating Godowns:-

First change F11 Features -(F2 inventory features)-Maintain Multiple Godowns-set –Yes to get additional option Godown under Inventry Info.

Gateway of Tally > Inventory Info. > Godown > Create or

I+D+C from Gateway of Tally

6). Voucher Entry in Tally ERP 9 :-

Accounting Vouchers:-

Tally .ERP9 is Pre-Programmed variety of accounting Vouchers, each designed to perform a different Job. The Standard Accounting Vouchers are –

Contra Voucher (F4):- Contra Voucher is use specific for Cash Deposit at Bank & Cash Withdrawal

Gateway of Tally > Accounting Vouchers> F4:Contra

Payment Voucher (F5):- All payment entry in Payment Voucher

Receipt Voucher (F6):- All Receipt entry maid in Receipt Voucher

Journal Voucher(F7) :- All Journal Voucher used for other than cash/bank and Purchase of Goods & Sales of Goods

Sales Voucher /Invoice (F8) :- The Sales Voucher used all cash bank Sales

Credit Note Voucher (Ctrl+F8):- All Sales Return transactions here entered.

Purchase Voucher (F9):- Cash or Credit Purchase entry made here.

Debit Note Voucher (Ctrl+F9) : All Purchase Return transactions here entered.

Reversing Journals (F10):-Reversing Journals are special Journals that are automatically reversed after a specified date. Gateway of Tally +F11 >F1: Accounting Feature –Use Reversing Journal & Optional Vouchers –Yes.

Memo voucher (CTRL+ F10):- Memorandum Vouchers is a non-accounting voucher and the entries made using the memo voucher will not affect your accounts. In other words, Tally does not post these entries to ledgers but stores them in a separate Memorandum Register.

You can use the Memorandum Vouchers for:

Payments towards suspense accounts – consider a company gives its employee cash for Conveyance expenses, the exact nature and cost of which are unknown. For such transactions, you can enter a voucher for the petty cash advance. A voucher to record the actual expenditure details when they are known, and another voucher to record the return of surplus cash. However, a simpler way of doing it is to enter a Memo voucher when the cash is advanced, and then turn it into a Payment voucher for the actual amount spent, when the actual details are known.

Vouchers not verified at the time of entry – if you do not understand the details of a voucher you are entering, you can enter it as a Memo voucher and amend it later when the details are available.

Items given on approval – Generally completed sales are entered into books. In case items are given on approval, use a Memo voucher to track and convert it into a proper Sales voucher. You can delete the memo voucher if the sale is not made.

7). Trade Discounts:-

If we want a separate column for discount in Invoices :-

To activate Separate Discount Column in Invoice-

Gate Way of Tally-Press F11-Features-F2 for Inventory Features-

Activate -Separate Discount Column in Invoice Set as –Yes

Use Different Actual & Billed Quantity

When there is difference between Quantities purchase/sold and delivered,we have to specify quantities, at the time of invoicing.

Example. We have delivered 4 T-Sharts out of which 1 T-Shirt free.then we will issue a bill for 3-T-Shirts.

Gate Way of Tally-Press F11-Features-F2 for Inventory Features-

Active – Use Separate actual and billed quantity Columns as –Yes

Zero Valued Entries in Voucher:-

It is useful Free Samples -in Purchase or Sales vouchers time

Gate Way of Tally-Press F11-Features-F2 for Inventory Features-

Activate – Enable Zero-Valued transactions- Set –Yes

8). Cost Centres:-

Example of Cost Centre are –

Department of an orgation-Finance,Manufacturing,Marketing,HR,Admin Etc

Product/Service of a Company-Product X,Product Y, Product Z

Individual such as Salesman -1,Salesman 2

Go to Gateway of Tally > Press F11 Features- F1 for Accounting Features-

Activate-Maintain Cost Centre-To Yes > Maintain more than one cost category to Yes and Accept the features

Creation of Cost category:-

Gateway of Tally—Accounts Info-Cost Category-Create

Creation of Cost Centre :-

Gateway of Tally—Accounts Info-Cost Centre-Create

9). Invoice No Number Creation:-

Gateway of Tally-Accounts Info-Voucher Types- Alter- Sales-

Method of Voucher Numbering- Select -Automatic-

Use Advance Configuration-Set-Yes-Voucher Type Alteration Screen Display-

Ask –Starting no, Width of Numerical Part- From date-Prefix & Suffix Details