11. After taking into account all the facts and circumstances of the case, we observe that the assessee is well within his rights to choose one of the two properties as self occupied and offered the property as deemed let out at his option. Therefore, we are treating the house at Mumbai as deemed let out and house at Lonavala as self occupied. Accordingly, we set aside the order of Ld. CIT(A) and direct the AO to assess the deemed rent on the same basis as has been done in the assessment year 2012-13.

10. In the present case we find that the ratio of the decision of honourable Jurisdictional High Court in the case of M.Haji Adam & Co. (supra) is duly applicable. In the said case honourable jurisdictional High Court had expounded that in case of trading concerns the addition on account of bogus purchases should be limited to the difference between the gross profit that is shown by the assessee on normal purchase as against the gross profit shown on bogus purchases.

11. Accordingly, we remit the issue to the file of the Assessing Officer to make the disallowance in accordance with the ratio of the decision of Hon’ble Bombay High Court in the case of M.Haji Adam & Co. (supra).

As is discernible from a perusal of the aforesaid statutory provision i.e Sec. 32(2), it can safely be concluded that as the same in substance had remained the same as in context to that applicable to the case of the assessee before us, therefore, the aforesaid view arrived at by the Hon’ble Apex Court seizes the issue under consideration.

Brought forward unabsorbed depreciation cant be set off against Income from HP & other sources

Accordingly, we are of the considered view that as the set-off of the unabsorbed depreciation cannot be bridled with a condition that the business should be continued by the assessee in the said year, therefore, the claim of set-off of the brought forward unabsorbed depreciation by the assessee against its current year Income from house property of Rs.2,15,72,559/- and Income from other sources of Rs.5,60,579/- is found to be in conformity with the mandate of law. We thus not find any infirmity in the order of the CIT(A), who had rightly vacated the incorrect view taken by the A.O, therefore, uphold his order.

Facts being identical, respectfully following the said decision, we hold that the assessee is entitled to depreciation on the non-compete fee. Thus, we sustain the order of the Ld. CIT(A) in treating the payments in the nature of non-compete fee and allowing depreciation. As the Tribunal in assessee’s own case has already held that the payments are in the nature of non-compete fee and entitled for depreciation the contentions raised by the assessee that it is in the nature of goodwill is only academic as submitted by the Ld. Counsel for the assessee. Since the ITAT held that the payments are non-compete fee and allowed depreciation the contention of the assessee in its appeal that it is non-compete fee is eligible for deduction U/s. 37 of the Act as revenue expenditure is rejected.

The Ld. Senior Counsel for the assessee has fairly pleaded that one more opportunity be provided to the assessee and the assessee will appear before the authorities below and file all necessary cogent evidence to prove that the said land was an agricultural land used by the assessee for agricultural purposes and the assessee is entitled to exemption from income tax on the gains which arose on sale of the said land.

Thus, with the observations made by us in this order, we are setting aside and restoring this matter back to the file of AO. The reason is denovo framing of an assessment by afresh determination of the issue on merits as per the law. The assessee is directed to produce all necessary cogent evidence/explanations before the AO in set aside proceedings to substantiate its claim of exemption. The AO shall admit all relevant evidence/explanations submitted by the assessee in support of its contentions in its defence which shall be evaluated by the AO on merits in accordance with the law.

The AO if wishes to rely on any documents/evidence collected at the back of the assessee to prejudice assessee shall forward/furnish a copy of such documents to the assessee for rebuttal. We reiterate that the assessee is seeking to claim exemption from income tax on gains arisen from sale of land. As per the assessee, the land was an agricultural land used for agricultural purposes. Here the onus is on the assessee to prove that its case strictly falls under exemption provisions as are contained in the 1961 Act. Thus, the appeal filed by the assessee is allowed for statistical purposes. We order accordingly.

8. In the result appeal of the assessee is allowed for statistical purposes.

No penalty to be levied on payee when payer who was liable to deduct TDS failed to deduct the same

IN THE INCOME TAX APPELLATE TRIBUNAL

The Relevant Text of the Order as follows :

6. Under this issue the assessee has challenged the levy of interest u/s 234B of the Act of Rs.79,49,35,017/-. The Ld. Representative of the assessee has argued that the payer is under obligation to deduct the tax at source and on account of failure of payer to deduct the tax at source, the penaltyinterest u/s 234B cannot be imposed on the payee. In support of this contention, the Ld. Representative of the assessee has relied upon the law settled by Hon’ble Bombay High Court Director of Income Tax (International Taxation) Vs. Ngc Network Asia LLC (2009) 222 CTR

85 (Bom). In the instant case also the assessee received the payment without deduction of TDS. No doubt, the payer was liable to be deduct the TDS who failed to do so, therefore, the penalty is not leviable to be payee in view of the law settled in Director of Income Tax (International Taxation) Vs. Ngc Network Asia LLC (2009) 222 CTR 85 (Bom). Therefore, in the said circumstances, it is quite clear that the interest and penalty cannot be imposed upon the payer. Accordingly, we decide this issue in favour of the assessee against the revenue.

7. In the result, the appeal filed by the assessee is hereby ordered to be allowed.

G.S.R. 464(E).—In exercise of the powers conferred by section 197 and 206C read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

TCS Return or Form 27EQ amended: Income Tax amendment of rule 31AA

1. Short title and commencement.–– (1) These rules may be called the Income-tax ( 17th Amendment) Rules, 2020.

(2) Save as otherwise provided in these rules, they shall come into force with effect from the 1st day of October, 2020.

2. In the Income-tax Rules, 1962 (hereinafter referred to as the principal rules), in rule 31AA, in sub-rule (4), after clause (v), the following clauses shall be inserted namely:-

“(vi) furnish particulars of amount received or debited on which tax was not collected,-

(a) by the authorised dealer from the buyer under the first proviso to sub-section (1G) of section 206C;

(b) by the authorised dealer under fourth proviso to sub-section (1G) of section 206C; and

(c) by the authorised dealer or seller of an overseas tour program from the buyer under clause (i) or clause (ii) of the fifth proviso of sub-section (1G) of section 206C or in view of any notification issued under clause (ii) of the fifth proviso of sub-section (1G) of section 206C.

(vii) furnish particulars of amount received or debited on which tax was not collected from the buyer,-

(a) under second proviso to sub-section (1H) of section 206C; and

(b) under sub-clause (A) or sub-clause (B) or sub-clause (C), or in view of any notification issued under sub-clause

(C), of clause (a) of the Explanation to sub-section (1H) of section 206C.”

3. In the principal rules, from the date of publication in the Official Gazette, in rule 37BC, in sub-rule (1), after the words “fees for technical services”, the words “, dividend” shall be inserted.

4. In the principal rules, in rule 37CA, the words, brackets, figures and letters ‘sub-section (1) or sub-section (1C)’, wherever they occur, shall be omitted.

5. In the principal rules, in rule 37-I, after sub-rule (2), the following sub-rule shall be inserted namely:-

“(2A) Notwithstanding anything contained in sub-rule (2), for the purposes of sub- section (1F) or, sub-section (1G) or, sub-section (1H) of section 206C, credit for tax collected at source shall be given to the person from whose account tax is collected and paid to the Central Government account for the assessment year relevant to the previous year in which such tax collection is made”

6. In the principal rules, in Appendix II, in Form 27EQ, for the “Annexure”, the following “Annexure” shall be substituted, namely :-

G.S.R. 469(E).—In exercise of the powers conferred by sub-section (7) of section 115UB read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. Short title and commencement.—(1) These rules may be called the Income-tax (18th Amendment) Rules, 2020.

(2) They shall come into force on the date of their publication in the Official Gazette.

(a) for rule 12CB, the following rule shall be substituted, namely:-

“12CB. Statement under sub-section (7) of section 115UB.—(1) The statement of income paid or credited by an investment fund to its unit holder shall be furnished by the person responsible for crediting or making payment of the income on behalf of an investment fund and the investment fund to the-

(i) unit holder by 30th day of June of the financial year following the previous year during which the income is paid or credited in Form No. 64C after generating and downloading the same from the web portal specified by the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) or the person authorised by him and duly verified by the person paying or crediting the income on behalf of the investment fund in the manner indicated therein; and

(ii) Principal Commissioner or the Commissioner of Income-tax, as the case may be, within whose jurisdiction the Principal office of the investment fund is situated by 15th day of June of the financial year following the previous year during which the income is paid or credited, electronically under digital signature, in Form No. 64D duly verified by an accountant in the manner indicated therein.

(2) The Principal Director General of Income-tax (Systems) or the Director General of Incometax (Systems), as the case may be, shall specify the,-

(i) procedure for filing of Form No. 64D and shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the statements of income paid or credited so furnished under this rule; and

(ii) procedure, formats and standards for generation and download of statement in Form No. 64C from the web portal specified by him or by the person authorised by him and he shall be responsible for the day-to-day administration in relation to the generation and download of certificates from the web portal specified by him or the person authorised by him.”

(b) in Appendix-II, for Form No. 64C and 64D, the following Forms shall be substituted, namely: –

“FORM NO. 64C

[See clause (i) of sub-rule (1) of rule 12CB )]

Statement of income distributed by an investment fund to be provided to the unitholder under section 115UB of the Income-tax Act, 1961

1. Name of the unit holder:

2. Address of the unit holder:

3. Permanent Account Number/AADHAAR of the unit holder:

4. Previous year ending:

5. Name and address of the Investment Fund:

6. Permanent Account Number of the Investment Fund:

7. Details of the income or loss [after ignoring the loss under clause (ii) of sub-section (2) of section 115UB] paid or credited by the Investment Fund to the unit holder during the previous year:

8. Details of deemed loss as on 31st March, 2019 in terms of sub-section (2A) of section 115UB (to be passed to the unit holder holding unit on 31st March, 2019):

S.O. 2445 (E).—In exercise of the powers conferred by section 435 of the Companies Act, 2013 (18 of 2013), the Central Government, with the concurrence of the Chief Justice of the High Court of Gauhati hereby designates the Court mentioned in column (2) of the Table below as Special Court for the purposes of providing speedy trial of offences under clause (b) of sub-section (2) of section 435 of the said Act, namely:-

G.S.R…..(E).—In exercise of the powers conferred by sub-rule (4) of rule 48 of the Central Goods and Services Tax Rules, 2017, the Government, on the recommendations of the Council, hereby makes the following amendments in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No.13/2020 – Central Tax, dated the 21st March 2020, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 196(E), dated the 21st March 2020, namely:–

E-Invoicing turnover threshold raised to Rs 500Cr: Read Notification

In the said notification, in the first paragraph,

(i) before the words “those referred to in sub-rules”, the words “a Special Economic Zone unit and” shall be inserted;

(ii) for the words “one hundred crore rupees”, the words “five hundred crore rupees” shall be substituted.

Note: The principal notification was published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide notification No. 13/2020-Central Tax, dated the 21st March, 2020, published vide number G.S.R. 196(E), dated the 21st March, 2020.

Input credit on Purchase of Lift would be available to Hotel as it has been used in the course or for the furtherance of business. Input credit on Purchase of Lift would be available to Hotel as it has been used in the course or for the furtherance of business.

1. In respect of solitary Question, we hold that the input tax credit of tax paid on Lifts procured and installed in hotel building shall not be available to the applicant as the same is blocked in terms of Section 17(5)(d) of the CGST Act 2017, become an integral part of the building.

ITC on Purchase of Lift by Hotel not available being blocked credit

2. The ruling is valid subject to the provisions under section 103(2) untill and unless declared void Section 104(1) of the GST Act.

26. In view of the above, Explanation (a) to the Rule 89(5) is read down to the extent that Explanation (a) which defines “Net Input Tax Credit’ means “input tax credit” only. The said explanation (a)of Rule 89(5) of the CGST Rules is held to be contrary to the provisions of Section 54(3) of the CGST Act. In fact the Net ITC should mean “input tax credit” availed on “inputs” and “input services” as defined under the Act.

27. The respondents are therefore, directed to allow the claim of the refund made by the petitioners considering the unutilised input tax credit of “input services” as part of the “net input tax credit”(Net ITC) for the purpose of calculation of the refund of the claim as per Rule 89(5) of the CGST Rules,2017 for claiming refund under Sub-section 3 of Section 54 CGST Act,2017.

28. In the result, for the forgoing reasons, the petitions are accordingly allowed. Rule is made absolute to the aforesaid extent. No order as to costs.

(J. B. PARDIWALA, J)

(BHARGAV D. KARIA, J)

FURTHER ORDER :

After the judgment is pronounced, Mr. Nirzar Desai learned Standing Counsel for the respondent made a request to stay the operation, implementation and execution of the judgment.

Having regard to what has been stated in the judgment and more, particularly, when Explanation(a) to Rule 89(5) of the CGST Rules, 2017 is held to be ultra vires the provisions of subsection(3) of section 54 of the CGST Act, 2017, request of the learned advocate is rejected.

1. Whether the Applicant is liable to discharge tax liability @ 18% on coal handling and distribution charges wherever the supply of such services is intended to be made expressly to a customer or will the Applicant be entitled to charge GST at the rate of 5% as applicable on supply of coal?

2. Will the applicant be entitled to utilize the input tax credit availed for discharging liability towards the supply of coal and supply of coal handling and distribution charges?

1. In respect of Question 1, we hold that coal handling and distribution charges will be taxable @18% and not 5% wherever the supply of such services only is intended to be expressly made to a customer.

2. In respect of Question No. 2, We have carefully considered the plea of the Applicant and in light of the referred provisions, we are of the opinion that input credit availed as per the conditions specified in section 16 shall be allowed for discharging the liability towards the supply of coal and supply of coal handling and distribution charges respectively.

3. The ruling is valid subject to the provisions under section 103(2) until and unless declared void under section 104(1) of the GST Act.

Book Building Process (IPO, FPO, Dividend), Reverse Book Building Process-Buyback, Underwriting, DRHP Report, Categories of Investors, Issue Price, IPO Online Application, IPO Analysis.

Speaker: Mr. Shailesh Sandel.

Day 2: Secondary Market:

Introduction of Stock Exchange, Index, Offline & Online Trading/ Demat Account, Types of orders, Rolling Settlement, Auction, Contract Note, Brokerage.

Speaker: Mr. Shailesh Sandel

Day 3: Mutual Funds:

Introduction of mutual funds, Types of Mutual Funds, How to choose Mutual Funds Schemes, Basics of Financial Planning.

Speaker: Mrs.Shivani Dani Wakhare

Day 4: Technical Analysis:

The underlying logic of technical analysis, Principles and Assumptions, Difference between Technical and Fundamental Analysis, Basic terms, Primary Trend & Secondary Trend & Minor movements, Trend Reversal, Trading Mode/ sideways, Characteristics of uptrend and downtrend, Reversal patterns, Continuous patterns, Types of charts, Famous candles, Volumes, Technical Indicators, Template

Speaker: Mr Indrajit Panaskar

Day 5: Fundamental Analysis:

Qualitative & Quantitative Analysis, Balance Sheet, P & L, ROE, Debt to Net worth

“14. In the year under consideration, the Ld. CIT(DR)repeated the arguments made before the Tribunal in assessment year 2009-10 and also contested that non-discrimination clause of article 24(3) of the DTAA between India and Japan is not applicable over the assessee and there was no discrimination qua the payer. However, we find that as far as the payment to Honda motor Japan is concerned, the issue in dispute is squarely covered by the decision of the Tribunal in assessment year2009- 10, wherein the Tribunal has followed the decision of the Hon’ble Delhi High Court in the case of CIT Vs. Herbalife (supra).

TDS deduction not applicable on purchase of raw material from non-resident Indian

We note that Hon’ble High Court in the case of Herbalife (supra) has also considered the amendment in provisions of section 40(a)(i) of the Act by way of insertion of sub-clause(ia) w.e.f. 01/04/2005. Accordingly, respectfully following the decision of the Hon’ble Delhi High Court and the order of Tribunal (supra), we delete the disallowance in respect of payment to Honda motor Japan.

15. Regarding payment to Honda Asia Thailand in the year under consideration, the assessee contended that no PE has been held by the DRP in the case of non-resident company in assessment year 2010-11 and this fact was not controverted by the Ld. CIT-(DR), thus, following the decision of the Tribunal in assessment year 2009-10, we hold no disallowance could be made under section 40(a)(i) of the Act for payment made to Honda Asia Thailand without deduction of tax at source.”

Final order:

14. In view of what has been discussed above and following the order passed by the coordinate Bench of the Tribunal in assessee’s own case (supra), we are of the considered view that addition made/sustained by the AO/CIT(A) of Rs.13,09,82,982/- u/s 40(a)(i) of the Act for not deducting the tax at source of payments made for purchase of raw material, components, etc. from non-resident Indian is not sustainable in the eyes of law, hence ordered to be deleted. Consequently, Grounds No.3 & 8 are determined in favour of the assessee.

6. We have heard the rival submissions and perused the relevant materials on record. The reasons for our decisions are given below.

The power of rectification u/s 154 of the Act can be exercised only if there is a mistake apparent from the record of the assessment of the assessee. In other words, in order to attract the power to rectify u/s 154, it is not sufficient, if there is merely a mistake in the order sought to be rectified. The mistake could be rectified must be one apparent from the record. The plain meaning of the word “apparent” is that it must be something which appears to be so ex facie and is incapable of argument or debate. It, therefore, follows that a decision on a debatable point of law or fact or failure to apply the law to a set of facts, which remain to be investigated, cannot be corrected by way of rectification.

Decision on debatable point of law is not a mistake apparent from record thus rectification not possible – ITAT

In T.S. Balaram v. Volkart Bros. (1971) 82 ITR 50 (SC), their Lordships of the Hon’ble Supreme Court have held that a mistake apparent on the record must be an obvious and patent mistake and not something which can be established by a long drawn process of reasoning on points on which there may be conceivably two opinions; a decision on a debatable point of law is not a mistake apparent from record.

In the instant case, the mistake as pointed out by the Ld. counsel is not apparent on the record; not obvious and patent mistake. In the instant case, the mistakes can be established by a long drawn process of reasoning on points on which there may be conceivably two opinions. In the instant case, the mistakes pointed out by the Ld counsel are rather debatable. Thus the ratio laid down by the Hon’ble Supreme Court in Volkart Bros (supra) is squarely applicable here.

In view of the above factual scenario and position of law, we uphold the order of the Ld. CIT(A).

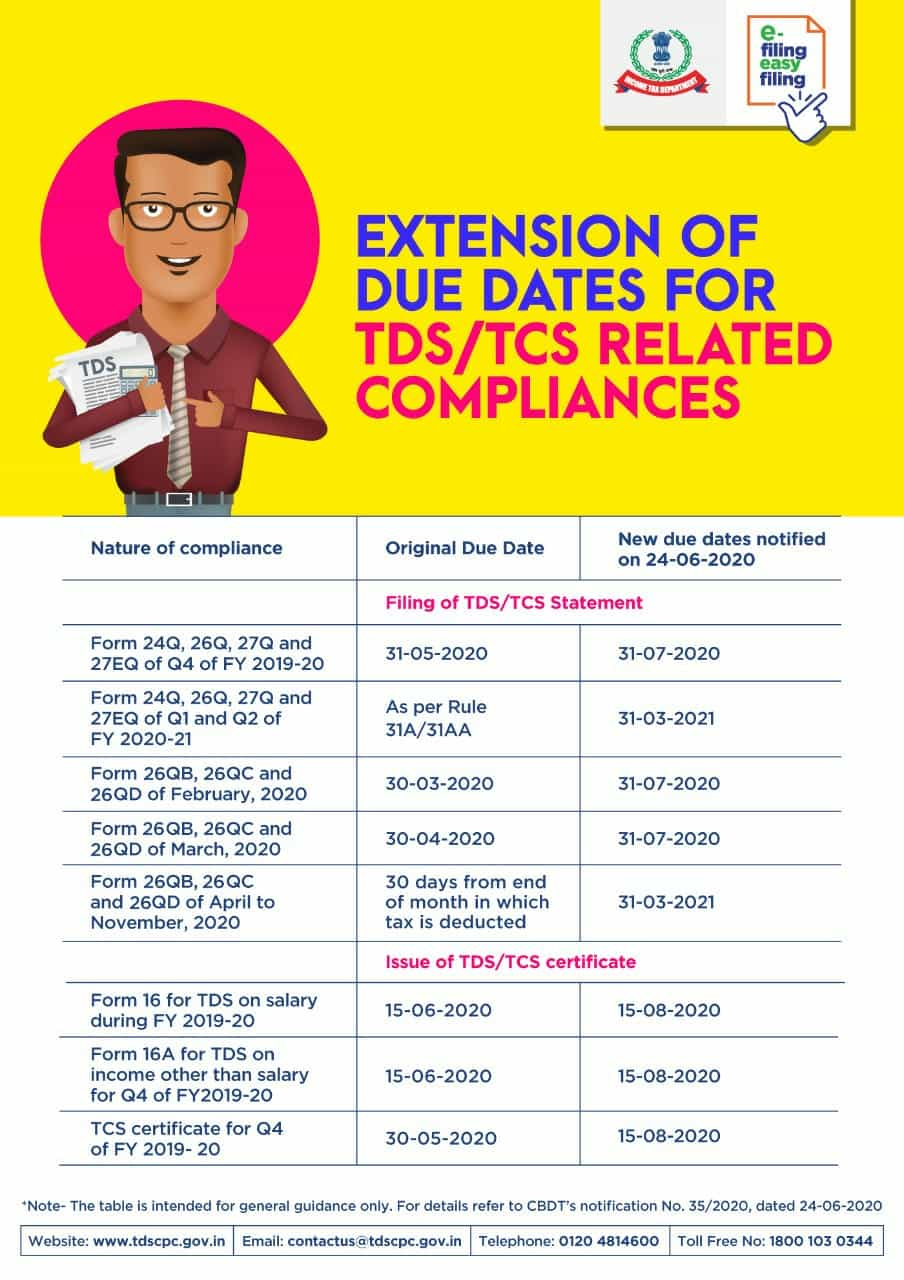

Due Date for filing TDS Return for Q1/Q2 of FY 2020-21 is 31.03.2021

The due date compliance Calendar for TCS/TDS related compliance is given below for your reference. This calendar has been made in line with a tweet made by the Income Tax Department.

ITR Filing due date for AY 2019-20 further extended to 30th Sep 2020

Below is the Notification for reference:

MINISTRY OF FINANCE

(Department of Revenue)

(CENTRAL BOARD OF DIRECT TAXES)

NOTIFICATION

New Delhi, the 29th July 2020

TAXATION AND OTHER LAWS

S.O. 2512(E).– In exercise of the powers conferred by sub-section (1) of section 3 of the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 (2 of 2020), the Central Government hereby makes the following amendment in the notification of the Government of India, Ministry of Finance, Department of Revenue, Central Board of Direct Taxes, number 35/2020, dated the 24th June 2020, published in the Gazette of India, Extraordinary, Part-II, Section 3, Sub-section (ii), vide number S.O. 2033(E), dated the 24th June 2020, namely:-

(i) in the first proviso, in clause (i), in sub-clause (a), for the words, figures and letters “the 31st day of July 2020” the words, figures and letters “the 30th day of September 2020” shall be substituted;

(ii) after the second proviso, the following proviso shall be inserted, namely: –

“Provided also that for the purposes of the second proviso, in case of an individual resident in India referred to in sub-section (2) of section 207 of the Income-tax Act, 1961 (43 of 1961), the tax paid by him under section 140A of that Act within the due date (before the extension) provided in that Act, shall be deemed to be the advance tax:”.

2. This notification shall come into force from the date of its publication in the Official Gazette.

[Notification No. 56/2020/ F. No. 370142/23/2020-TPL]

NIRAJ KUMAR, Dy. Secy. (Tax Policy and Legislation Division)

Note:- The principal notification number S.O. 2033(E), dated the 24th June 2020 was published in the Gazette of India, Extraordinary, Part-II, Section 3, Sub-section (ii), dated 24th June 2020.

GST Department cannot point out deficiencies in refund application after lapse of prescribed time limit

IN THE HIGH COURT OF DELHI AT NEW DELHI

The Text of the Order as follows :

1. The petition has been heard by way of video conferencing.

2. Present writ petition has been filed seeking a direction to respondent to grant refund of Rs.9,12,893/- claimed under Section 54 of the Delhi Goods and Services Tax Act, 2017 (hereinafter referred to as „DGST Act‟) for the month of August, 2019 as well as the grant of interest in accordance with Section 56 of DGST/CGST Act.

3. Learned counsel for petitioner states that in accordance with Section 54(6) of DGST Act read with Rule 91(2) of Delhi Goods and Services Tax Rules, 2017 (for short “DGST Rules”) proper officer is required to refund at least 90% per cent of the refund claimed on account of zero-rated supply of goods or services or both made by registered persons within a period of seven days from the date of acknowledgment issued under sub-rule (l) or sub-rule (2) of Rule 90 of DGST Rules. He states that despite the period of fifteen days from the date of filing of the refund application having expired on 19th November, 2019, the respondent has till date neither pointed out any deficiency/discrepancy in FORM GST RFD-03 nor it has issued any acknowledgement in FORM GST RFD-02.

4. Learned counsel for petitioner further states that even for the refunds for the months of September and November, 2017, petitioner had to file W.P.(C) No.6337/2019 and it was only thereafter the Department had refunded the tax along with partial interest.

5. On the last two dates of hearing, Mr. Anuj Aggarwal, learned counsel for respondent had sought time to obtain instructions. He admits that there has been laxity on the part of the respondent in processing the petitioner‟s application. He, however, states that a formal deficiency memo will have to be issued as certain documents though annexed with the writ petition had not been uploaded by the petitioner along with its refund application.

6. Having heard learned counsel for the parties, this Court finds that Rules 90 and 91 of CGST/DGST Rules provide a complete code with regard to acknowledgement, scrutiny and grant of refund. The said Rules also provide a strict time line for carrying out the aforesaid activities. For instance, Rules 90(2) and (3) of the DGST Rules states that within fifteen days from the date of filing of the refund application, the respondent has to either point out discrepancy/deficiency in FORM GST RFD-03 or acknowledge the refund application in FORM GST RFD-02. In the event deficiencies are noted and communicated to the applicant, then the applicant would have to file a fresh refund application after rectifying the deficiencies. The relevant portion of Rule 90 of CGST/DGST Rules is reproduced hereinbelow:-

GST Department cannot point out deficiencies in refund application after lapse of prescribed time limit

“90. Acknowledgement.- ……….

(1) Where the application relates to a claim for refund from the electronic cash ledger, an acknowledgement in FORM GST RFD- 02 shall be made available to the applicant through the common portal electronically, clearly indicating the date of filing of the claim for refund and the time period specified in in sub-section (7) of section 54 shall be counted from such date of filing.

(2) The application for refund, other than claim for refund from electronic cash ledger, shall be forwarded to the proper officer who shall, within a period of fifteen days of filing of the said application, scrutinize the application for its completeness and where the application is found to be complete in terms of sub-rule (2), (3) and (4) of rule 89, an acknowledgement in FORM GST RFD-02 shall be made available to the applicant through the common portal electronically, clearly indicating the date of filing of the claim for refund and the time period specified in sub-section (7) of section 54 shall be counted from such date of filing.

(3) Where any deficiencies are noticed, the proper officer shall communicate the deficiencies to the applicant in FORM GST RFD- 03 through the common portal electronically, requiring him to file a fresh refund application after rectification of such deficiencies.”

7. In the event of default or inaction to carry out the said activities within the stipulated period, consequences like payment of interest are stipulated in Section 56 of CGST/DGST Act.

8. Admittedly, till date the petitioner‟s refund application dated 4th November, 2019 has not been processed. As neither any acknowledgment in FORM GST RFD-02 has been issued nor any deficiency memo has been issued in RFD-03 within time line of fifteen days, the refund application would be presumed to be complete in all respects in accordance with sub- rule (2), (3) and (4) of Rule 89 of CGST/DGST Rules.

9. To allow the respondent to issue a deficiency memo today would amount to enabling the Respondent to process the refund application beyond the statutory timelines as provided under Rule 90 of the CGST Rules, referred above. This could then also be construed as rejection of the petitioner‟s initial application for refund as the petitioner would thereafter have to file a fresh refund application after rectifying the alleged deficiencies. This would not only delay the petitioner‟s right to seek refund, but also impair petitioner‟s right to claim interest from the relevant date of filing of the original application for refund as provided under the Rules.

10. Moreover, the respondent‟s prayer to raise a deficiency memo is a hyper-technical plea as admittedly, all the relevant documents have been annexed with the present writ petition and the respondent is satisfied about their authenticity.

11. Consequently, this Court is of the view that the respondent has lost the right to point out any deficiency, in the petitioner‟s refund application, at this belated stage.

12. Accordingly, this Court directs the respondent to pay to the petitioner the refund along with interest in accordance with law within two weeks.

13. With the aforesaid directions, present writ petition stands disposed of.

14. The order be uploaded on the website forthwith. Copy of the order be also forwarded to the learned counsel through e-mail.