TCS Rate Chart For Assessment year 2021-22 or Financial Year 2020-21

The Article contains TCS Rate Chart for Assessment year 2021-22 or Financial Year 2020-21. Refer TCS chart for AY 2021-22 in pdf download, TCS rate chart for FY 2020-21 pdf, TCS rate chart FY 2020-21, TCS rates for FY 2020-21, TCS rate chart pdf for your compliances.

In this Article we shall discuss other compliances related to TCS as well, like: Provision for TCS, RATE OF TAX COLLECTION AT SOURCE (TCS), TIME OF DEPOSIT TCS, TCS Payment, TCS Return forms, DUE DATE OF SUBMISSION OF TCS RETURN, MODE OF FURNISHING RETURNS OF TCS, Certificate of TCS, Time limit for issuing TCS certificate, CONSEQUANCE ON DEFAULT IN TCS PROVISIONS

TCS Rate Chart For Assessment year 2021-22 or Financial Year 2020-21

Please note that provisions of Section 206C(1G)(a) – TCS on foreign remittance through Liberalised Remittance Scheme, Section 206C(1G)(b) – TCS on selling of overseas tour package, Section 206C(1H) – TCS on sale of goods over a limit [Not Applicable if the seller is liable to collect TCS under other provision of section 206C] have been introduced by Finance Act 2020 and are applicable with effect from 1st October 2020.

Basic Steps involved in TCS Compliance

- COLLECTION AT SOURCE UNDER SECTION 206(C)

- DEPOSIT OF TAX COLLECTED AT SOURCE IN GOVERNMENT’S TREASURY WITHIN THE STIPULATED TIME

- SUBMISSION OF TCS RETURN WITHIN STIPULATED TIME

- TAG OR ADD OF CHALLAN TO THE TCS STATEMENT

- DOWNLOAD OF TCS CERTIFICATE FROM TRACES

Provision for TCS

Profits and gains from the business of trading, grants of lease or license, sale of motor vehicle under section 206C as Income tax collected at source i.e. TCS

Every person , being a seller shall at the time of debiting of the amount payable by the buyer to the account of buyer or at the time of receipt of such amount from the said buyer, whichever is earlier, collect from the buyer of such amount as income tax.

TCS shall not be collected if buyer declares that purchase of goods shall be utilized for the purpose of manufacture, processing or producing articles or things.

TIME OF DEPOSIT TCS

| Taxpayer | Date of Deposit |

| Is office of the Govt. and tax is paid without production of income tax challan. | On the same day on which tax is deducted |

| Is office of the Govt. and tax is paid with production of income tax challan. | On or before 7 days from the end of month in which tax is collected. |

| Tax is collected by a person other than office of Government | On or before 7 days from the end of month in which tax is collected. |

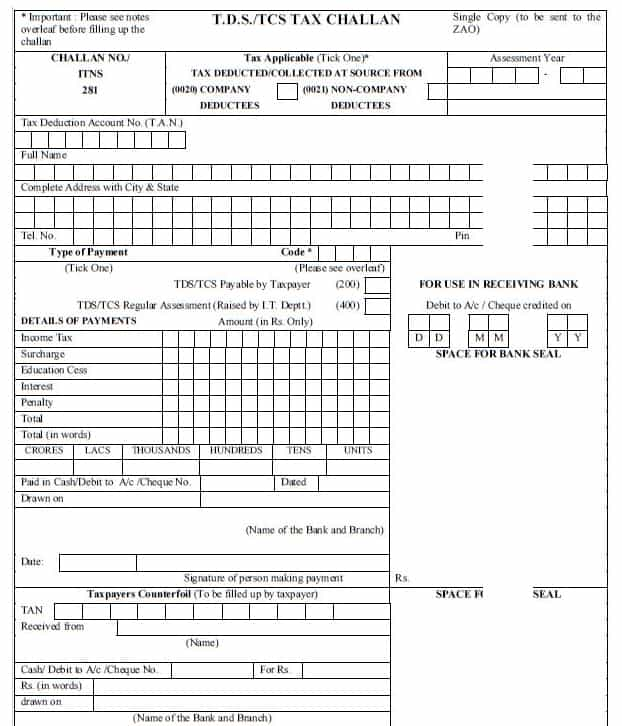

How to Make TCS Payment?

- TCS should be deposit in Challan No. 281

- TCS will have to deposit through internet banking.

- Indicate accurate TAN in challan

- Minor Head of Challan – 200 : TCS payable by tax payer

- Minor Head of Challan – 400: TCS Regular assessment raised by Income Tax Department.

- Amount of TCS, Interest, Late filing fee, penalty etc, should be separately shown while filing the challan

- Note down BSR code, Challan serial number, Date of payment, and amount of challan. This will help you in case challan is misplaced.

TCS Return form

TCS Return has to be submitted quarterly in Form No. 27EQ.

Due Date of Submission of TCS Return form

Due Date of Submission of TCS Return form for FY 2020-21 are given below:

| Quarter | Period | Due Date |

| 1st Quarter | 1st April to 30th June | 15th July 2020 |

| 2nd Quarter | 1st July to 30th September | 15th Oct 2020 |

| 3rd Quarter | 1st October to 31st December | 15th Jan 2021 |

| 4th Quarter | 1st January to 31st March | 15th May 2021 |

How to Furnish Return of TCS

- In case where deductor or collector are an office of Govt. or Principal officer of a company or is person who is required to get his account audited u/s 44AB in immediately preceding financial year or when the numbers of collectee’s are more than 20, then TCS quarterly return shall be submitted electronically.

- Other than above, any other collector can submit TCS return either in paper format or electronically.

- Electronic return can be uploaded with Digital signature or verification of form 27A electronically

- Electronic return will be uploaded in FVU file

- FVU file can be generated through e-TCS RPU (return prepare utility) which is available in

- In every quarter download latest e-TCS RPU

- In e-TCS return details of challan paid [ i.e. TCS amount, Interest, Fee, Other/penalty, BSR code, Challan serial No., Date of challan, Minor head] , details of deductee/collectee has to fill like section under which payment made, PAN, Name, Date of payment, Date deposit of TCS, amount paid, amount of TCS, Rate of TCS etc,.

Process of TCS return by the Income tax department through Traces

- After uploading of TCS return, IT department will process the return.

- Collector has to registered in Traces site and create User ID and Password

- After uploading return, TCS return can be process without default. If TCS return is process with default, that means there is some error in return and there may be demand of short deduction, interest, late filing fee or penalty.

- To know details of process with defaults, justification report has to be downloading.

- If there is demand of short deduction or interest or late filing fee, then collector has to deposit the demand under minor head 400 showing separately TCS, Interest, late fee or others penalty and add this challan to the respective quarterly statement.

- After Tag/add of challan, again TCS correction return has to be uploaded.

- When TCS return is process without default, that means TCS return process is completed. Thereafter TCS certificate has to download.

Certificate of TCS or TCS Certificate

Form 27D is the TCS Certificate. Same is issued within 15 Days of furnishing the TCS Return.

Time limit for issuing TCS certificate

| For the Quarter ending | Form No 27D |

| Jun-30 | Jul-30 |

| Sep-30 | Oct-30 |

| Dec-31 | Jan-30 |

| Mar-31 | May-30 |

CONSEQUANCE ON DEFAULT IN TCS PROVISIONS

| Failure to collect tax at source and paid. [Sec 206C (7)] | Tax with interest @ 1% per month |

| Failure in furnish TCS return within stipulated time [U/S 234E] | Rs. 200 per day and shall not exceed the amount of tax deducted/collected. |

| Penalty for failure to furnish quarterly TCS return [271H] | Rs. 10000/- to Rs. 100000/- |

You May Also Refer:

- Corporate Compliance Calendar for the Month of April 2020

- TCS provisions applicable from 1st Oct 2020- Discussion & Analysis

The post TCS Rate Chart For Assessment year 2021-22 or Financial Year 2020-21 appeared first on Studycafe.

from Studycafe https://ift.tt/3bHQ87o

No comments:

Post a Comment